Since the mid-1980s, many multinational companies (MNCs) have transformed their finance functions into financial shared service centers (FSSCs), in order to cut costs and optimize internal operations. When it came to the 21st century, breakthroughs in technology have witnessed the rapid growth of the digital economy, promoting the digital transformation of enterprises and the digital transformation of finance. The construction of a FSSC has laid a solid foundation for the digital transformation of finance and has gained popularity in large companies. However, the practices of FSSC in China are deeply associated with the development of IT. Some scholars see it as a kind of IT application in the finance function, as evidenced by the active involvement of IT companies in the establishment of FSSCs. In this paper, the authors launched a questionnaire to measure the maturity of the FSSC in Chinese companies. Data was analyzed by using structural equation modeling (SEM), aiming to study the factors that have impacts on the maturity of FSSC and the influencing path of the factors. Influencing factors were designed based on the TOE (Technology-Organization-Environment) theory, and the maturity model of FSSC was modified from the PwC (PricewaterhouseCoopers) maturity model of FSSC. And then a structural model was constructed. Various tests for SEM were used, and the study showed that the technological and organizational conditions of enterprises have promoted the construction and development of FSSCs, while the external environmental conditions indirectly influenced the maturity of FSSC through affecting the organizational and technological conditions. The paper also showed the influencing path of the factors.

| Published in | American Journal of Management Science and Engineering (Volume 9, Issue 6) |

| DOI | 10.11648/j.ajmse.20240906.12 |

| Page(s) | 124-140 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2024. Published by Science Publishing Group |

Digital Transformation, Finance Function, Financial Shared Service Center (FSSC), Structural Equation Modeling (SEM), TOE Theory, Influencing Factors

Dimension | Description and Criteria |

|---|---|

Strategy | 1. Criteria used to select the FSSC location, and their respective ranking 2. Implementation strategy chosen 3. Evaluation of the objectives since FSSC implementation from today's perspective 4. compared to when the FSSC was founded |

Organization/governance/compliance | 1. Center concept of the FSSC (cost center versus profit center) 2. Cost allocation method for services provided 3. Scope and revision cycle of service level agreements 4. “Process owner”approach to manage processes 5. Governance of the FSSC 6. Monitoring of process compliance and use of automated controls |

Continuous improvement | 1. Systematic and regular analysis of costs and quality 2. Continuous search for and implementation of optimization measures 3. Deployment of quality improvement tools 4. Approach to measure whether an FSSC is meeting its objectives |

Business processes | 1. Degree of standardization and automation of processes within the FSSC 2. Degree of standardization and automation of processes in upstream and downstream 3. processes outside the FSSC 4. Level of process documentation |

Customer relations | 1. Customer structure (share of internal and external customers) 2. Service structure and customer orientation within the FSSC 3. Deployment of tools for customer management |

Performance management | 1. Sophistication of performance management systems in place 2. Transparency of the performance measurement process 3. Availability of information related to operational and strategic management 4. Definition of measurable performance targets and monitoring of target achievement 5. Extent of financial control systems within the FSSC |

Human resources management | 1. Use of different training tools and training types by staff group 2. Quality of communication between management and staff in the FSSC 3. Approach to linking the performance evaluation of employees with the definition of development measures 4. Use of employee satisfaction surveys |

Systems and technology | 1. Degree of process automation and standardization of IT systems 2. Continuous optimization of IT systems 3. Extent to which workflow and integrated ERP systems are deployed 4. IT governance supporting financial control processes |

Variables | Dimension | Code | Item | Reference |

|---|---|---|---|---|

Maturity | Organization/governance/compliance | MA1 | Clear structure and governance of FSSC monitoring of process compliance and use of automated controls existed | Pwc (2012) [28] . |

Continuous improvement | MA2 | Continuous search for and implementation of optimization measures in FSSC | ||

Business processes | MA3 | Degree of standardization and automation of processes within and outside the FSSC is high | ||

Customer relations | MA4 | Operation of FSSC is customer orientated | ||

Performance management | MA5 | Transparency of the performance measurement process existed in FSSC | ||

Human resources management | MA6 | Use of different training tools and training types by staff group | ||

Systems and technology | MA7 | IT system deployed is process automated and standardized | ||

Technology | Technology adoption | TE1 | Mature ERP in place before FSSC was established | He Ying and Zhou Fang (2013) [22] ;The Hackett Group (2018) [36] ;Thomas and Hiensch (2016) [37] . |

Functions | TE2 | There are Reliable and multifunctional platform for IT application | ||

Stability | TE3 | The company have continuous maintenance of IT equipment | ||

Compatibility | TE4 | IT system is fit for FSSC | ||

Data management | TE5 | Data management is mature when establishing FSSC | ||

Process automation | TE6 | Automation and standardization have been achieved when establishing FSSC | ||

SMAC* | TE7 | SMAC technology is in use for decision making before FSSC implementation | ||

Business intelligence | TE8 | Business intelligence and expert system are in use for decision making before FSSC implementation | ||

Organization | Organizational design | OR1 | Organization structure is fit for implementation of FSSC | He Ying and Zhou Fang (2013) [22] . |

Support from the top management | OR2 | Top managers deem it necessary to implement FSS to optimize the finance process | ||

Human resources management | OR3 | There are periodic training for employees of the company | ||

Performance management | OR4 | There exists refine and opaque performance evaluation | ||

Environment | Compliance pressure | EN1 | FSSC establishment is required by the governmental agency or industry associations | Xu Feng (2012) [38] . |

Supportive policy | EN2 | FSSC establishment is recommended by the governmental agency | ||

Competitive advantage | EN3 | FSSC helps the company to gain competitive advantages among competitors | ||

Competitors | EN4 | Competitors have implemented FSSC |

Code | Hypothesis |

|---|---|

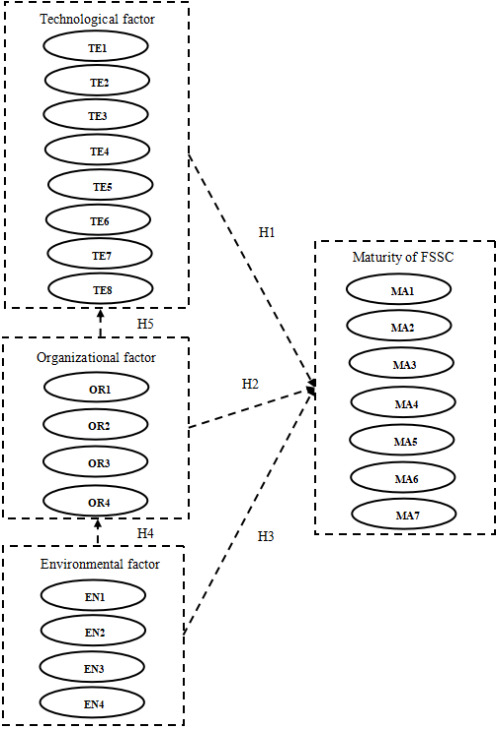

H1 | Higher level of technology has positive effect on maturity of FSSC |

H2 | Good organizational conditions have positive effects on maturity of FSSC |

H3 | A good environmental condition has a positive impact on the maturity of FSSC |

H4 | Environmental conditions have impacts on organizational conditions of FSSC |

H5 | Organizational conditions have impacts on technology implementation of FSSC |

Item | Category | Samples (no) | % | ||

|---|---|---|---|---|---|

Established | Starter | Established | Starter | ||

Industry | Manufacture | 22 | 14 | 24% | 33% |

Wholesaler and retailer | 12 | 4 | 13% | 9% | |

IT | 9 | 4 | 10% | 9% | |

Finance | 7 | 5 | 8% | 12% | |

Transportation | 4 | 3 | 4% | 7% | |

Real estate | 7 | 0 | 8% | 0% | |

Scientific research and technology services | 3 | 3 | 3% | 7% | |

Utilities | 5 | 1 | 5% | 2% | |

Others | 22 | 9 | 24% | 21% | |

Ownership | State owned | 38 | 16 | 42% | 37% |

Private | 31 | 19 | 34% | 44% | |

Foreign | 20 | 3 | 22% | 7% | |

Joint venture | 1 | 5 | 1% | 12% | |

Collectively owned | 1 | 0 | 1% | 0% | |

Revenues | Less than 50 million | 2 | 7 | 2% | 16% |

50M-100M | 4 | 5 | 4% | 12% | |

100M-1000M | 20 | 19 | 22% | 44% | |

100M-10 billion | 31 | 10 | 34% | 23% | |

10 billion -50billion | 11 | 2 | 12% | 5% | |

50 billion -100 billion | 11 | 0 | 12% | 0% | |

100 billion -500 billion | 7 | 0 | 8% | 0% | |

More than 500 billion | 5 | 0 | 5% | 0% | |

Item | Min | Max | Average | Std Err | Skewness | Kurtosis |

|---|---|---|---|---|---|---|

MA1 | 1 | 5 | 3.82 | 0.94 | -0.71 | 0.13 |

MA2 | 1 | 5 | 3.88 | 0.81 | -0.66 | 0.91 |

MA3 | 1 | 5 | 3.46 | 0.89 | -0.37 | -0.30 |

MA4 | 1 | 5 | 3.07 | 1.25 | -0.26 | -0.95 |

MA5 | 1 | 5 | 3.25 | 1.14 | -0.38 | -0.44 |

MA6 | 1 | 5 | 3.43 | 1.10 | -0.41 | -0.64 |

MA7 | 1 | 5 | 3.64 | 0.97 | -0.84 | 0.43 |

TE1 | 1 | 5 | 4.08 | 0.96 | -0.83 | 0.06 |

TE2 | 1 | 5 | 3.92 | 1.04 | -0.68 | -0.46 |

TE3 | 1 | 5 | 4.29 | 0.82 | -1.32 | 2.32 |

TE4 | 1 | 5 | 3.97 | 0.94 | -1.05 | 1.45 |

TE5 | 1 | 5 | 3.90 | 0.96 | -0.85 | 0.56 |

TE6 | 1 | 5 | 3.70 | 0.99 | -0.76 | 0.34 |

TE7 | 1 | 5 | 3.07 | 1.19 | -0.13 | -0.78 |

TE8 | 1 | 5 | 2.86 | 1.24 | 0.10 | -0.95 |

OR1 | 1 | 5 | 3.75 | 0.99 | -0.85 | 0.50 |

OR2 | 1 | 5 | 4.13 | 0.77 | -1.11 | 2.43 |

OR3 | 1 | 5 | 3.79 | 0.97 | -0.68 | 0.21 |

OR4 | 1 | 5 | 3.53 | 0.99 | -0.25 | -0.40 |

EN1 | 1 | 5 | 2.79 | 1.01 | -0.15 | -0.43 |

EN2 | 1 | 5 | 3.38 | 1.00 | -0.51 | 0.30 |

EN3 | 1 | 5 | 3.76 | 1.04 | -0.90 | 0.54 |

EN4 | 1 | 5 | 3.66 | 0.95 | -0.47 | 0.08 |

Variable | KMO Value | Bartlett 's Test of Sphericity | ||

|---|---|---|---|---|

Chi-Square | df | P Value | ||

Technology | 0.874 | 569.138 | 28 | 0.000 |

Organization | 0.786 | 154.955 | 6 | 0.000 |

Environment | 0.666 | 62.711 | 6 | 0.000 |

Maturity | 0.830 | 363.236 | 21 | 0.000 |

Factor | Initial Eigenvalues | Extraction Sums of Squared Loadings | Rotated Sums of Squared Loadings | ||||||

|---|---|---|---|---|---|---|---|---|---|

Total | % of Variance | Cumulative % | Total | % of Variance | Cumulative % | Total | % of Variance | Cumulative % | |

1 | 7.536 | 47.102 | 47.102 | 7.536 | 47.102 | 47.102 | 4.759 | 29.746 | 29.746 |

2 | 2.005 | 12.529 | 59.631 | 2.005 | 12.529 | 59.631 | 3.423 | 21.395 | 51.140 |

3 | 1.222 | 7.640 | 67.271 | 1.222 | 7.640 | 67.271 | 2.581 | 16.131 | 67.271 |

Item | Factor Load Coefficient after Rotation | ||

|---|---|---|---|

Factor 1 | Factor 2 | Factor 3 | |

TE3 | 0.881 | ||

TE5 | 0.852 | ||

TE2 | 0.828 | ||

TE4 | 0.777 | ||

TE6 | 0.759 | 0.351 | |

TE1 | 0.741 | ||

OR3 | 0.771 | ||

OR4 | 0.769 | 0.326 | |

OR2 | 0.442 | 0.735 | |

EN3 | 0.721 | 0.361 | |

OR1 | 0.659 | 0.331 | |

EN4 | 0.526 | ||

TE8 | 0.392 | 0.745 | |

TE7 | 0.464 | 0.706 | |

EN1 | 0.689 | ||

EN2 | 0.656 | ||

Variable | Item | CITC | Cronbach α with deleted items | Cronbach α |

|---|---|---|---|---|

Technology | TE1 | 0.669 | 0.923 | 0.923 |

TE2 | 0.853 | 0.898 | ||

TE3 | 0.828 | 0.904 | ||

TE4 | 0.752 | 0.912 | ||

TE5 | 0.815 | 0.904 | ||

TE6 | 0.772 | 0.910 | ||

Organization | OR1 | 0.686 | 0.811 | 0.849 |

OR2 | 0.725 | 0.803 | ||

OR3 | 0.665 | 0.819 | ||

OR4 | 0.703 | 0.803 | ||

Environment | EN1 | 0.513 | - | 0.678 |

EN2 | 0.513 | - | ||

Maturity | MA1 | 0.665 | 0.881 | 0.893 |

MA2 | 0.722 | 0.877 | ||

MA3 | 0.711 | 0.877 | ||

MA4 | 0.705 | 0.879 | ||

MA5 | 0.748 | 0.871 | ||

MA6 | 0.657 | 0.883 | ||

MA7 | 0.700 | 0.877 |

Latent Variable | Item | Std Err | Std Factor Loading | P Value |

|---|---|---|---|---|

Technology | TE1 | - | 0.702 | - |

TE2 | 0.17 | 0.884 | 0.000 | |

TE3 | 0.134 | 0.875 | 0.000 | |

TE4 | 0.154 | 0.804 | 0.000 | |

TE5 | 0.157 | 0.85 | 0.000 | |

TE6 | 0.161 | 0.805 | 0.000 | |

Organization | OR1 | - | 0.773 | - |

OR2 | 0.107 | 0.828 | 0.000 | |

OR3 | 0.134 | 0.735 | 0.000 | |

OR4 | 0.136 | 0.745 | 0.000 | |

Environment | EN1 | - | 0.535 | - |

EN2 | 0.584 | 0.958 | 0.000 |

Variable | AVE | CR |

|---|---|---|

Technology | 0.675 | 0.925 |

Organization | 0.585 | 0.849 |

Environment | 0.600 | 0.735 |

Variable | Technology | Organization | Environment |

|---|---|---|---|

Technology | 0.822 | - | - |

Organization | 0.554 | 0.765 | - |

Environment | 0.333 | 0.449 | 0.775 |

Index | Norm | Value |

|---|---|---|

χ2 | - | 286.465 |

χ2/df | 1~3 | 1.949 |

RMSEA | <0.10 | 0.103 |

GFI | >0.90 | 0.736 |

CFI | >0.90 | 0.881 |

NFI | >0.90 | 0.786 |

TLI | >0.90 | 0.861 |

IFI | >0.90 | 0.883 |

Index | Norm | Value |

|---|---|---|

χ2 | - | 259.191 |

χ2/df | 1~3 | 1.788 |

RMSEA | <0.10 | 0.094 |

GFI | >0.90 | 0.771 |

CFI | >0.90 | 0.902 |

NFI | >0.90 | 0.807 |

TLI | >0.90 | 0.885 |

IFI | >0.90 | 0.905 |

Hypothesized Path /Structural relationship | Standardized Estimates | C. R. Value | P Value | Is hypothesis Supported? |

|---|---|---|---|---|

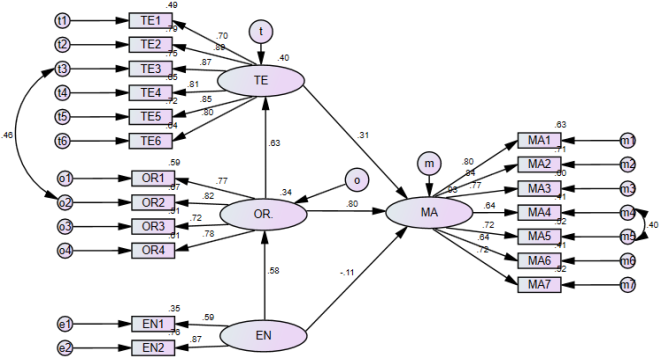

Technology→ Maturity | 0.305 | 3.358 | 0.000 | supported |

Organization→ Maturity | 0.799 | 5.724 | 0.000 | supported |

Environment→ Maturity | -0.111 | -1.009 | 0.313 | Not supported |

Environment→ Organization | 0.582 | 3.192 | 0.001 | supported |

Organization→ Technology | 0.635 | 5.211 | 0.000 | supported |

Constructs | Direct effects | Indirect effects | Total effects |

|---|---|---|---|

Technology→ Maturity | 0.305 | 0.000 | 0.305 |

Organization→ Maturity | 0.799 | 0.194 | 0.993 |

Environment→ Maturity | 0.000 | 0.578 | 0.578 |

MNC | Multinational Company |

FSSC | Financial Shared Service Center |

FSS | Financial Shared Service |

SEM | Structural Equation Modeling |

TOE | Technology-Organization-Environment |

PwC | PricewaterhouseCoopers |

IDC | International Data Corporation |

ERP | Enterprise Resource Planning |

IMA | Institute of Management Accountants |

SSC | Shared Service Center |

BPR | Business Process Re-engineering |

ZTE | Zhongxing Telecom Equipment |

GBS | Global Business Service |

KPMG | Klynveld Peat Marwick Goerdeler |

SMAC | Social Mobile Analytics and Cloud |

SOE | State Owned Enterprise |

RPA | Robotic Process Automation |

KMO | Kaiser-Meyer-Olkin |

CITC | Corrected Item-Total Correlation |

AVE | Average Variance Extracted |

CR | Composite Reliability |

RMSEA | Root Mean Square Error of Approximation |

GFI | Goodness of Fit Index |

CFI | Comparison Fit Index |

NFI | Normed Fit Index |

TLI | Tucker-Lewis Index |

IFI | Incremental Fit Index |

MI | Modification Index |

CIPFA | Chartered Institute of Public Finance and Accountancy |

| [1] | CFO. Thriving in the digital economy: The innovative finance function. Available from: |

| [2] |

IDC. Worldwide digital transformation spending guide. Available from:

https://www.idc.com/getdoc.jsp?containerId=IDC_P32575 (accessed 31 July 2018). |

| [3] | Yang Yin, Liu Qin, Huang Hu. Research on enterprise financial intelligent transformation: Architecture and path process. Friends of Accounting. 2020, (20), 145-150. |

| [4] | Accenture. The CFO reimagined: From driving value to building the digital enterprise. Available from: |

| [5] |

SASAC. Guiding opinions on accelerating the construction of a world-class financial management system by central SOE. Available from:

https://www.sasac.gov.cn/n2588035/c23471965/content.html (accessed 2 March 2022). |

| [6] | Accenture. Digitally transforming finance for the intelligent enterprise. Available from: |

| [7] |

BlackLine Magazine. Share services in an age of finance transformation. Available from:

https://www.blackline.com/blog/shared-services-finance-transformation/ (accessed 27 July 2017). |

| [8] |

IMA. Financial sharing model innovation and application practice research questionnaire analysis report driven by intelligent technology. Available from:

https://www.imachina.org.cn/global_details/1716.html (accessed 2020). |

| [9] | Schulman, D. S. Shared services: Adding value to the business units. New York: Wiley; 1999. Available from: |

| [10] | Bergeron, B. Essentials of shared services. Hoboken: John Wiley & Sons Inc; 2002. Available from: |

| [11] | Herbert, I. P, Seal, W. B. Shared services as a new organizational form: Some implications for management accounting. British Accounting Review. 2012, 44(2), 83-97. |

| [12] | Zhang Ruijun, Zhang Yongji. Strategies for constructing financial sharing service model. Finance and Accounting. 2008, (13), 60-61. |

| [13] |

Chen Hu, Dong Hao. Performance management and evaluation of FSSC. Finance and Accounting. 2008, (22), 61-62. Available from:

https://www.zhangqiaokeyan.com/academic-journal-cn_finance-accounting_thesis/0201268975388.html |

| [14] | Xie Changqiang. Research on design and application of financial sharing information system of H Group. Master's Thesis, Shandong University, Jinan, 2012. |

| [15] |

Zhang Qinglong, Nie Xingkai, Pan Lijing. Typical cases of FSSC in China. Beijing: Publishing House of Electronics Industry;2016. Available from:

https://www.phei.com.cn/module/goods/wssd_content.jsp?bookid=46919 |

| [16] | Cui Yongcheng. Analysis of process reengineering under the financial sharing model of construction enterprises. Friends of Accounting. 2019, (21), 93-95. |

| [17] | Reijers, H. A., Mansar, L. S. Best practices in business process redesign: An overview and qualitative evaluation of successful redesign heuristics. Omega. 2005, 33(4), 283-306. |

| [18] | Martin, W. Critical success factors of shared service projects-results of an empirical study. Advances in Management. 2011, 4(5), 21-26. Available from: |

| [19] | Rohith, R. A literature review on shared services. African Journal of Business Management. 2013, 7(1), 1-7. |

| [20] | Grant, F., Delvin, J. A. Using existing modeling techniques for manufacturing process reengineering: A case study. Computers in Industry. 1999, 8(1), 102-111. |

| [21] | Zhang Ruijun, Chen Hu, Zhang Yongji. Research on key factors of process reengineering of financial shared services in enterprise groups: Based on the management practice of ZTE Group. Accounting Research. 2010, (7), 57-64+96. |

| [22] | He Ying, Zhou Fang. An empirical study on the key factors of implementing financial shared services in Chinese enterprise groups. Accounting Research. 2013, (10), 59-66+97. |

| [23] | Hu Lei. Multi-case study on key success factors of enterprise financial sharing service. Master's Thesis, Southwest University of Political Science and Law, Chongqing, 2019. |

| [24] | Tornatzky, L. G., Fleischer, M., Chakrabarti, A. K. Processes of technological innovation. Lexington, MA: D. C. Heath & Company; 1990. |

| [25] |

The Hackett Group. Global business services transformation: Are you taking the right steps to drive enterprise performance optimization and value? Available from:

https://www.thehackettgroup.com/global-business-services/gbs-transformation/ (accessed 2012). |

| [26] |

KPMG. Global business services—maturity assessment. Available from:

https://assets.kpmg.com/content/dam/kpmg/pl/pdf/2016/10/pl-maturity-assessment.pdf (accessed 2015). |

| [27] | CIPFA. Shared services: Sharing the gain. Available from: |

| [28] |

PwC. Financial shared service center on the rise toward valuable business partners - 2nd generation FSSCs. Available from:

https://pwcplus.de/en/article/156215/financial-shared-service-center/ (accessed 16 July 2012). |

| [29] |

Ma Huijuan. Research on the relationship between financial shared services and organizational change in enterprises: A case study of H Group. Tax. 2019, 13(27), 60-61. Available from:

https://kns.cnki.net/KCMS/detail/detail.aspx?dbcode=CJFD&filename=NASH201927039 |

| [30] | Dong L. Modeling top management influence on ES implementation. Business Process Management Journal. 2001, 7(3), 243-250. |

| [31] | Fahy, M. The financial future. Financial Management. 2005, 21(5), 210-219. Available from: |

| [32] | Chen Hu, Li Ying. Financial sharing services industry survey report. 1st Edition. Beijing: China Finance and Economics Press; 2011, 1-5. Available from: |

| [33] | Chen Yi. Research on FSSC performance evaluation system in the era of "Big wisdom moving cloud". Friends of Accounting. 2018, (16), 73-78. |

| [34] |

MOF. Norms for enterprise accounting informatization work. Available from:

https://kjs.mof.gov.cn/zhengcefabu/201312/t20131216_1025312.htm (accessed 19 December 2013). |

| [35] | MOF. Guiding opinions on comprehensively promoting the construction of management accounting system. Available from: |

| [36] | The Hackett Group. Four critical drivers for successful finance transformation. Available from: |

| [37] | Thomas, D., Hiensch, J. Shared services: How digital can accelerate the leap to value-added differentiation. Cognizant. 2016, (1), 1-16. Available from: |

| [38] | Xu Feng. Research on organizational information system adoption based on integrated TOE framework and UTAUT model. Master's Thesis, Shandong University, Jinan, 2012. |

APA Style

Guo, X., Wu, J., Sun, M. (2024). Impact Factors of the Maturity of FSSC in the Digital Age: A Study Based on Structural Equation Modeling. American Journal of Management Science and Engineering, 9(6), 124-140. https://doi.org/10.11648/j.ajmse.20240906.12

ACS Style

Guo, X.; Wu, J.; Sun, M. Impact Factors of the Maturity of FSSC in the Digital Age: A Study Based on Structural Equation Modeling. Am. J. Manag. Sci. Eng. 2024, 9(6), 124-140. doi: 10.11648/j.ajmse.20240906.12

AMA Style

Guo X, Wu J, Sun M. Impact Factors of the Maturity of FSSC in the Digital Age: A Study Based on Structural Equation Modeling. Am J Manag Sci Eng. 2024;9(6):124-140. doi: 10.11648/j.ajmse.20240906.12

@article{10.11648/j.ajmse.20240906.12,

author = {Xiaomei Guo and Jiajin Wu and Mengdie Sun},

title = {Impact Factors of the Maturity of FSSC in the Digital Age: A Study Based on Structural Equation Modeling

},

journal = {American Journal of Management Science and Engineering},

volume = {9},

number = {6},

pages = {124-140},

doi = {10.11648/j.ajmse.20240906.12},

url = {https://doi.org/10.11648/j.ajmse.20240906.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ajmse.20240906.12},

abstract = {Since the mid-1980s, many multinational companies (MNCs) have transformed their finance functions into financial shared service centers (FSSCs), in order to cut costs and optimize internal operations. When it came to the 21st century, breakthroughs in technology have witnessed the rapid growth of the digital economy, promoting the digital transformation of enterprises and the digital transformation of finance. The construction of a FSSC has laid a solid foundation for the digital transformation of finance and has gained popularity in large companies. However, the practices of FSSC in China are deeply associated with the development of IT. Some scholars see it as a kind of IT application in the finance function, as evidenced by the active involvement of IT companies in the establishment of FSSCs. In this paper, the authors launched a questionnaire to measure the maturity of the FSSC in Chinese companies. Data was analyzed by using structural equation modeling (SEM), aiming to study the factors that have impacts on the maturity of FSSC and the influencing path of the factors. Influencing factors were designed based on the TOE (Technology-Organization-Environment) theory, and the maturity model of FSSC was modified from the PwC (PricewaterhouseCoopers) maturity model of FSSC. And then a structural model was constructed. Various tests for SEM were used, and the study showed that the technological and organizational conditions of enterprises have promoted the construction and development of FSSCs, while the external environmental conditions indirectly influenced the maturity of FSSC through affecting the organizational and technological conditions. The paper also showed the influencing path of the factors.

},

year = {2024}

}

TY - JOUR T1 - Impact Factors of the Maturity of FSSC in the Digital Age: A Study Based on Structural Equation Modeling AU - Xiaomei Guo AU - Jiajin Wu AU - Mengdie Sun Y1 - 2024/12/12 PY - 2024 N1 - https://doi.org/10.11648/j.ajmse.20240906.12 DO - 10.11648/j.ajmse.20240906.12 T2 - American Journal of Management Science and Engineering JF - American Journal of Management Science and Engineering JO - American Journal of Management Science and Engineering SP - 124 EP - 140 PB - Science Publishing Group SN - 2575-1379 UR - https://doi.org/10.11648/j.ajmse.20240906.12 AB - Since the mid-1980s, many multinational companies (MNCs) have transformed their finance functions into financial shared service centers (FSSCs), in order to cut costs and optimize internal operations. When it came to the 21st century, breakthroughs in technology have witnessed the rapid growth of the digital economy, promoting the digital transformation of enterprises and the digital transformation of finance. The construction of a FSSC has laid a solid foundation for the digital transformation of finance and has gained popularity in large companies. However, the practices of FSSC in China are deeply associated with the development of IT. Some scholars see it as a kind of IT application in the finance function, as evidenced by the active involvement of IT companies in the establishment of FSSCs. In this paper, the authors launched a questionnaire to measure the maturity of the FSSC in Chinese companies. Data was analyzed by using structural equation modeling (SEM), aiming to study the factors that have impacts on the maturity of FSSC and the influencing path of the factors. Influencing factors were designed based on the TOE (Technology-Organization-Environment) theory, and the maturity model of FSSC was modified from the PwC (PricewaterhouseCoopers) maturity model of FSSC. And then a structural model was constructed. Various tests for SEM were used, and the study showed that the technological and organizational conditions of enterprises have promoted the construction and development of FSSCs, while the external environmental conditions indirectly influenced the maturity of FSSC through affecting the organizational and technological conditions. The paper also showed the influencing path of the factors. VL - 9 IS - 6 ER -

School of Management, Xiamen University, Xiamen, China

Biography: Guo Xiaomei is a professor and master tutor of the Department of Accounting at Xiamen University. She received her Ph.D. in Management from Xiamen University in 2001. She is currently the director of Management Accounting Research Center of Xiamen University, member of IMA Academic Advisory Committee, editorial board member of China Management Accounting Magazine, and management accounting consulting expert of Fujian Provincial Department of Finance. Her "Management Accounting" was selected as one of the first batch of national first-class online courses and won the special prize of ten years typical case of Fujian MOOCs. In addition, she is also the winner of the 14th National Top 100 management cases. At present, she is mainly engaged in management accounting case development and smart finance related topics, including shared financial talent training project, shared financial center model innovation and application practice project.

Research Fields: Management Accounting; Environmental Accounting; Risk Management and Internal Control

School of Management, Xiamen University, Xiamen, China

Biography: Wu Jiajin is a graduate student of the Department of Accounting at Xiamen University, under the supervision of Professor Guo Xiaomei, participating in the writing of management accounting case documents, and participating in the research on the construction of financial sharing service center.

Research Fields: Management Accounting; FSSC

School of Management, Xiamen University, Xiamen, China

Biography: Sun Mengdie is employed by China Overseas Grand Oceans Group Co., Ltd. Shaoxing Branch, where she is responsible for project financial accounting, fund management, expense reimbursement, and other related tasks. She got her master degree in management (major in accounting_ at the School of Management, Xiamen University.

Research Fields: Management Accounting

Information