2. Review of Related Literature

2.1. Theoretical Review of Literature

2.1.1. Auditing

According to Porter et al.

| [59] | Porter, B. S. (2008). Principles of external auditing, 3rd edition, John Wiley and Sons, Ltd, England. |

[59]

, auditing is a methodical process that involves objectively gathering and assessing evidence related to claims about economic actions and events that the person or organization making the claims has been involved in. The goal is to determine the degree of correspondence between the claims and established criteria and to report the findings to users of the reports that contain the claims. An audit is the gathering and assessment of data to ascertain and document whether the data complies with predetermined standards. The objectivity and honesty of the auditor define their independence, which is why an audit report's credibility depends on the auditor's independence

| [4] | Agbaje, A. G. (2021). Effect of auditors’ independence on the financial reporting quality of Nigerian deposit money banks. Financial Internet Quarterly, 17(2), 59-65. |

[4]

.

An impartial, methodical, and unbiased assessment of financial statements carried out by a professionally trained individual is known as an audit. Internal and external auditing are the two basic categories of auditing. A common definition of auditing is a methodical process of gathering and objectively assessing evidence related to claims made about economic actions and events to determine the extent to which those claims and established criteria correspond, and then informing interested parties of the outcome

| [40] | Lakech, A. &. (2018). Determinant of internal audit effectiveness: in the Gurage region. |

[40]

.

Finding, examining, confirming, and controlling various pieces of evidence within an organization is the aim of auditing. Not every mistake in an annual report can be found by an auditor. The materiality and risk idea limits the amount of work that can be done to keep the auditing process from being too extensive and, consequently, too costly for the client. Although these ideas were not thoroughly examined in this study, they imply that little, insignificant errors may be tolerated by the auditor, provided they do not cause the public to have a false picture of the organization

| [50] | Munro, L. A. (2011). Journal of Business and Industrial Marketing Vol. 26. Iss. 6. pp. 464-48. |

[50]

.

Arnes

| [11] | Arens, R. A. (2011). Auditing, Assurance Service and Ethics in Australia. 8th Edition. Pearson Australia. |

[11]

asserts that auditors have a responsibility to identify material errors. Planning and executing audits to identify unintentional mistakes made by employees and management takes up a large amount of an auditor's work. Auditors find many types of mistakes, including math errors, oversights, misinterpretations, improper application of accounting standards, and inaccurate summaries and justifications. Auditor duties also include the detection of material fraud. Regardless of auditing standards, the auditor's responsibilities to search for errors and fraud remain the same. In both cases, the auditor must get a reasonable assurance as to whether the statements contain no material misstatements

.

2.1.2. Auditors’ Independence

Being independent of parties with a stake in the outcomes disclosed in an entity's financial statements is what is meant by the term "independence of the external auditor." The code of ethics of the public accounting profession helps guide independence from suppliers, clients, and third parties. The support of and relationship to the client company's audit committee, the contract, and the contractual reference to public accounting standards/codes generally provide independence from management

| [15] | Chepkorir. (2013). Factors Influencing Auditors' Independence And Accountability: A Case Study of KTDA Affiliated Tea Factories In BOMET and KERICHO County, KENYA. a research project submitted to the School of Business and Economics in partial fulfillment. N. |

[15]

.

Two criteria have been used to evaluate auditor independence: appearance and reality. While independence in appearance entails avoiding conditions that may lead consumers of the audit reports to infer that the auditor may provide an unbiased view, independence in thought enables auditors to conduct audits with objectivity, honesty, and doubt. Therefore, auditors must be objective in their judgment, be independent of any clients for whom they perform audit services, and be able to withstand pressure from client company managers

| [16] | Chrystelle, R. (2006). Why an auditor can’t be competent and independent: A French case study. European Accounting Review, 15(2), 153-179. |

[16]

.

According to Aliu, Okpanachi, and Mohammed

| [6] | Aliu, M. O. (2018). Auditor’s Independence and Audit Quality: An Empirical Study. International Accounting and Taxation, Review, Vol. 2, No. 2. |

[6]

, an auditor's independence may be summed up as having an objective mindset while making choices during the financial report audit. An auditor's objectivity guarantees that they are perceived as impartial at all times. The dependability and integrity of a financial report can be evaluated by looking at the auditor's independence.

Finding, examining, confirming, and controlling various pieces of evidence within an organization is the aim of auditing. Not every mistake in an annual report can be found by an auditor. The work done throughout the auditing process is restricted by the materiality and risk concept to keep it from being too broad and, thus, too costly for the customer. These ideas were not explored in greater detail in this study, but they imply that minor, insignificant errors are acceptable in the eyes of the auditor, provided they do not create a false impression of the business

| [50] | Munro, L. A. (2011). Journal of Business and Industrial Marketing Vol. 26. Iss. 6. pp. 464-48. |

[50]

.

Additionally, auditor independence is defined by the Independence Standard Board (2000) as the absence of external influences and other factors that could reasonably be expected to impair an auditor's ability to make objective audit decisions. Examine audit independence as necessitating a responsible mindset distinct from the client's interest; the auditor retains a professional yet balanced doubt. To summarize, the independence of the auditor refers to their capacity to conduct the audit, evaluate the findings, and provide an unbiased attestation of the audit report without any undue influence

| [11] | Arens, R. A. (2011). Auditing, Assurance Service and Ethics in Australia. 8th Edition. Pearson Australia. |

[11]

.

According to Adelopo

| [1] | Adelopo, I. (2016). Auditor Independence: Auditing, Corporate Governance, and Market Confidence: Routledge. |

[1]

, there is uncertainty in the definition and conception of auditor independence, which is a challenge for academics and researchers. He contends that this leaves space for manipulation, which breeds more uncertainty

| [63] | Romadhina, A. (2016). Expertise, Independence, and Professional Skills of Internal Auditors in Preventing Fraud on E-Commerce Transactions (A Case Study at Pt KeretaApi Indonesia). Asia Pacific Fraud Journal. 1(2). 337-350. |

| [64] | Saunders, M. E. (n.d.). Research Methods for Business Students (5th ed.). Harlow: Pearson Education Ltd. |

| [66] | Singh, A. S. (2014). Conducting Case Study Research in Non-Profit Organisations. Qualitative Market Research: An International Journal, 17, 77-84. |

[63, 64, 66]

. When implementing evaluation tests based on exam results and creating audit reports, independence refers to an unbiased viewpoint. From those conclusions, it can be inferred that the mentality and mindset of public accountants and experts, free from other parties' influence, persuasion, and control in the preparation, evaluation, and reporting of test results, is the definition of public accountant independence.

According to Aren

| [9] | Arens, A. &. (2000). Auditing: An Integrated Approach, 8th Edition, Prentice-Hall International Edition, United States of America. |

[9]

, the existence of a disagreement between the client and the auditor about how to handle issues related to audit reporting, fraud, and financial misstatements is a necessary condition for auditor independence

| [1] | Adelopo, I. (2016). Auditor Independence: Auditing, Corporate Governance, and Market Confidence: Routledge. |

[1]

. The concept of responsibility, Lauwers

| [42] | Louwers, R. S. (2015). Auditing & Assurance Service: 6th Edition. McGraw-Hill Education: USA. |

[42]

, requires the auditor to maintain their physical and mental autonomy. The auditor needs to be objective, possess an independent mentality, and accept all professional judgment in addition to all audited financial accounts. However, the appearance of independence has an impact on how consumers perceive auditor independence. For example, even in cases when the auditor does not directly or indirectly have a financial stake, they still need to ensure that their activities do not appear to affect their neutrality when offering a judgment. Audit independence is a prerequisite for both professional value and audit quality

| [37] | Joppe, M. (2000). The Research Process. Retrieved February 25, 1998, from. |

[37]

.

2.1.3. Factors Affecting the External Auditor’s Independence

The regulatory environment and auditor independence

Quality audits that are dependable and beneficial for financial statement users are required by regulations governing the accounting profession. Significant modifications to financial statements and business failures increase the likelihood that audit quality and the ethical principles of auditors will be questioned. To be sure of the accuracy of the audited financial statements, the authors therefore recommended exercising greater disbelief regarding the value of the opinion provided

| [43] | Loveday A. Nwanyanwu. (2017). "Audit Quality Practices and Financial Reporting in Nigeria," International Journal of Academic Research in Accounting, Finance and Management Sciences, Human Resource Management Academic Research Society, International Journal. |

| [44] | Mardiah, A. &. (2012). The Effects of Voluntary Disclosure, Audit Tenure, and Audit or Specialization on Information Asymmetry with Audit Committee as A Moderating Variable in Banking Companies Registered in the Indonesia Stock Exchange. Intern. |

| [45] | Mengistu, D. a. (2011). Reliance of External Auditors on Internal Audit Work: A Corporate Governance Perspective. International business research, 4(2), 67-79. |

| [46] | Mohamed, A. H. (2016). Compliance of Auditors to Ethics and Rules of Professional Conduct and Its Impact on Audit Quality. 2, 610 - 621. |

[43-46]

.

The ethical standards and auditor independence

The ethical climate has a significant impact on a public accounting firm's ability to make ethical decisions

| [7] | Apriliani, D. A. (2014). The effect of an organization's ethical culture and ethical climate on the ethical decision-making of an auditor with self-efficacy as a moderating. Review of Integrative Business and Economics Research, 4(1). |

[7]

. Establishing a strong ethical culture and a reputation for justice, both as an employer and as a business, begins with the ethical audit. The findings of an ethical audit can help you identify and address behavioral issues before they cause major financial or reputational harm

| [60] | Ratna, T. (2020). The Effect of Experience, Independence, and Gender on Auditor Professional Scepticism with Professional Ethics as a Moderator. Accounting Analysis Journal, 9(2), 138-145. |

[60]

. Researchers have found that the independence of the auditor is essential to the auditing process and is an intellectual requirement that the auditor be free from any organizational, external, and personal restraints that hinder their ability to perform their duties. This has to do with the auditor's moral behavior

| [5] | Al Quraish, H. F. (2014). The ethical rules of auditing and the impact of compliance with the ethical rules on auditing quality. International journal of research and Reviews in applied sciences, 18(3), 1. |

[5]

.

The greater the auditor's dedication to applying ethics, the higher the quality audit report was. The financial interests and auditor independence are two major guiding principles when it comes to applying ethics: the imperative principle, which directs behavior according to ethical regulations, and the utilitarian principle, which emphasizes weighing the effects of each action rather than adhering to multiple ethical rules

| [57] | Peecher, M. A. (2014). PCAOB’s ‘‘audit failure’’ rate is highly suspect. CFO.com. Available at: http://ww2.cfo.com/auditing/2014/02/pcaobs-audit-failure-rate-highly-suspect/ |

| [61] | Ray. W. & Kurt P. (2001). “Principles of Auditing and other Assurance Services”, 13th Edition, Irwin, Boston. p: 70. |

| [62] | Robson, C. (2011). Real World Research: A Resource for Users of Social Research Methods in Applied Settings, (2nd Ed.). Sussex, A. John Wiley and Sons Ltd. |

[57, 61, 62]

.

The financial interests and auditor independence

The Public Company Accounting Oversight Board (PCAOB) released a report titled "The Financial Interests and Auditor Independence" in 2007. The study looks at how auditor independence and financial interests are related, and it offers reform suggestions to make auditor independence stronger. According to the paper, auditor independence may be weakened by conflicts of interest brought about by their financial interests. For instance, even in the event that a company's financial statements are inaccurate, auditors who own shares in the company they are auditing may be more inclined to see the business favorably. According to Moore et al.

| [47] | Moore, D. A. (2006). Conflicts of interest and the case of auditor independence: Moral seduction and strategic issue cycling. 31(1), 10-29. |

[47]

, Circumstances like the auditor's investment and other financial interests could indicate the auditor's financial interest in the audit. As a result, it may affect the auditor’s financial interests in the audit unit, affecting the professional objective and independent judgment of the auditor.

The client's pressures and Auditor independence.

Regarding this matter, there are two schools of thought regarding the influence of the length of the auditor-client relationship on the quality of the audit process. According to the first school of thought, the auditor's deep understanding of the client and the variables affecting the activity, as well as the time required to attain it, are determined by the length of the relationship with the client

| [69] | Titus, M. M. (2014). Factors affecting external auditors' independence in discharging their responsibilities: A study of medium-level auditing firms in Nairobi.. International Journal of Business & Law Research, 22-35. |

[69]

.

The client valued the experienced auditor more, and the audit office was less dependent on the client and more resilient to pressure. The auditor has been working for years with a single client who supports independence, so they feel stable and independent. This is reflected in the audit process's efficiency, short audit duration, and lack of costs. According to the second opinion, the length of the relationship with the client has a detrimental effect on the auditor's independence because it consolidates the personal relationship, which leads the auditor to overlook certain matters that could compromise the audit's quality and jeopardize the auditor's independence and integrity

| [65] | Shockley, R. (1981). “Perceptions of auditors' independence: an empirical analysis”, The Accounting Review, Vol. LVI No. 4, pp. 785-800. |

[65]

.

The legal and regulatory framework and auditor independence.

A vital component of the accounting and auditing professions is the legal and regulatory environment, as well as auditor independence. It includes all of the rules, laws, and guidelines that control auditor behavior and procedures, guaranteeing their impartiality and independence in carrying out their responsibilities

| [48] | More, D. A. (2000). Wars of interest and the case of auditor independence: Moral seduction and strategic issue cycling. |

| [52] | Ndubuisi, A. N. (2017). Audit Quality Determinants: Evidence from Quoted Health Care Firms in Nigeria. International Journal of Academic Research in Accounting, Finance and Management Sciences, 7(4), 21. |

[48, 52]

. In order to defend the interests of creditors, investors, and other stakeholders who depend on audited financial statements, this framework attempts to preserve the credibility and integrity of the financial reporting process. It creates standards for auditor independence, such as limitations on non-audit activities, payment schedules, and client relationships to reduce conflicts of interest.

2.1.4. Theoretical Literature

Theory of Inspired Confidence

This theory was developed by the Limperg Institute in the Netherlands in 1985. The theory of inspired confidence offers a connection between the requirements for a properly and credibly audited financial report and the ability of the process of auditing to meet those demands. Furthermore, this theory noted that an auditor is known as a confidential agent who drives their function by an independent and expert assessment and the need to present independent judgments that are supported by evidence. According to the Limperg Institute

| [41] | Limperg Institute. (1985)). The social responsibility of auditors: A basic theory on auditors’ function. The Limperg Institute, Netherlands. |

[41]

noted that reducing the occurrence of undetected misstatement of materials means that the accountant is charged with the responsibility of conducting his duties in a manner that doesn’t tarnish his image and betray the already established confidence before a right-thinking individual even if the accountant produces what is less than the expectation of the public. The introduction of the theory of inspired confidence implies that the duties of auditors are derived from the confidence that the public bestows on them concerning the success of the process of audit process and the assurance that the accountant's opinion conveys. Hence, this confidence is an important part of the process; any form of confidence betrayal implies termination of the function or process. Carmichael assessed the social significance of audit and concluded that if, by any means, the stakeholders’ confidence in the effectiveness of the process of audit and report is misplaced, the value placed on the audit is damaged

| [25] | Edmonds, A. &. (2017). An Applied Guide to Research Designs: Quantitative, Qualitative, and Mixed Methods, 2nd ed. London,. United Kingdom Publication. |

| [26] | Ezugwu, C. A. (2014). Auditor’s reputation: the impact on compliance with International Accounting Standard 5 by quoted companies in Nigeria. Kuwait Chapter of Arabian Journal of Business and Management Review, 3: 12. |

| [27] | Fasika, A. (2018). Factors Affecting Perceptions of Private Audit Quality: The Case of Amhara Region A Research for the Partial Fulfillment of the Requirements for the Degree of Master of Accounting and Auditing 1-65. BAHIR DAR. |

[25-27]

.

The Comfort Theory

The origin of this theory is connected to the medical profession. As was suggested by Orlando

| [55] | Orlando, I. (1961). The dynamic nurse-patient relationship functions, processes, and principles. New York: G P Putnam's Sons. |

[55]

, one of the primary duties of nurses is to establish a cordial and good relationship with their patients to create a comfortable atmosphere. The comfort theory was applied for the first time in the auditing profession by Collins

| [19] | Collins, R. (1981). ‘On the Microfoundations of Macrosociology’. American Journal of Sociology, 86(5): 984-1014. |

[19]

, who noted that the conduct and conclusion of an audit process involve an emotional procedure and an orderly approach that creates a sense of social order that leads to conformity. Pentland

opined that financial information that is deceitful is changed to capture its fair and true position by conducting a diligent appraisal of the financial statement, thereby producing comfort for the users. This implies that the application of professional skill and care by an auditor helps to correctly diagnose the ability to apply professional skill and care to the auditor, which is aimed at correctly diagnosing and provisioning appropriate solutions, hence providing comfort for the users of the financial statement of the public sector

| [53] | Okunola, A. O. (2021)). ‘An Assessment of Auditor’s Independence on the Quality of Financial Reporting: Evidence from Lagos State Parastatals’. International Journal of Management, Economics and Social Sciences 2021, Vol. 10(2-3), pp. 88 - 109. |

[53]

.

Performance Theory of Public Sector Auditing

Oluwagbemiga, Zaccheaus, Olugbenga, and Oluwaseyi

| [54] | Oluwagbemiga, O. E. (.(2014)). ‘Stakeholders’ Perception of the Independence of Public Sector Auditors in Nigeria’. Asian Journal of Finance & Accounting 2014, Vol. 6, No. 2. |

[54]

, opined that after the market-based economy began, Eastern Europe and Central countries instituted a functioning auditing practice that is suited for a democratic institutional system. The new institutional theoretical framework was based on the opinion of the majority of countries concerned and on the experience and legislation of Western democracies. The introduction of performance auditing in the public sector is a value-added to the already existing traditional auditing role. In the aspect of financial audit, the auditor has the right to express how the financial statement is prepared, and whether it conforms to the financial reporting framework. Furthermore, the performing audit mandates the auditor to note whether, in all aspects, a program’s administrative role or function has been economically, effectively, and efficiently carried out. The performance audit is a newly introduced type of audit

| [23] | Deyganto, K. O. (2021). Determinants of External Auditors ‘Independence: A Case Study on Ethiopian Authorized Audit Firms. International Journal of Financial Management (IJFM). Vol. 10, Issue 1, 39-54. |

| [24] | Douglas, M. (2015). Meaning of data. Retrieved on 22nd September, Retrieved on 21st June 2020, from http://www.onlineetymologydictionary/data |

| [29] | Field, A. (2008). Discovering statistics using SPSS (3rd ed). SAGE Publications Ltd. |

| [28] | Earnley, S. (2004). The reform of the UK's auditor independence framework after the Enron collapse: An example of evidence‐based policy making. International Journal of Auditing, 8(2), 117-138. |

[23, 24, 29, 28]

. According to the INTOSAI international audit standard, the performance audit represents an independent examination or assessment of the extent to which a program or activities of public institutions efficiently and effectively operate with due consideration to the economy. Aderibigbe

| [2] | Aderibigbe, P. (2005). ‘Auditor’s Independence and Corporate Fraud’. Journal of Social Sciences, 10(2), 135-139. |

[2]

noted that it’s pertinent to comprehend that these days, sufficient conditions don’t necessarily imply that public funds are spent on the provision of the law, but they must maintain effective, efficient, and economic conditions. This type of auditing system has developed to satisfy the quest for greater information by the parliaments, taxpayers, and their representatives regarding the economy and efficient use of resources by the public managers who represent the executives. These requirements made the audit offices develop standard institutional capabilities and apply them in the techniques and procedures of auditing, which ensures that decision-makers can be certain about the effective and economic use of the assets and resources entrusted into their care

| [33] | Hatfield, R. C. (2011). The effects of prior audit involvement and client pressure on proposed audit adjustments. Behavioral Research in Accounting 23(2): 117-130. |

| [34] | Houqe, M. N. (2010). The effect of IFRS adoption and investor protection on earnings quality around the world. A Working Paper No. 70. Centre for Accounting, Governance and Taxation Research, School of Acc. |

| [35] | Iyad. K, ” (2002)., following the organizational structure of companies subject to review on auditor independence”, unpublished Master Thesis, University of Damascus, Damascus, p. 53. |

[33-35]

.

2.2. Empirical Literature Review

Chepkorir

| [15] | Chepkorir. (2013). Factors Influencing Auditors' Independence And Accountability: A Case Study of KTDA Affiliated Tea Factories In BOMET and KERICHO County, KENYA. a research project submitted to the School of Business and Economics in partial fulfillment. N. |

[15]

The study "Factors Influencing Auditor's Independence and Accountability" sought to ascertain what factors support the auditor's independence and accountability, as well as whether the auditor's tenure at the audit firm has an impact on their work in Kenyan KTDA Tea factories and the influence of the audit committee's competence on the auditor's independence. The results showed that the four factors—audit firm size, audit firm tenure, audit fees, and audit committee commitment—had a significant and favorable impact on the auditor's independence.

A questionnaire was used to gather information. Stepwise multiple regression, Pearson's product-moment coefficient, and descriptive statistics were used in univariate, bivariate, and multivariate analyses. The results indicate that financial reporting (as determined by financial statement reliability) and audit quality metrics (auditor independence, technical training and credentials, and engagement effectiveness) have a statistically significant, positive, strong association.

Munro and Stewart

| [50] | Munro, L. A. (2011). Journal of Business and Industrial Marketing Vol. 26. Iss. 6. pp. 464-48. |

[50]

discovered that when evaluating internal control risks, external auditors often depend heavily on their clients' internal audits. As a result, they may not do as much substantive testing or gather as much data as necessary. Therefore, such reliance on IAF could be seen as a danger to independence. According to

| [38] | Kaklar, H. K. (2012). Audit quality and financial reporting quality: Case of Tehran Stock Exchange (TSE). Innovative Journal of Business and Management, 1: 3, May - June, 43-47. |

[38]

, a high-quality audit should produce a high-quality financial report that may be used as a tool to prevent financial crises.

Using a qualitative research methodology, Muthui et al.

| [51] | Muthui, T. M. (2014). Factors Affecting External Auditors’ Independence in Discharging their Responsibilities: A Survey of Medium Level Auditing Firms in Nairobi, International Journal of Business & Laws Research, 2(4), Pp 22-35. |

[51]

investigated the variables influencing the independence of external auditors in medium-sized audit companies in Nairobi. They discovered that, depending on the members, relationships with clients got better over time. Their analysis suggests upholding quality standards in line with widely recognized auditing practices. They stated in their study's conclusion that an audit firm's independence is impacted by its longevity.

Using a qualitative study approach, Aqeel

| [8] | Aqeel Al-Bawab, A. (2012). The Factors which Affect the Choice of the External Auditor in Jordanian Banks from the Perspective of the External Auditor in Jordan (An empirical study), International Journal of Humanities and Social Sciences, 2(6), Pp 180. |

[8]

investigated the variables influencing Jordanian banks' decisions about their external auditors. According to his research, there were a few factors that Jordanian banks had in common that contributed to the external auditor switch, including new management and management decisions. In addition, he discovered additional justifications for switching external auditors that have to do with generally accepted auditing norms, like lower auditor fees and conflicts between bank management and the auditor. Additionally, he discovered a few justifications for the audit office to substitute a different external auditor.

The Generalized Least Squares (GLM) method was employed by Admasu, A.

| [3] | Admasu, A. (2012). Factors Affecting the Performance of Micro and Small Enterprises in Arada and Lideta Sub-Cities. Unpublished Master’s Thesis, Addis Ababa University. |

[3]

to examine the variables influencing the independence of government auditors. They found that NAS and fierce rivalry among auditors are the two primary factors that significantly influence people's perceptions of the independence of auditors. The investigation also found consistency in the results provided by the government auditors. Arens, A. E.

| [10] | Arens, A. E. (2012). Auditing and Assurance Services: An Integrated Approach, 4th ed, Pearson Prentice Hall, USA. |

[10]

examined the independence and caliber of the audits carried out by the auditors in Nigerian deposit money institutions using panel data analysis. Their findings indicate a favorable correlation between audit quality and audit charge.

Furthermore, a significant association has been observed between audit quality and audit firm rotation, suggesting that a consistent rotation of auditors among firms could function as a safeguard against any threats to auditor independence that may compromise audit quality. Muthui et al.

| [51] | Muthui, T. M. (2014). Factors Affecting External Auditors’ Independence in Discharging their Responsibilities: A Survey of Medium Level Auditing Firms in Nairobi, International Journal of Business & Laws Research, 2(4), Pp 22-35. |

[51]

used a qualitative research methodology to examine the factors impacting the independence of external auditors in medium-sized audit firms located in Nairobi. They found that ties with clients improved over time, contingent on the members. As per established auditing guidelines, their research suggests upholding quality. They concluded their investigation by saying that an audit firm's longevity affects its independence.

John and Chukwumerije

| [36] | John, A. O. (2012). Perceptions of Accountants on Factors Affecting Auditors’ Independence in Nigeria. International Journal of Research in Commerce, IT & Management, 2(11), 25-30. |

[36]

investigated the elements influencing the independence of Nigerian auditors. Utilizing a survey research approach, the study sampled 150 chartered accountants from 15 audit firms in Lagos at random, and data were gathered using a Likert-rated questionnaire. Descriptive statistics and chi-square were used in the analysis to evaluate the hypothesis. Their findings demonstrate a substantial association between the auditor's independence and each of the following factors: audit firm size, audit market competition, audit firm tenure, audit fee size, and non-audit services.

Establishing audit committees greatly enhances auditor independence, per Board

| [12] | Board., I. S. (2000). Statement of Independence Concepts: A Conceptual Framework for Auditor Independence, Exposure Draft (No. ED 00-2). |

[12]

research. Audit Committee A small group of board of directors’ members make up a company's audit committee, and one of its responsibilities is to help the auditors continue to be independent from management. As a result, the hypothesis that audit committees and auditor independence are positively connected—that is, that the presence of an audit committee increases an auditor's independence—is strongly supported by the available data.

Establishing audit committees greatly enhances auditor independence, per Chan, H

research. Audit Committee A small group of board of directors’ members make up a company's audit committee, and one of its responsibilities is to help the auditors continue to be independent from management. As a result, the hypothesis that audit committees and auditor independence are positively connected—that is, that the presence of an audit committee increases an auditor's independence—is strongly supported by the available data.

Conversely, Tesfamichael

| [68] | Tesfamichael, T. (2016). Perception of Auditors on Mandatory Audit Firm Rotation and Its Effect on Auditors' Independence in Ethiopia (Doctoral dissertation, AAU. |

[68]

his goal in the study "Perception of Auditors on Mandatory Audit Firm Rotation and Its Effect on Auditors' Independence in Ethiopia" was to investigate how external auditors perceived the impact of mandatory audit firm rotation on auditor independence in Ethiopia. Long audit tenure, financial reliance on a single audit client, non-audit services rendered to audit clients, and employment of former auditors by audit clients are all factors that can compromise an auditor's ability to maintain their independence

| [14] | Chepkorir, C. (2014). “Factors Influencing Auditors' Independence and Accountability.” Academia, Sept. |

[14]

.

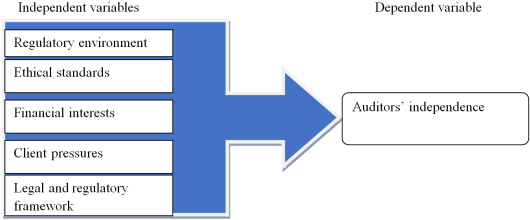

2.3. Conceptual Framework

Based on the above review of related literature, the researcher has developed the following conceptual framework for analysis. This particular study emphasized factors affecting external auditors’ independence. Therefore, the finding depends on the relationship and outputs of the dependent and independent variables.

Figure 1. Conceptual Framework.

3. Research Methodology

3.1. Research Design

This study uses an explanatory survey research design to investigate causal linkages and interactions between variables. The design aims to understand the causal relationships between factors and the level of independence exhibited by external auditors in the Ethiopian context. The researchers collect data from participants using surveys or questionnaires, analyzing the data to conclude relationships between variables. This design allows for deeper investigation into the underlying mechanisms and reasons behind observed phenomena.

3.2. Research Approach

In the study, a quantitative approach was adopted. A quantitative approach refers to a systematic and empirical method of gathering and analyzing numerical data to understand and explain phenomena. The quantitative approach entails the gathering of data to quantify the information and subject it to statistical analysis to confirm or refute competing knowledge claims

| [22] | Creswell, J. (2003). Research design : qualitative, quantitative, and mixed methods approaches. Thousand Oaks, California. |

[22]

.

3.3. Population and Sample

The people who pique the attention of the researchers in extrapolating the study's findings are known as the research population. According to Creswell

| [20] | Creswell, J. (2014). Research design : qualitative, quantitative, and mixed methods approaches. Thousand Oaks, California:. |

[20]

the population can also be defined as the total number of units (people, groups, occasions, things, or things) from which samples are taken for analysis. The 140 external auditors in the study region comprised the population employed in this investigation. An individual or group of respondents chosen as representative of a broad population is called a sample. The act, procedure, or method of choosing a sample is known as sampling

| [17] | Church, B. J. (2018). Auditor Independence in the United States: Cornerstone of the Profession or Thorn in Our Side? Accounting Horizons, 32, 145-168. |

| [18] | Church, B. K. (2012). PCAOB inspections and large accounting firms. Accounting Horizons 26(1): 43-63. |

| [21] | Creswell, J. W. (2009). Research Design: Qualitative, Quantitative, and Mixed Research Approaches. Los Angles. |

[17, 18, 21]

.

3.4. Data Sources and Types

Information was gathered by the researcher from primary and secondary data sources. Individual external auditors employed in the chosen case area served as the study's primary source of data, with secondary data coming from other sources, including the internet, books, journals, publications, records, and the outcomes of previous research projects. Researchers can obtain a wider range of data, validate findings, and present a more thorough study of the research issue by merging primary and secondary data sources. It enables the triangulation of data from several sources, improving the quality and dependability of the study's conclusions.

3.5. Data Collection Procedures

Data collection is crucial for statistical analysis and can be divided into primary and secondary data. This study used questionnaires and interviews to gather data, with interviews being a common method for understanding people's views and preferences. Researchers collect qualitative data from observations, interviews, documents, and audiovisual materials. The questionnaire, a five-point Likert scale, was used to measure respondents' agreement or disagreement with the claims made under each idea.

3.6. Data Analysis

This study used descriptive and inferential analysis to examine factors affecting external auditors' independence. Data was gathered from primary and secondary sources and analyzed using SPSS Vr.25 software. Descriptive analysis ranked variables based on mean and standard deviation, while inferential analysis tested the significance of the data. Pearson's correlation and multiple linear regressions were used to analyze the relationships between the dependent variable and the independent variables, aiming to provide insights into the factors affecting auditor independence.

4. Data Analysis and Interpretation

This chapter covers the study's findings as outlined in the research methodology as well as presentations, discussions, and interpretations of the data gathered through questionnaire analysis. The study focused on 140 external auditors in Mirab Omo zone Bero Woreda. Of these, 135 were completed and recovered, yielding a 96.4% response rate. This response rate was outstanding and supported the claim made by Pallant, J.

| [56] | Pallant, J. (2011). A Step-by-Step Guide to Data Analysis Using the SPSS Program: Survival Manual, (4th Ed.). McGraw-Hill, Berkshire. |

[56]

that a response rate of at least 70% is excellent and that a rate of no less than 50% is appropriate for generalizing findings to the entire population. As a result, 135 respondents provided good study response rates, and the analysis was conducted using their responses.

4.1. Test of Regression Assumptions

4.1.1. Normality Test

This assumption is applied to ascertain whether the residuals are normally distributed. P-P plot dots should be closer to the diagonal line to indicate that the study's normalcy assumption has been met; normal P-P plot points should sit on a substantially straight diagonal line that runs from bottom left to top right

| [39] | Kimberlin, C. L. (2008). Validity and Reliability of Measurement Instruments Used in Research. American Journal of Health-System Pharmacists, 65(1), 2276- 2284. |

[39]

. The P-P plot dots are almost drawn closer to the diagonal line, as can be seen in the image below. Thus, the supposition of normality is satisfied.

Figure 2. Normality test.

4.1.2. Heteroskedasticity Test

In regression analysis, a violation of the homoscedasticity postulation is known as heteroskedasticity. The assumption of homoscedasticity states that at all levels of the independent variable(s), the error term's crosswise difference is constant. But when the variance of the error term is not constant across all levels of the independent variables, it is known as heteroskedasticity

. The output comprises the Breusch-Pagan test findings. homoskedasticity is rejected, and heteroskedasticity is found if the p-value is less than the significance level (0.05). We refer to errors as heteroskedastic if they lack a continuous variance. The Breusch-Pagan/Cook-Weisberg test of heteroskedasticity was used to identify this issue in Stata 16 by using the hettest command. The Chi-square calculation was less than the table value, which claims that the error term has constant variance (homoskedastic), and was accepted. Therefore, there is no heteroskedasticity issue in this study, as evidenced by the Chi-square calculated (0.001) being less than the table value (0.05).

4.1.3. Multicollinearity Test

The almost perfect relationship between two variables is known as collinearity. Regression models are referred to as multicollinear when they contain numerous variables that have strong correlations with the independent variable, the dependent variable, and each other

| [73] | Young, D. S. (2017). Handbook of regression methods, CRC Press, Boca Raton, FL, 109-136. |

[73]

.

According to Field

| [29] | Field, A. (2008). Discovering statistics using SPSS (3rd ed). SAGE Publications Ltd. |

[29]

, there is a hint that a multi-collinearity issue exists if "multi-collinearity would be suspected if tolerance figures are below 0.10 or if VIF statistics are 10.0 or higher." To put it another way, the tolerance value should be more than 0.10 and the VIF value should be ˂ 10. There is no multi-collinearity between the independent variables in the model because, according to the coefficient output (Collinearity statistics) and the table below, the tolerance for each independent variable is greater than 0.10, and the VIF for independent variables is less than the limited value (10). Therefore, there is no multicollinearity issue with this data.

Table 1. Multicollinearity test table.

Variables | Collinearity Statistics |

Tolerance | VIF |

Regulatory environment | .972 | 1.028 |

Effect of ethical standards | .842 | 1.188 |

Legal and regulatory framework | .834 | 1.200 |

Financial interests | .873 | 1.145 |

Client pressures | .713 | 1.402 |

Source: Research Data (2024)

Correlation shows the strength the magnitude, and direction of the relationship with each other. The linear relationship between variables can be measured by the correlation coefficient (r), which is commonly called Pearson product-moment correlation. The table below shows the measures of correlation between the variables, which was adapted from (Weiliang et al. 2011).

Table 2. Reliability.

№ | Size of correlation | Interpretation |

1 | +/-.00 to +/-.19 | very weak |

2 | +/-.20 to +/-.39 | Weak |

3 | +/-.40 to +/-.59 | Moderate |

4 | +/-.60 to +/-.79 | Strong |

5 | +/-.80 to +/- 1.00 | very strong |

Source: Weiliang et al. 2011

4.2. Correlations Analysis

Several important findings may be drawn from the correlation analysis of the variables of the legal and regulatory framework, ethical standards, financial interests, client demands, and the independence of external auditors. The regulatory environment and the independence of external auditors have a positive and significant relation (r = 0.331, p < 0.01). This implies that a greater impression of auditor independence is linked to a more robust regulatory framework. This result lends credibility to the idea that strong laws can support and preserve the independence of auditors. The independence of external auditors and ethical standards have a satisfactory and significant relationship (r = 0.368, p < 0.01). This suggests that a greater sense of auditor independence is related to a stronger adherence to ethical standards. This result emphasizes how crucial moral conduct and values are to preserving the independence of auditors. The independence of external auditors and the legal and regulatory framework have a positive and significant relationship (r = 0.441, p < 0.01). This suggests that a stronger sense of auditor independence is related to a strong legal and regulatory environment. This research implies that policies that are both effective and transparent can support the preservation of auditor independence. Financial interests and the independence of external auditors are positively and significantly correlated (r = 0.472, p < 0.01). This implies that auditor independence may be impacted by a perceived conflict between financial interests and independence. Client pressures and the independence of external auditors are positively and significantly correlated (r = 0.608, p < 0.01). This suggests that the independence of auditors can be significantly impacted by client pressure. The results of this study demonstrate the interdependence and impact of these variables on the independence of auditors.

Table 3. Correlation table.

S.№ | | 1 | 2 | 3 | 4 | 5 | 6 |

1 | Regulatory environment | 1 | | | | | |

2 | Effect of ethical standards | .441 | 1 | | | | |

3 | Legal and regulatory framework | .121 | .057 | 1 | | | |

4 | Financial interests | .419 | .626 | .613 | 1 | | |

5 | Client pressures | .053 | .297 | .256 | .317 | 1 | |

6 | External Auditor's independence | .331** | .368** | .441** | .472** | .608** | 1 |

Source: Research Data (2024)

4.3. Model Summary

Based on the provided Model Summary table, blow R-Value or multiple correlation coefficient: The dependent variable and the independent variables (client pressures, regulatory environment, legal and regulatory framework, financial interests, and effect of ethical standard) have a significant positive association (R-value = 0.830). The coefficient of determination, or R-Square, is 0.688, indicating that the independent variables in the model account for 68.8% of the variance in the dependent variable. However, additional indicators not included in this study or model account for 31.2% of the explanation. Adjusted R-Square: The model may have a good fit and is not overfitting the data, as indicated by the Adjusted R-Square of 0.676. According to this model summary, the dependent variable is strongly and significantly influenced by the independent variables (client pressures, regulatory environment, legal and regulatory framework, financial interests, and effect of ethical standards), and the model fits the data well overall.

Table 4. Model summary table.

Model | R | R Square | Adjusted R Square |

1 | .830a | .688 | .676 |

Source: Research Data (2024)

4.4. ANOVA

The value of Significance (Sig.) is 0.000, indicating a lower degree of significance than the standard 0.05. This indicates that there is a statistically significant relationship between the independent variables and the dependent variable overall and that the regression model as a whole is statistically significant.

Table 5. ANOVA table.

ANOVAa |

Model | Sum of Squares | df | Mean Square | F | Sig. |

1 | Regression | 2.744 | 5 | .549 | 56.932 | .000b |

Residual | 1.243 | 129 | .010 | | |

Total | 3.987 | 134 | | | |

a. Dependent Variable: External Auditor's independence

b. Predictors: (Constant), Client pressures, Regulatory environment, Legal and regulatory framework, financial interests, Effect of ethical standards

Source: Research Data (2024)

4.5. Regression Analysis Results

The Sig. value for the Regulatory environment is p (0.009, <0.05), This means that the relationship between the Regulatory environment and the External Auditor's independence is statistically significant. The coefficient for the Regulatory environment is 0.028, which means that for every one-unit increase in the Regulatory environment, the External Auditor's independence is predicted to increase by 0.028 units, holding all other variables constant.

The Sig. value for the Effect of ethical standards is p (0.000, <0.05). This means that the relationship between the Effect of ethical standards and the External Auditor's independence is statistically significant.

The coefficient for the Effect of ethical standards is 0.097, which means that for every one-unit increase in the Effect of ethical standards, the External Auditor's independence is predicted to increase by 0.097 units.

The Sig. value for Legal and regulatory framework is (0.000 <0.05). This means that the relationship between Legal and regulatory framework and External Auditor's independence is statistically significant. The coefficient for the Legal and regulatory framework is 0.216, which means that for every one-unit increase in the Legal and regulatory framework, the External Auditor's independence is predicted to increase by 0.216 units.

The Sig. value for financial interests is p (0.000<0.05) which is less than the commonly used significance level of 0.05. This means that the relationship between financial interests and the External Auditor's independence is statistically significant.

The unstandardized coefficient for financial interests is 0.121, which means that for every one-unit increase in financial interests, the External Auditor's independence is predicted to increase by 0.121 units.

The Sig. value for Client pressures is 0.000 <0.05). This means that the relationship between Client pressures and External Auditor's independence is statistically significant. The coefficient for Client pressures is 0.184, which means that for every one-unit increase in Client pressures, the External Auditor's independence is predicted to increase by 0.184 units.

Table 6. Regression result table.

Coefficients |

Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig (P). |

B | Std. Error | Beta |

1 | (Constant) | 1.000 | .168 | | 5.960 | .000 |

Regulatory environment | .028 | .011 | .132 | 2.651 | .009 |

Effect of ethical standards | .097 | .015 | .343 | 6.401 | .000 |

Legal and regulatory framework | .216 | .025 | .466 | 8.650 | .000 |

Financial interests | .121 | .016 | .387 | 7.353 | .000 |

Client pressures | .184 | .042 | .257 | 4.419 | .000 |

a. Dependent Variable: External Auditor's independence

Source: Research Data (2024)

5. Findings, Conclusion, and Recommendations

5.1. Findings

The findings show that the regulatory environment and the external Auditor's independence suggest that the regulatory environment has a meaningful impact on the independence of external auditors.

The statistically significant relationship between the effect of ethical standards and external auditors' independence highlights the importance of ethical considerations in maintaining auditor independence. This finding suggests that when ethical standards are effectively implemented and adhered to, external auditors are more likely to demonstrate independence in their judgments and decision-making processes.

The statistically significant relationship between the legal and regulatory framework and the external auditor's independence underscores the significance of a robust legal and regulatory system in promoting auditor independence. The finding suggests that when the legal and regulatory framework provides clear guidelines and enforces compliance, external auditors are more likely to act independently, free from undue influence.

The statistically significant relationship between financial interests and the External Auditor's independence indicates that financial considerations can impact auditor independence. This suggests that when auditors face conflicting financial interests or potential biases, their independence may be compromised. Effective safeguards and ethical guidelines are necessary to mitigate these risks and maintain independence.

The statistically significant relationship between Client pressures and External Auditor's independence highlights the potential influence of client demands and pressures on auditor independence. When auditors face significant pressures from clients, such as demands to overlook or manipulate financial information, their independence may be at risk. It emphasizes the need for auditors to maintain professional doubt and resist unwarranted influence to ensure independent and objective assessments.

5.2. Conclusions

Based on the findings, the researcher concluded that the regulatory environment and the independence of external auditors are significantly related. This suggests that a strong regulatory framework plays a crucial role in ensuring auditor independence. Additionally, the study emphasizes the importance of ethical standards in maintaining auditor independence, as the results indicate a significant relationship between ethical considerations and auditor independence.

Furthermore, the research highlights the significance of a strong legal and regulatory system in promoting auditor independence. When clear guidelines and enforcement mechanisms are in place, auditors are more likely to act independently and free from unnecessary influence. On the other hand, the study also reveals that financial interests can impact auditor independence, emphasizing the need for effective safeguards and ethical guidelines to mitigate the risks associated with conflicting financial interests.

Finally, the research underscores the potential influence of client pressures on auditor independence. When auditors face significant demands or pressures from clients, their independence may be compromised. To ensure independent and objective assessments, auditors must maintain professional doubt and resist unnecessary influence.

In conclusion, the findings suggest that a combination of a strong regulatory framework, adherence to ethical standards, effective safeguards against financial interests, and resistance to client pressures are crucial in maintaining the independence of external auditors.

5.3. Recommendations

It is recommended that regulatory bodies continue to strengthen and enforce the regulatory framework for external auditors. This includes ensuring clear guidelines, monitoring compliance, and implementing appropriate sanctions for non-compliance. Additionally, regular reviews and updates of the regulatory environment should be conducted to address any emerging challenges and maintain the independence of external auditors.

To maintain auditor independence, it is crucial to prioritize the implementation and adherence to ethical standards. This should be achieved through ongoing training and education to enhance auditors' understanding of ethical considerations and their implications for independence. Furthermore, ethical guidelines should be regularly reviewed and updated to reflect evolving industry practices and challenges.

It is recommended that countries or jurisdictions with weaker legal and regulatory systems focus on strengthening their framework. This can be achieved by establishing clear guidelines and enforcement mechanisms, promoting transparency and accountability, and ensuring appropriate penalties for non-compliance. Collaboration between regulatory bodies and professional accounting organizations should also help in developing a healthy legal and regulatory system.

To mitigate the impact of financial interests on auditor independence, it is important to implement effective safeguards and ethical guidelines. This may include establishing guidelines on financial relationships and conflicts of interest, requiring auditors to disclose any financial interests that may compromise their independence, and conducting regular reviews of auditors' financial relationships.

To address the potential influence of client pressures, auditors should receive training on how to handle such situations and maintain their independence. Communication channels should be established to report any undue influence or pressure from clients, ensuring that auditors feel supported and protected when facing such challenges. Additionally, professional accounting organizations and regulatory bodies should collaborate to develop guidelines and best practices for dealing with client pressures.