The Indian and Singaporean real estate markets are among the top investment destinations in the Asia-Pacific region, attracting significant foreign equity investments. This study provides a comparative analysis of the financial performance drivers of top real estate companies in India and Singapore. Through statistical analysis, key differences in financial structures, capital utilization, and profitability drivers were identified. The findings reveal that Return on Capital Employed (ROCE) significantly influences net profitability in both markets, though other financial ratios exhibit varying impacts. For Indian real estate firms, stock turnover ratio and debtor turnover ratio are critical determinants of financial performance, whereas for Singaporean firms, liquidity management (current ratio) and macroeconomic conditions (inflation) play a more significant role. The study also highlights that Indian firms maintain a more balanced capital structure, while Singaporean companies exhibit higher leverage and operational efficiency. Moreover, statistical tests indicate that the mean differences in net profitability ratio, current ratio, debt-to-capital employed ratio, and creditors' turnover ratio between Indian and Singaporean real estate companies are insignificant. However, significant differences exist in debt-equity ratio, stock turnover ratio, debtor turnover ratio, and ROCE. While FDI growth rates are comparable between the two countries, inflation rates vary significantly, impacting investment decisions and cost structures. The study suggests that Indian firms should enhance inventory turnover and debtor management, whereas Singaporean firms should optimize leverage and capital efficiency. Policymakers in India should focus on transparent debt management practices, while Singaporean authorities should regulate high leverage levels to mitigate financial risks. Future research should incorporate a broader dataset, including commercial and residential real estate segments, and analyze the impact of additional macroeconomic factors such as interest rates, housing demand, and government policies. These insights offer valuable recommendations for companies, investors, and policymakers to strengthen financial stability and improve market competitiveness in the real estate sector of India and Singapore.

| Published in | International Journal of Accounting, Finance and Risk Management (Volume 10, Issue 2) |

| DOI | 10.11648/j.ijafrm.20251002.12 |

| Page(s) | 94-110 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

India, Singapore, Real Estate, Profitability, GDP, Inflation, Financial Variables, Return on Capital Employed

Company | Statistics | Profitability Ratio | Current ratio | Debt Equity Ratio | Debt Capital Employed | Stock Turnover | Debtors Turnover | Creditors Turnover | ROCE |

|---|---|---|---|---|---|---|---|---|---|

DLF | Mean | 0.32 | 5.79 | 0.707 | 0.74 | 0.37 | 27.45 | 4.34 | 0.02 |

Median | 0.28 | 2.22 | 0.27 | 0.30 | 0.37 | 17.63 | 4.05 | 0.02 | |

Std Deviation | 0.22 | 9.38 | 1.4 | 1.45 | 0.09 | 28.65 | 1.93 | 0.014 | |

Macrotech | Mean | 0.02 | 1.34 | 0.16 | 0.26 | 0.28 | 12.7 | 0.91 | 0.006 |

Median | 0.02 | 1.4 | 0.18 | 0.25 | 030 | 12.5 | 0.17 | 0.005 | |

Std Deviation | 0.07 | 0.20 | 0.06 | 0.24 | 0.04 | 2.86 | 0.35 | 0.013 | |

Godrej Properties | Mean | 0.11 | 1.54 | 0.16 | 0.21 | 0.77 | 6.89 | 0.36 | 0.019 |

Median | 0.16 | 1.42 | 0.16 | 0.26 | 0.58 | 5.36 | 0.32 | 0.02 | |

Std Deviation | 0.12 | 0.54 | 0.14 | 0.14 | 0.67 | 4.76 | 0.23 | 0.017 |

Company | Statistics | Profitability Ratio | Current ratio | Debt Equity Ratio | Debt Capital Employed | Stock Turnover | Debtors Turnover | Creditors Turnover | ROCE |

|---|---|---|---|---|---|---|---|---|---|

CapitaLand | Mean | 0.11 | 1.05 | 7.67 | 0.87 | 0.82 | 2.01 | 1.03 | 0.40 |

Median | 01.6 | 1.12 | 7.39 | 0.88 | 0.79 | 2.07 | 0.96 | 0.22 | |

Std Deviation | 0.27 | 0.35 | 2.15 | 0.02 | 0.09 | 01.4 | 0.14 | 0.54 | |

UOL Group | Mean | 0.44 | 2.27 | 2.51 | 0.68 | 1167.2 | 9.13 | 6.96 | 0.22 |

Median | 0.32 | 2.01 | 2.38 | 0.70 | 809.06 | 6.48 | 5.22 | 0.16 | |

Std Deviation | 0.29 | 0.911 | 0.97 | 0.10 | 1269.9 | 4.78 | 8.3 | 01.2 | |

Fraser Property | Mean | 0.29 | 1.87 | 7.10 | 0.86 | 730.13 | 6.39 | 1.88 | 0.13 |

Median | 0.28 | 1.83 | 6.64 | 0.86 | 772.5 | 6.41 | 2.06 | 0.10 | |

Std Deviation | 0.11 | 0.57 | 2.6 | 0.05 | 221.79 | 2.23 | 0.79 | 0.09 |

S. No | Hypothesis | P Value | Interpretation |

|---|---|---|---|

1 | Ho:- Mean of net profitability ratio of the top Indian real estate companies according to market capitalisation is equal to top Singapore real estate companies Ha:- Mean of net profitability ratio for top Indian real estate companies according to market capitalisation is not equal to top Singapore real estate companies | 0.10 | Fail to reject the null hypothesis |

2 | Ho:- Mean of current ratio for top Indian real estate companies according to market capitalisation is equal to top Singapore real estate companies Ha:- Mean of current ratio for top Indian real estate companies according to market capitalisation is not equal to top Singapore real estate companies | 0.19 | Fail to reject the null hypothesis |

3 | Ho:- Mean of debt equity ratio for top Indian real estate companies according to market capitalisation is equal to top Singapore real estate companies according to market capitalisation Ha:- Mean of debt equity ratio for top Indian real estate companies according to market capitalisation is not equal to top Singapore real estate companies | 0.00 | Reject null hypothesis |

4 | Ho:- Mean of debt to capital employed ratio for top Indian real estate companies according to market capitalisation is equal to top Singapore real estate companies Ha:- Mean of debt to capital employed ratio for top Indian real estate companies according to market capitalisation is not equal to top Singapore real estate companies | 0.30 | Fail to reject the null hypothesis |

5 | Ho:- Mean of stock turnover ratio for top Indian real estate companies according to market capitalisation is equal to top Singapore real estate companies Ha:- Mean of stock turnover ratio for top Indian real estate companies according to market capitalisation is not equal to top Singapore real estate companies | 0.00 | Reject the null hypothesis |

6 | Ho:- Mean of debtors turnover ratio for top Indian real estate companies according to market capitalisation is equal to top 3 Singapore real estate companies Ha:- Mean of debtors turnover ratio for top Indian real estate companies according to market capitalisation is not equal to top 3 Singapore real estate companies | 0.01 | Reject the null hypothesis |

7 | Ho:- Mean of creditors turnover ratio for top Indian real estate companies according to market capitalisation is equal to top Singapore real estate companies Ha:- Mean of creditors turnover ratio for top Indian real estate companies according to market capitalisation is not equal to top Singapore real estate companies | 0.10 | Fail to reject the null hypothesis |

8 | Ho:- Mean of return on capital employed (ROCE) for top Indian real estate companies according to market capitalisation is equal to top Singapore real estate companies Ha:- Mean of return on capital employed (ROCE) for top Indian real estate companies according to market capitalisation is not equal to top Singapore real estate companies | 0.00 | Reject the null hypothesis |

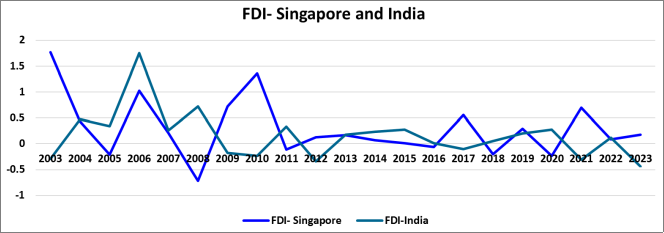

9 | Ho:- Mean of FDI growth rate of Singapore is equal to FDI growth rate of India Ha:- Mean of FDI growth rate of Singapore is not equal to FDI growth rate of India | 0.10 | Fail to reject the null hypothesis |

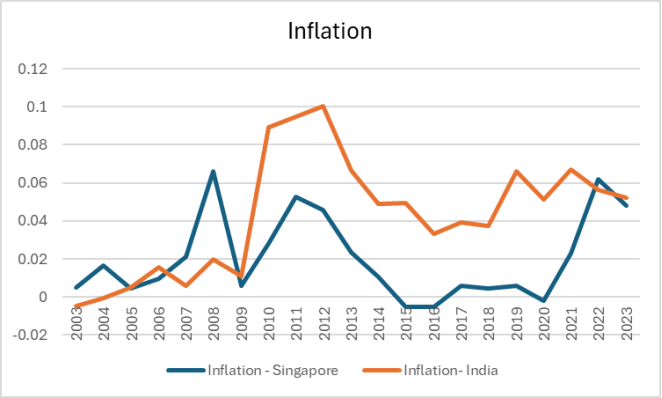

10 | Ho:- Mean of inflation rate of Singapore is equal to inflation rate of India Ha:- Mean of inflation rate of Singapore is not equal to inflation rate of India | 0.00 | Reject the null hypothesis |

S. No | Hypothesis | Equation |

|---|---|---|

1 | Ho:- ROCE does not significantly impacts net profitability ratio of top Indian real estate companies as per market capitalisation Ha:- ROCE significantly impacts net profitability ratio of top Indian real estate companies as per market capitalisation | Net Profit Ratio = C+ β(ROCE) + β (Current Ratio) + β (Creditors turnover ratio) + β (stock turnover ratio) + β (Inflation) + β (FDI growth rate) |

2 | Ho:- Net profit ratio does not significantly impacts ROCE of top Indian real estate companies as per market capitalisation Ha:- Net profit ratio significantly impacts ROCE of top Indian real estate companies as per market capitalisation | ROCE = C + β(Net Profi)t + β(Stock) + β (Debtors) + β (Creditors) + β (FDI) + β (Inflation) |

3 | Ho:- ROCE does not significantly impacts net profitability ratio of top Singapore real estate companies as per market capitalisation Ha:- ROCE significantly impacts net profitability ratio of top Singapore real estate companies as per market capitalisation | Net Profit Ratio = C+ β(ROCE) + β (Current Ratio) + β (Creditors turnover ratio) + β (stock turnover ratio) + β (Inflation) + β (FDI growth rate) |

4 | Ho:- Net profit ratio does not significantly impacts ROCE of top Singapore real estate companies as per market capitalisation Ha:- Net profit ratio significantly impacts ROCE of top Singapore real estate companies as per market capitalisation | ROCE = C + β(Net Profi)t + β(Stock) + β (Debtors) + β (Creditors) + β (GDP) + β (FDI growth rate) |

S. No | Hypothesis | P Value | Interpretation | Equation | Significant Variables | Adj R Square |

|---|---|---|---|---|---|---|

1 | Ho: - ROCE does not significantly impacts net profitability ratio of top Indian real estate companies as per market capitalisation Ha:- ROCE significantly impacts net profitability ratio of top Indian real estate companies as per market capitalisation | 0 | ROCE is significantly impacted by net profitability ratio of top Indian real estate companies as per market capitalisation | Net Profit Ratio = (0.05) C + 13.73 (ROCE) +).0019 (Current Ratio) - 0.0146 (Creditors Turnover Ratio) - 0.30 (Stock Turnover ratio) +0.58 (Inflation) +0.06 (FDI Growth) + Error | ROCE and Stock Turnover Ratio (Table A1) | 0.79 |

2 | Ho:- Net profit ratio does not significantly impacts ROCE of top Indian real estate companies as per market capitalisation Ha:- Net profit ratio significantly impacts ROCE of top Indian real estate companies as per market capitalisation | 0.00 | For top Indian real estate companies as per market capitalisation Net profit ratio gets significantly impacted by ROCE | ROCE = (-0.002) C + 0.05 (Net profit ratio) + 0.02 (Stock Turnover Ratio) + 0.00018 (Debtors turnover ratio) + 0.0010 (Creditors Turnover Ratio) - 0.001 (FDI Growth) - 0.05 (Inflation) | Net Profit Ratio, Stock Turnover Ratio, Debtors Turnover Ratio, Creditors Turnover ratio(Table A2) | 0.89 |

3 | Ho: - ROCE does not significantly impacts net profitability ratio of top Singapore real estate companies as per market capitalisation Ha:- ROCE significantly impacts net profitability ratio of top Singapore real estate companies as per market capitalisation | 0.03 | For top Singapore real estate companies as per market capitalisation ROCE significantly gets impacted by net profitability ratio | Net profit ratio = -0.03 (C) +0.57 (ROCE)+0.11 (Current Ratio)-0.004 (Creditors Turnover ratio) +0.000003 (Stock turnover ratio)-0.1 (Inflation) +0.13 (FDI Growth) + Error | 0.25 | |

4 | Ho:- Net profit ratio does not significantly impacts ROCE of top Singapore real estate companies as per market capitalisation Ha:- Net profit ratio significantly impacts ROCE of top Singapore real estate companies as per market capitalisation | 0.04 | For top Singapore real estate companies as per market capitalisation Net profit ratio gets significantly impacted by ROCE | ROCE = .09 (C) +0.31 (Net Profit Ratio)+ 0.000(Stock Turnover Ratio)- 0.0045 (Debtors Turnover Ratio) - 0.004 (Creditors Turnover Ratio) -0.001 (FDI Growth) -+3.63 (Inflation) | Stock turnover ratio, debtors turnover ratio, creditors turnover ratio (Table A4) | 0.26 |

APAC | Asia-Pacific |

GDP | Gross Domestic Product |

ROCE | Return On Capital Employed |

HPEC | High Powered Expert Committee |

CBRE | Coldwell Banker Richard Ellis |

HDB | Housing Development Board |

RBF | Radial Basis Function |

PF | Project Financing |

DLF | Delhi Land & Finance |

P Value | Probability Value |

ADF | Augmented Dickey Fuller |

VIF | Variance Inflation Factor |

Dependent Variable: NET_PROFITABILITY_RATIO | ||||

|---|---|---|---|---|

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

C | 0.052552 | 0.078583 | 0.668746 | 0.5121 |

ROCE | 13.73136 | 1.485824 | 9.241577 | 0.0000 |

CURRENT_RATIO | 0.001976 | 0.003378 | 0.585045 | 0.5658 |

CREDITORS_TURNOVER_RATIO | -0.014636 | 0.009762 | -1.499301 | 0.1511 |

STOCK_TURNOVER_RATIO | -0.302496 | 0.073955 | -4.090293 | 0.0007 |

FDI_GROWTH_RATE | 0.061414 | 0.082411 | 0.745218 | 0.4658 |

INFLATION | 0.582705 | 1.442778 | 0.403877 | 0.6911 |

R-squared | 0.842701 | Mean dependent var | 0.257803 | |

Adjusted R-squared | 0.790268 | S.D. dependent var | 0.222695 | |

S.E. of regression | 0.101987 | Akaike info criterion | -1.496454 | |

Sum squared resid | 0.187223 | Schwarz criterion | -1.155169 | |

Log likelihood | 25.70567 | Hannan-Quinn criter. | -1.401796 | |

F-statistic | 16.07198 | Durbin-Watson stat | 1.670589 | |

Prob(F-statistic) | 0.000002 | |||

Dependent Variable: ROCE | ||||

|---|---|---|---|---|

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

C | -0.002506 | 0.004029 | -0.621956 | 0.5418 |

NET_PROFITABILITY_RATIO | 0.056235 | 0.005158 | 10.90348 | 0.0000 |

STOCK_TURNOVER_RATIO | 0.021117 | 0.003699 | 5.709429 | 0.0000 |

DEBTORS_TURNOVER_RATIO | 0.000185 | 5.00E-05 | 3.698640 | 0.0016 |

CREDITORS_TURNOVER_RATIO | 0.001013 | 0.000478 | 2.118459 | 0.0483 |

INFLATION | -0.053858 | 0.068186 | -0.789869 | 0.4399 |

FDI_GROWTH_RATE | -0.001067 | 0.004319 | -0.247135 | 0.8076 |

R-squared | 0.918616 | Mean dependent var | 0.024058 | |

Adjusted R-squared | 0.891488 | S.D. dependent var | 0.015949 | |

S.E. of regression | 0.005254 | Akaike info criterion | -7.428265 | |

Sum squared resid | 0.000497 | Schwarz criterion | -7.086979 | |

Log likelihood | 99.85331 | Hannan-Quinn criter. | -7.333607 | |

F-statistic | 33.86238 | Durbin-Watson stat | 1.854382 | |

Prob(F-statistic) | 0.000000 | |||

Dependent Variable: NET_PROFITABILITY_RATIO | ||||

|---|---|---|---|---|

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

C | -0.038172 | 0.124026 | -0.307773 | 0.7604 |

ROCE | 0.576901 | 0.216284 | 2.667331 | 0.0122 |

CURRENT_RATIO | 0.116875 | 0.049023 | 2.384076 | 0.0236 |

CREDITORS_TURNOVER_RATIO | -0.004792 | 0.006679 | -0.717438 | 0.4787 |

STOCK_TURNOVER_RATIO | 3.67E-05 | 3.98E-05 | 0.922437 | 0.3637 |

INFLATION | -0.108669 | 2.061582 | -0.052711 | 0.9583 |

FDI__US$_BILLION_ | 0.137041 | 0.083997 | 1.631495 | 0.1132 |

R-squared | 0.376229 | Mean dependent var | 0.361592 | |

Adjusted R-squared | 0.251475 | S.D. dependent var | 0.269326 | |

S.E. of regression | 0.233014 | Akaike info criterion | 0.093219 | |

Sum squared resid | 1.628862 | Schwarz criterion | 0.397988 | |

Log likelihood | 5.275441 | Hannan-Quinn criter. | 0.200664 | |

F-statistic | 3.015761 | Durbin-Watson stat | 1.891881 | |

Prob(F-statistic) | 0.019899 | |||

Dependent Variable: ROCE | ||||

|---|---|---|---|---|

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

C | 0.093516 | 0.077309 | 1.209634 | 0.2359 |

NET_PROFITABILITY_RATIO | 0.314066 | 0.119651 | 2.624847 | 0.0135 |

STOCK_TURNOVER_RATIO | -1.25E-05 | 3.00E-05 | -0.416416 | 0.6801 |

DEBTORS_TURNOVER_RATIO | -0.004570 | 0.007575 | -0.603331 | 0.5508 |

CREDITORS_TURNOVER_RATIO | -0.004602 | 0.005162 | -0.891501 | 0.3798 |

INFLATION | 3.630322 | 1.442099 | 2.517387 | 0.0174 |

FDI__US$_BILLION_ | -0.000988 | 0.066251 | -0.014906 | 0.9882 |

R-squared | 0.383094 | Mean dependent var | 0.215901 | |

Adjusted R-squared | 0.259713 | S.D. dependent var | 0.206330 | |

S.E. of regression | 0.177527 | Akaike info criterion | -0.450735 | |

Sum squared resid | 0.945470 | Schwarz criterion | -0.145967 | |

Log likelihood | 15.33861 | Hannan-Quinn criter. | -0.343290 | |

F-statistic | 3.104962 | Durbin-Watson stat | 2.016036 | |

Prob(F-statistic) | 0.017375 | |||

| [1] | Choi, A., & Hyland, G. (2025). 2025 Asia Pacific Investor Intentions Survey. In |

| [2] | Chuang, Z., & Min, P. (2022). Real Estate Tax Reform, Economic Growth and Financial Stability. China Finance and Economic Review, 11(1), 89-112. |

| [3] | Discover Key Insights into the Indian Real Estate Sector in 2024. (n.d.). India Brand Equity Foundation. Retrieved February 6, 2025, from |

| [4] | Edison, J. C. (2017). Financial analysis of the real estate industry in India. Journal of Business and Economic Development, 2(1), 44. |

| [5] | Fan, W., He, Y., Hao, L., & Wu, F. (2024). Do high house prices promote the development of China’s real economy? Empirical evidence based on the decomposition of real estate price. PLoS ONE, 19(1), e0295311. |

| [6] | Gill, A., 1, Herbert, G. D., 1, Mand, H. S., 2, Sharma, S. P., 3, & Mathur, N., 4. (2012). Factors that Influence Indian Propensity to Invest in the Real Estate Market [Journal-article]. Journal of Finance and Investment Analysis, vol. 1 (no. 2), 137-156. |

| [7] | Guo, J., Hao, A., & Ren, Y. (2014). Design optimization of real estate tax and effect analysis in China. Journal of Industrial Engineering and Management, 7(2). |

| [8] |

India population (2025) - Worldometer. (n.d.). Retrieved February 6, 2025, from

https://www.worldometers.info/world-population/india-population/ |

| [9] | Issah, M., & Antwi, S. (2017). Role of macroeconomic variables on firms’ performance: Evidence from the UK. Cogent Economics & Finance, 5(1), 1405581. |

| [10] | India: leading real estate companies by market capitalization 2024 | Statista. (2024, August 30). Statista. |

| [11] | Jianyu, G., Wenzhi, P., Mingqing, J., & Dong, Z. (2022). Construction of real estate debt crisis early warning model based on RBF neural network. Security and Communication Networks, 2022, 1-8. |

| [12] | KPMG Assurance and Consulting Services LLP, Bansal, N., KPMG Assurance and Consulting Services LLP, Hari, & KPMG Assurance and Consulting Services LLP. (2024). Navigating the dynamics of real estate in India. |

| [13] | KRAJNAKOVA, E., JEGELAVICIUTE, R., & NAVICKAS, V. (2018). THE ECONOMIC FACTORS INFLUENCE ON REAL ESTATE MARKET DEVELOPMENT. JOURNAL OF INTERDISCIPLINARY RESEARCH, 8(2). |

| [14] | Li, J., Ji, J., Guo, H., & Chen, L. (2018). Research on the influence of real estate development on private investment: A case study of China. Sustainability, 10(8), 2659. |

| [15] | Li, P., Wang, Y., Zhang, L., & Zhang, X. (2024). China’s GDP at risk: The role of housing prices. The Journal of Finance and Data Science, 10. |

| [16] | Liow, K. H. (2004). Corporate real estate and stock market performance. The Journal of Real Estate Finance and Economics, 29(1), 119-140. |

| [17] | Liu, F., Ren, H., Liu, C., & Tan, D. (2022). Formation of Financial Real Estate Risks and Spatial Interactions: Evidence from 35 Cities in China. Journal of Risk and Financial Management, 15(12), 576. |

| [18] | Manganelli, B., Morano, P., Rosato, P., & De Paola, P. (2020). The effect of taxation on investment demand in the real estate market: the Italian experience. Buildings, 10(7), 115. |

| [19] | Matysiak, G., & Fuerst, F. (2009). Analyzing the Performance of Non-Listed Real Estate Funds: A panel data analysis. SSRN Electronic Journal. |

| [20] |

MACROTRENDS. (2025a, January 31). India Foreign Direct Investment 1970-2025.

https://www.macrotrends.net/global-metrics/countries/ind/india/foreign-direct-investment |

| [21] |

MACROTRENDS. (2025b, January 31). India inflation rate 1960-2025.

https://www.macrotrends.net/global-metrics/countries/IND/india/inflation-rate-cpi |

| [22] | Mehta, N. (2021). The Study of Relationship Between FDI and Stock Market and The Real Estate Sector. Turkish Journal of Computer and Mathematics Education, 12(12), 3131-3141. |

| [23] | Mitra, G., Gupta, V., & Gupta, G. (2023). Impact of macroeconomic factors on firm performance: Empirical evidence from India. Investment Management and Financial Innovations, 20(4), 1-12. |

| [24] | Phuong, L. L., & Quynh, A. N. (2024). IMPACTS OF MACROECONOMIC FACTORS ON REAL ESTATE BUBBLE IN VIETNAM’S BIG CITIES WITH INDUSTRIAL ZONES. International Journal of Economics and Business Research, 27(3). |

| [25] |

Prasad, S., & Gupta, P. (2023, May 18). India High on Investor’s Agenda - Colliers India. Retrieved February 6, 2025, from

https://www.colliers.com/en-in/news/press-release-india-high-on-investors-agenda |

| [26] | RealEstate, E. (2025, January 10). Singapore, US and Canada dominate foreign investments in Indian real estate market in 2024: Report. ETRealty.com. |

| [27] | Reporter, B. (2024, November 6). Banking on bricks: The real story behind India’s real estate boom. |

| [28] | Ro, S., Lee, J., & Kim, D. (2024). The dark side of project financing: leverage, CEO overconfidence, and sustainability challenges in the construction sector. Sustainability, 17(1), 16. |

| [29] | Rzeszut, S. J., Kowalski, M. J., & Kazak, J. K. (2023). Financial efficiency and investor behavior on the European real estate market in the rising inflation environment. Real Estate Management and Valuation, 32(1), 71-83. |

| [30] | Salah, M., Faisal-E-Alam, M., Kader, A., Imran, M., & Beg, T. H. (2022). FINANCIAL PERFORMANCE EVALUATION THROUGH RATIO ANALYSIS: A STUDY ON RURAL POWER COMPANY LTD. International Journal of Business and Management Future, 9-18. |

| [31] | Sanchaniya, R. J., Sanchaniya, J. V., & Bhalodi, P. P. (2023). Comparative analysis of the Indian and Canadian real estate markets. Baltic Journal of Real Estate Economics and Construction Management, 11(1), 1-13. |

| [32] | Shishir Baijal & Ashwani Awasthi. (2023). Skilled employment in construction sector in India. In Knight Frank India. |

| [33] |

Singapore real estate companies - top company list. (n.d.).

https://www.mordorintelligence.com/industry-reports/singapore-real-estate-market/companies |

| [34] | Singapore Real Estate Market Size & Trends. (2025). In |

| [35] | Stanković, D. (2022). Analysis of the impact of macroeconomic factors on real estate prices in Bosnia And Herzegovina. Economics, 10(2), 147-160. |

| [36] |

Statista. (2024, November 28). Inflation rate in Singapore 2029.

https://www.statista.com/statistics/379423/inflation-rate-in-singapore/ |

| [37] | Statista. (n.d.-a). Real Estate - India | Statista market forecast. Retrieved February 6, 2025, from |

| [38] |

Statista. (n.d.-b). Real Estate - Singapore | Statista market forecast. Retrieved February 6, 2025, from

https://www.statista.com/outlook/fmo/real-estate/singapore#value |

| [39] |

Statista. (2024a, July 4). Urbanization in India 2023. Retrieved February 6, 2025, from

https://www.statista.com/statistics/271312/urbanization-in-india/ |

| [40] |

Statista. (2024b, November 8). Gross domestic product (GDP) in Singapore 2029. Retrieved February 6, 2025, from

https://www.statista.com/statistics/378648/gross-domestic-product-gdp-in-singapore/ |

| [41] |

Statista. (2025, January 10). Gross domestic product (GDP) in India 2029. Retrieved February 6, 2025, from

https://www.statista.com/statistics/263771/gross-domestic-product-gdp-in-india/ |

| [42] | Tajani, F., Morano, P., Saez-Perez, M. P., Di Liddo, F., & Locurcio, M. (2019). Multivariate dynamic analysis and Forecasting Models of future property bubbles: Empirical applications to the housing markets of Spanish metropolitan cities. Sustainability, 11(13), 3575. |

| [43] | Terterashvili, N., & Shaburishvili, S. (2023). A STUDY OF THE FACTORS AFFECTING THE REAL ESTATE MARKET WITH a MACROECONOMIC CONTEXT. Zenodo (CERN European Organization for Nuclear Research). |

| [44] | Top 64 largest Singaporean Real Estate Companies 2025. (n.d.). Disfold. Retrieved February 7, 2025, from |

| [45] | India population (2025) - Worldometer. (n.d.). |

| [46] | World Bank Open Data. (n.d.). World Bank Open Data. |

| [47] | Zhang, R., & Pang, Y. (2024). The role of digital inclusive finance in weakening real estate market speculation. Buildings, 14(5), 1306. |

| [48] | Zubairu, I., Akeba Atiawin, P., Jamal Iddrisu, A., & Amoako Amanquah, B. (2025). Assessing the effects of macroeconomic factors on the financial performance of Ghanaian listed manufacturing companies. International Journal of Accounting, Finance and Risk Management, 10(1), 23-41. |

APA Style

Denzongpa, S. G. D., Shrivastava, N. (2025). Drivers of Financial Performance of Top Real Estate Companies in India and Singapore - A Comparative Analysis. International Journal of Accounting, Finance and Risk Management, 10(2), 94-110. https://doi.org/10.11648/j.ijafrm.20251002.12

ACS Style

Denzongpa, S. G. D.; Shrivastava, N. Drivers of Financial Performance of Top Real Estate Companies in India and Singapore - A Comparative Analysis. Int. J. Account. Finance Risk Manag. 2025, 10(2), 94-110. doi: 10.11648/j.ijafrm.20251002.12

@article{10.11648/j.ijafrm.20251002.12,

author = {Sonam Gyaltsen Dorjee Denzongpa and Neharika Shrivastava},

title = {Drivers of Financial Performance of Top Real Estate Companies in India and Singapore - A Comparative Analysis

},

journal = {International Journal of Accounting, Finance and Risk Management},

volume = {10},

number = {2},

pages = {94-110},

doi = {10.11648/j.ijafrm.20251002.12},

url = {https://doi.org/10.11648/j.ijafrm.20251002.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijafrm.20251002.12},

abstract = {The Indian and Singaporean real estate markets are among the top investment destinations in the Asia-Pacific region, attracting significant foreign equity investments. This study provides a comparative analysis of the financial performance drivers of top real estate companies in India and Singapore. Through statistical analysis, key differences in financial structures, capital utilization, and profitability drivers were identified. The findings reveal that Return on Capital Employed (ROCE) significantly influences net profitability in both markets, though other financial ratios exhibit varying impacts. For Indian real estate firms, stock turnover ratio and debtor turnover ratio are critical determinants of financial performance, whereas for Singaporean firms, liquidity management (current ratio) and macroeconomic conditions (inflation) play a more significant role. The study also highlights that Indian firms maintain a more balanced capital structure, while Singaporean companies exhibit higher leverage and operational efficiency. Moreover, statistical tests indicate that the mean differences in net profitability ratio, current ratio, debt-to-capital employed ratio, and creditors' turnover ratio between Indian and Singaporean real estate companies are insignificant. However, significant differences exist in debt-equity ratio, stock turnover ratio, debtor turnover ratio, and ROCE. While FDI growth rates are comparable between the two countries, inflation rates vary significantly, impacting investment decisions and cost structures. The study suggests that Indian firms should enhance inventory turnover and debtor management, whereas Singaporean firms should optimize leverage and capital efficiency. Policymakers in India should focus on transparent debt management practices, while Singaporean authorities should regulate high leverage levels to mitigate financial risks. Future research should incorporate a broader dataset, including commercial and residential real estate segments, and analyze the impact of additional macroeconomic factors such as interest rates, housing demand, and government policies. These insights offer valuable recommendations for companies, investors, and policymakers to strengthen financial stability and improve market competitiveness in the real estate sector of India and Singapore.},

year = {2025}

}

TY - JOUR T1 - Drivers of Financial Performance of Top Real Estate Companies in India and Singapore - A Comparative Analysis AU - Sonam Gyaltsen Dorjee Denzongpa AU - Neharika Shrivastava Y1 - 2025/03/21 PY - 2025 N1 - https://doi.org/10.11648/j.ijafrm.20251002.12 DO - 10.11648/j.ijafrm.20251002.12 T2 - International Journal of Accounting, Finance and Risk Management JF - International Journal of Accounting, Finance and Risk Management JO - International Journal of Accounting, Finance and Risk Management SP - 94 EP - 110 PB - Science Publishing Group SN - 2578-9376 UR - https://doi.org/10.11648/j.ijafrm.20251002.12 AB - The Indian and Singaporean real estate markets are among the top investment destinations in the Asia-Pacific region, attracting significant foreign equity investments. This study provides a comparative analysis of the financial performance drivers of top real estate companies in India and Singapore. Through statistical analysis, key differences in financial structures, capital utilization, and profitability drivers were identified. The findings reveal that Return on Capital Employed (ROCE) significantly influences net profitability in both markets, though other financial ratios exhibit varying impacts. For Indian real estate firms, stock turnover ratio and debtor turnover ratio are critical determinants of financial performance, whereas for Singaporean firms, liquidity management (current ratio) and macroeconomic conditions (inflation) play a more significant role. The study also highlights that Indian firms maintain a more balanced capital structure, while Singaporean companies exhibit higher leverage and operational efficiency. Moreover, statistical tests indicate that the mean differences in net profitability ratio, current ratio, debt-to-capital employed ratio, and creditors' turnover ratio between Indian and Singaporean real estate companies are insignificant. However, significant differences exist in debt-equity ratio, stock turnover ratio, debtor turnover ratio, and ROCE. While FDI growth rates are comparable between the two countries, inflation rates vary significantly, impacting investment decisions and cost structures. The study suggests that Indian firms should enhance inventory turnover and debtor management, whereas Singaporean firms should optimize leverage and capital efficiency. Policymakers in India should focus on transparent debt management practices, while Singaporean authorities should regulate high leverage levels to mitigate financial risks. Future research should incorporate a broader dataset, including commercial and residential real estate segments, and analyze the impact of additional macroeconomic factors such as interest rates, housing demand, and government policies. These insights offer valuable recommendations for companies, investors, and policymakers to strengthen financial stability and improve market competitiveness in the real estate sector of India and Singapore. VL - 10 IS - 2 ER -

Kodaikanal International School, Dindigul, India

Global Research Hub, Bangalore, India

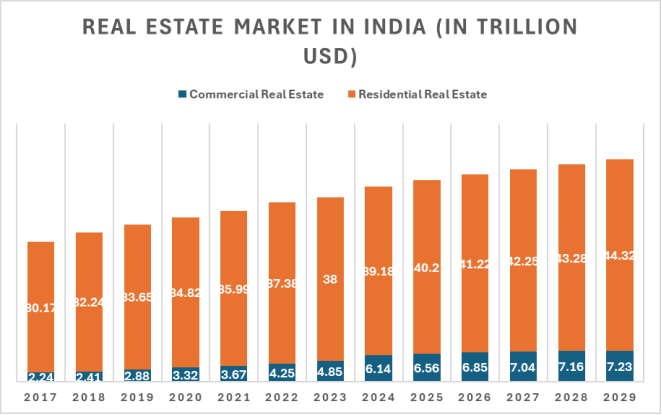

Figure 1. Real estate Market in India (In Trillion USD).

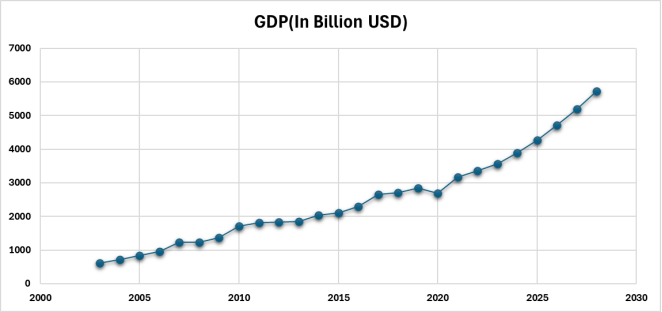

Figure 2. India’s GDP (In Billion USD).

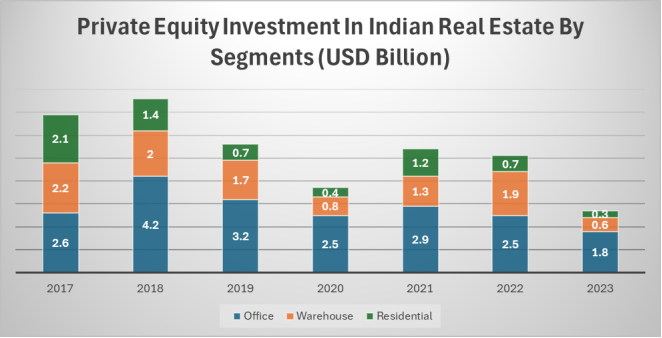

Figure 3. Private Equity Investment In Indian Real Estate By Segment (USD Billion).

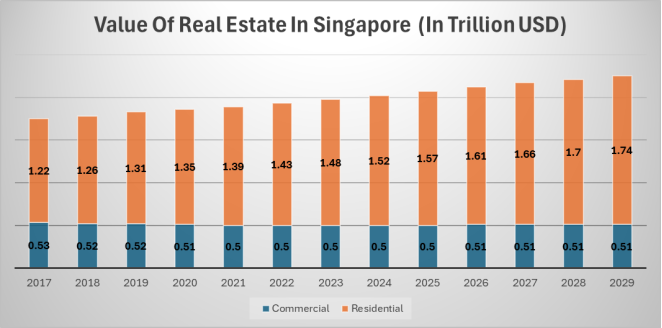

Figure 4. Value of Real Estate in Singapore (In Trillion USD).

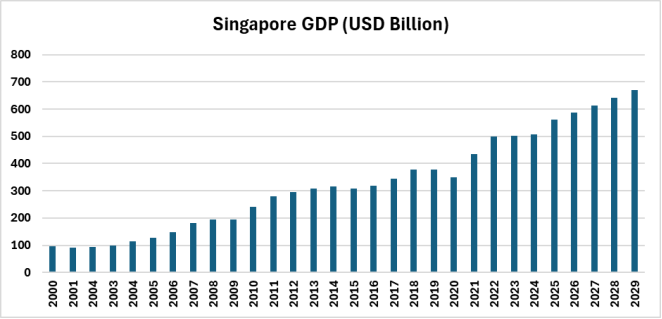

Figure 5. Singapore GDP (In USD Billion).

Figure 6. Inflation - India and Singapore.

Figure 7. FDI Growth - India and Singapore.

Information