The study was conducted at the time of increasing demand to provide insight into the role of financial technologies in inclusive economic growth among the South Asian economies. Even though there is a rapid growth in mobile financial services in the region, there is a dearth of comparative evidence on the role of such innovations in promoting the financial inclusion phenomenon in various countries situated in the SAARC region. Filling this gap, the study offers a timely insight into policies to be improved by policymakers, regulators, and financial institutions to improve digital finance strategies and enhance equitable access to financial systems. The paper analyses the mobile finance markets as a proportion of the total economy among SAARC countries, focusing on factors affecting financial inclusion. The data has been collected from WDI from 2012 to 2022, demonstrating one of the latest studies focused on SAARC nations regarding MFS and Financial inclusions. After cleaning the data, the indicators from Bangladesh, India, and Pakistan were retained to maintain the accuracy of the results derived from this study. Five indicators, such as financial inclusion, mobile money transactions, GDP growth rate, individuals using the internet, and the number of mobile cellular subscriptions, were adopted from earlier research to compare the MFS market. This study shows that MFS markets have grown significantly over the past decade. However, the growth of a few MFS indicators has been steady since 2020 due to COVID-19 and other global issues. The results of panel regression revealed that mobile money transactions and mobile cellular subscriptions have a significance in improving financial inclusion in SAARC nations. Therefore, this research offers significant perspectives for authorities and mobile financial service providers to use effective mobile money methods in order to attain higher levels of financial inclusion in SAARC countries.

| Published in | International Journal of Sustainability Management and Information Technologies (Volume 11, Issue 2) |

| DOI | 10.11648/j.ijsmit.20251102.12 |

| Page(s) | 76-90 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Mobile Financial Service, Financial Inclusion, Panel Data, SAARC

Country | Mobile Penetration | Internet Users | 4G Availability | 5G Rollout |

|---|---|---|---|---|

India | As of 2023, India has around 1.17 billion mobile subscribers, and mobile penetration is estimated to be around 84%. | India has over 850 million internet users, out of which the internet penetration stands at around 60%, making the country the second-largest internet market globally. | Chawla and Joshi found that 4G services are widely available and the coverage is about 98% of the population [10] . | In mid-2022, India started 5G services, and it will roll out further in the country. |

Bangladesh | Bangladesh has 182+ million mobile users with a mobile penetration rate of 110%, implying multiple SIM card usage. | Hasan stated that it boasts about 130 million internet users and an internet usage rate of 78% [2 1]. | There is a total availability of 4G services to approximately 90% of the population. | Bangladesh launched limited 5G services in late 2021, with plans for broader expansion. |

Pakistan | According to Kemal, Pakistan has approximately 195 million mobile subscribers, representing roughly 89% of the total population [2 7]. | Currently, there is internet user of 125 million and the Internet is accessible to 54% of the population. | Recently, it has been noted that the 4G services provide coverage for over 85% of the population. | 5G has not been launched in Pakistan yet and the country is in the initial phase of trial, though it is going to launch soon commercially. |

Sri-Lanka | Sri Lanka has approximately 30 million mobile users, with an estimated usage rate of 140%, a factor indicating multiple subscriptions. | It has about 11 million internet users, which is half of its population which making the internet penetration rate about 50%. | 4G services are also available, and it is said that they cover more than 95% of the population of the country. | di Castri marked that 5G is at the trial stage currently in Sri Lanka, with a commercial rollout soon [14] . |

Nepal | Currently, there are around 42 million users of mobile phones among the total population of Nepalese people, and the average Mobile phone penetration in Nepal is more than 140%, which shows that there is a high tendency of multiple SIM connections. | Pradhan and Dahal stated that it is shocking to learn that the internet users of Nepal are over 18 million and internet usage is at 60% of the population [4 1]. | Coverage of 4G services is some 85 per cent of the population. | Currently, Nepal has not started 5G services, but it has ventured into the trials of 5G. |

Afghanistan | As per Rahman et al., there are about 23 million mobile subscribers with a 60% mobile phone penetration [4 2]. | The country has about 10 million people with internet access, with internet usage being approximately 27%. | 4G services have been deployed mostly in large cities, and the penetration is estimated to be 50%. | Afghanistan has not started the 5G trial yet because of infrastructure and political problems. |

Bhutan | Bhutan has a total mobile user of approximately 800 million and it shows that the mobile penetration is around 108%. | It is estimated that there are about 700000 internet users, giving internet connectivity of roughly 90%. | The 4G services are widely spread, especially in the urban areas hence touching on the majority of the population. | Currently, Bhutan has not widely embraced 5G but has plans to in future, depending on its development. |

Maldives | Currently, there are approximately 900,000 mobile subscribers, and the mobile subscribers’ penetration is more than 200% in the Maldives, and which refers to multiple SIM usage. | Currently, an easily accessible internet is available in the country as it has nearly about 600000 internet users and the internet is highly penetrated to the extent of 120%. | Song et al. explained that 4G is offered in all the regions and even on the remote islands of the country [4 6]. | The Maldives introduced 5G services in 2020, with a wide coverage requirement being one of the first countries in the region to do so. |

Component | Eigenvalue | Difference | Proportion | Cumulative |

|---|---|---|---|---|

1 | 4.383 | 2.854 | 0.731 | 0.731 |

2 | 1.528 | 1.466 | 0.255 | 0.985 |

3 | 0.062 | 0.044 | 0.010 | 0.996 |

4 | 0.018 | 0.011 | 0.003 | 0.999 |

5 | 0.007 | 0.006 | 0.001 | 1 |

6 | 0.001 | 0.000 | 1 |

Variable | Obs | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

FI | 30 | 11.827 | 4.042 | 6.663 | 19.479 |

MM | 30 | 1780000000 | 1580000000 | 4.706 | 5300000000 |

GDP | 30 | 8.066 | 14.228 | -5.831 | 81.747 |

INT | 30 | 21.950 | 11.842 | 6.630 | 47.240 |

MCS | 30 | 466000000 | 453000000 | 117000000 | 1180000000. |

Variables | FI | MM | GDP | INT | MCS |

|---|---|---|---|---|---|

FI | 1 | ||||

MM | 0.447 | 1 | |||

GDP | 0.041 | -0.235 | 1 | ||

INT | 0.465 | 0.845 | 0.206 | 1 | |

MCS | 0.956 | 0.337 | -0.105 | 0.331 | 1 |

Variables | Coefficient | Std. Err. | z-Statistic | Prob. |

|---|---|---|---|---|

MM | 0.004 | 0.001 | 3.070 | 0.002 |

GDP | 0.003 | 0.014 | 1.850 | 0.065 |

MCS | 0.008 | 0.005 | 17.720 | 0.000 |

_cons | 7.093 | 0.365 | 19.430 | 0.000 |

CSR | Corporate Social Responsibility |

FI | Financial Inclusion |

MM | Mobile Money |

MCS | Mobile Cellular Subscriptions |

GDP | Gross Domestic Product |

INT | Internet Users |

PCA | Principal Component Analysis |

KMO | Kaiser |

Meyer | Olkin (Test for Sampling Adequacy) |

RE | Random Effects |

FE | Fixed Effects |

GLS | Generalized Least Squares |

SAARC | South Asian Association for Regional Cooperation |

WDI | World Development Indicators |

ICT | Information and Communication Technology |

SDG | Sustainable Development Goals |

WB | World Bank |

UN | United Nations |

ITU | International Telecommunication Union |

| [1] | Abdelghaffar, R. A., Emam, H. A., & Samak, N. A. (2023). Financial inclusion and human development: is there a nexus?. Journal of Humanities and Applied Social Sciences, 5(3), 163-177. |

| [2] | Afroze, D., & Rista, F. I. (2022). Mobile Financial Services (MFS) and Digital Inclusion – a Study on Customers’ Retention and Perceptions. Qualitative Research in Financial Markets, 14(5). |

| [3] | Akter, U., Anwar, S. R., Mustafa, R., Ali, Z., & Cumilla, B. (2021). Revisiting the impact of mobile banking on financial inclusion among the developing countries. International Journal of Financial Research, 12(2), 62-74. |

| [4] | Aron, J. (2017). Leapfrogging': A survey of the nature and economic implications of mobile money. Centre for the Study of African Economies, University of Oxford (No. 2017-02). |

| [5] | Bawuah, I. (2024). Mobile Money and Financial Inclusion: The role of Institutional Quality. Global Social Welfare, 1-15. |

| [6] | Bayar, Y., Gavriletea, M. D., & Păun, D. (2021). Impact of mobile phones and internet use on financial inclusion: Empirical evidence from the EU post-communist countries. Technological and Economic Development of Economy, 27(3), 722-741. |

| [7] | Berdibayev, Y., & Kwon, Y. (2020). Improving digital financial services inclusion: A panel data analysis. |

| [8] | Biswanath Behera, Haldar, A., & Sethi, N. (2023). Investigating the direct and indirect effects of Information and Communication Technology on economic growth in the emerging economies: role of financial development, foreign direct investment, innovation, and institutional quality. 12, 7(e), 1–24. |

| [9] | Cámara, N., & Tuesta, D. (2014). Measuring financial inclusion: A muldimensional index. BBVA Research Paper, (14/26). |

| [10] | Chawla, D., & Joshi, H. (2019). Consumer attitude and intention to adopt mobile wallet in India – An empirical study. International Journal of Bank Marketing, 37(7), 1590–1618. |

| [11] | Dabla-Norris, E., Ji, Y., Townsend, R. M., & Unsal, D. F. (2017). Distinguishing constraints on financial inclusion and their impact on gdp and inequality. |

| [12] | Daoud, J. I. (2017, December). Multicollinearity and regression analysis. In Journal of Physics: Conference Series (Vol. 949, No. 1, p. 012009). IOP Publishing. |

| [13] | Dass, R., & Pal, S. (2011). EXPLORING THE FACTORS AFFECTING THE ADOPTION OF MOBILE FINANCIAL SERVICES AMONG THE RURAL UNDER-BANKED. European Conference on Information Systems, 246. |

| [14] | di Castri, S. (2013). Enabling Mobile Money Policies in Sri Lanka: The Rise of EZ Cash. SSRN Electronic Journal. |

| [15] | Dienillah, A. A., Anggraeni, L., & Sahara, S. (2018). Impact of financial inclusion on financial stability based on income group countries. Bulletin of Monetary Economics and Banking, 20(4), 429-442. |

| [16] | Donner, J., & Tellez, C. A. (2008). Mobile banking and economic development: linking adoption, impact, and use. Asian Journal of Communication, 18(4), 318–332. |

| [17] | Donovan, K. (2012). Mobile money for financial inclusion. Information and Communications for development, 61(1), 61-73. |

| [18] | Evans, O. (2016). Determinants of financial inclusion in Africa: A dynamic panel data approach. |

| [19] | Ghosh, S. (2016). How important is mobile telephony for economic growth? Evidence from MENA countries. info, 18(3), 58-79. |

| [20] | Gupta, S., & Dhingra, S. (2022). Past, present and future of mobile financial services: A critique, review and future agenda. International Journal of Consumer Studies, 46(6), 2104-2127. |

| [21] | Hasan, M. A. (2019). Factors Affecting on Users’ Intentions toward 4G Mobile Services in Bangladesh. Asian Business Review, 9(1), 11–16. |

| [22] | Hazra, U., & Priyo, A. K. K. (2021). Mobile financial services in Bangladesh: Understanding the affordances. The Electronic Journal of Information Systems in Developing Countries, 87(3), e12166. |

| [23] | Sharif, S. (2017). Telecommunication and Its Impact over the Economic Development of SAARC Countries. |

| [24] | Hsiao, C. (2022). Analysis of panel data (No. 64). Cambridge university press. |

| [25] | Jacolin, L., Massil Joseph, K., & Noah, A. (2019). Informal Sector and Mobile Financial Services in Developing Countries: Does Financial Innovation Matter? SSRN Electronic Journal, 20(7). |

| [26] | Kabir, Md. H., Huda, S. S. M. S., & Faruq, O. (2021). MOBILE FINANCIAL SERVICES IN THE CONTEXT OF BANGLADESH. Copernican Journal of Finance & Accounting, 9(3), 83. |

| [27] | Kemal, A. A. (2018). Mobile banking in the government-to-person payment sector for financial inclusion in Pakistan. Information Technology for Development, 9(2), 1–28. |

| [28] | Khan, A. G., Lima, R. P., & Mahmud, Md. S. (2020). Investigating the relationship between service quality and customer satisfaction of BKash in Bangladesh. International Journal of Financial Services Management, 1(1), 1. |

| [29] | Khowsehawat, P., & Jantarakolica, T. (2020). Does Mobile Cellular Subscription Enhance Access of Financial Inclusion? (Doctoral dissertation, Thammasat University). |

| [30] | Kim, M., Zoo, H., Lee, H., & Kang, J. (2018). Mobile financial services, financial inclusion, and development: A systematic review of academic literature. The Electronic Journal of Information Systems in Developing Countries, 84(5), e12044. |

| [31] | Kumar, D. (2022). Prospects and challenges of mobile financial services (MFS) in Bangladesh. Handbook of research on social impacts of E-payment and blockchain technology, 320-341. |

| [32] | Lenka, S. K., & Barik, R. (2018). Has expansion of mobile phone and internet use spurred financial inclusion in the SAARC countries?. Financial Innovation, 4(1), 1-19. |

| [33] | Liébana-Cabanillas, F., Sánchez-Fernández, J., & Muñoz-Leiva, F. (2014). The moderating effect of experience in the adoption of mobile payment tools in Virtual Social Networks: The m-Payment Acceptance Model in Virtual Social Networks (MPAM-VSN). International Journal of Information Management, 34(2), 151–166. |

| [34] | Mas, I., & Morawczynski, O. (2009). Designing Mobile Money Services Lessons from M-PESA. Innovations: Technology, Governance, Globalization, 4(2), 77–91. |

| [35] | Mialou, A., Amidzic, G., & Massara, A. (2017). Assessing countries’ financial inclusion standing—A new composite index. Journal of Banking and Financial Economics, 2(8), 105-126. |

| [36] | Morduch, J., & Haley, B. (2002). Analysis of the effects of microfinance on poverty reduction (Vol. 1014, p. 7). New York: NYU Wagner working paper. |

| [37] | Musau, S., Muathe, S., & Mwangi, L. (2018). Financial inclusion, GDP and credit risk of commercial banks in Kenya. International Journal of Economics and Finance, 10(3), 181. |

| [38] | Okello Candiya Bongomin, G., Ntayi, J. M., Munene, J. C., & Malinga, C. A. (2018). Mobile money and financial inclusion in sub-Saharan Africa: the moderating role of social networks. Journal of African Business, 19(3), 361-384. |

| [39] | Oruo, J. (2013). The relationship between Financial Inclusion and GDP growth in Kenya (Doctoral dissertation, University of Nairobi). |

| [40] |

Osafo-Kwaako, P., Singer, M., White, O., & Zouaoui, Y. (2018). Mobile money in emerging markets: The business case for financial inclusion. McKinsey Global Institute, March.

https://www.rfilc.org/wp-content/uploads/2020/08/Mobile-money-in-emerging-markets.pdf |

| [41] | Pradhan, R. S., & Dahal, P. (2022). Effect of E-Banking on Financial Inclusion in Nepal. International Journal of Finance, Entrepreneurship & Sustainability, 15(4). |

| [42] | Rahman, A., Arabi, S., & Rab, R. (2021). Feasibility and Challenges of 5G Network Deployment in Least Developed Countries (LDC). Wireless Sensor Network, 13(01), 1–16. |

| [43] | Rajesh, S., Didwania, M., & Kumar, P. (2011). Need for financial inclusion for poverty alleviation and GDP growth. International Journal of Multidisciplinary Research, 1(6). |

| [44] | Rasheed, B., Law, S. H., Chin, L., & Habibullah, M. S. (2016). The role of financial inclusion in financial development: International evidence. Abasyn University Journal of Social Sciences, 9(2), 330-348. |

| [45] | Sarma, M. (2016). Measuring financial inclusion for Asian economies. Financial inclusion in Asia: Issues and policy concerns, 3-34. |

| [46] | Song, P., Lee, J., Abdelmoniem, A. M., & Mukhanov, L. (2025). Unlocking the power of 4G/5G mobile networks: An empirical dive into quality and energy efficiency in YouTube Edge services. Computer Networks, 111344. |

| [47] | Saxena, R., & Mokashi Punekar, R. (2020). Designing pro-poor mobile financial services: Learning from the financial diaries of urban poor in India. World Development Perspectives, 20(5), 100266. |

| [48] | Shaikh, A. A., Alamoudi, H., Alharthi, M., & Glavee-Geo, R. (2022). Advances in mobile financial services: a review of the literature and future research directions. International Journal of Bank Marketing, 41(1), 1-33. |

| [49] | Sharma, M. K. (2016). Financial inclusion: A prelude to economic status of vulnerable group. International Journal of research-Granthaalayah, 4(12), 147-154. |

| [50] | Song, H., & Chun, S. (2017). (Financial Inclusion) (A Case Study of Financial Services Companiess Differentiation Strategies with Financial Inclusion). SSRN Electronic Journal, 5(9). |

| [51] | Sultana, R. (2014). Mobile Financial Services (MFS) Business and Regulations: Evolution in South Asian Markets. SSRN Electronic Journal, 2(6). |

| [52] | Tram, T. X. H., Lai, T. D., & Nguyen, T. T. H. (2023). Constructing a composite financial inclusion index for developing economies. The Quarterly Review of economics and finance, 87, 257-265. |

| [53] | World Bank, 2022. Global Financial Development Report 2022: Financial Inclusion. Washington, DC: World Bank. |

APA Style

Shetty, S., Rahim, M. J., Islam, M. J., Nath, S. D., Ahmed, M. U. (2025). Comparative Analysis of Mobile Finance Markets in SAARC Nations: Drivers of Financial Inclusion. International Journal of Sustainability Management and Information Technologies, 11(2), 76-90. https://doi.org/10.11648/j.ijsmit.20251102.12

ACS Style

Shetty, S.; Rahim, M. J.; Islam, M. J.; Nath, S. D.; Ahmed, M. U. Comparative Analysis of Mobile Finance Markets in SAARC Nations: Drivers of Financial Inclusion. Int. J. Sustain. Manag. Inf. Technol. 2025, 11(2), 76-90. doi: 10.11648/j.ijsmit.20251102.12

@article{10.11648/j.ijsmit.20251102.12,

author = {Shekar Shetty and Md. Jawadur Rahim and Md. Jahidul Islam and Subroto Deb Nath and Mushfiq Uddin Ahmed},

title = {Comparative Analysis of Mobile Finance Markets in SAARC Nations: Drivers of Financial Inclusion

},

journal = {International Journal of Sustainability Management and Information Technologies},

volume = {11},

number = {2},

pages = {76-90},

doi = {10.11648/j.ijsmit.20251102.12},

url = {https://doi.org/10.11648/j.ijsmit.20251102.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijsmit.20251102.12},

abstract = {The study was conducted at the time of increasing demand to provide insight into the role of financial technologies in inclusive economic growth among the South Asian economies. Even though there is a rapid growth in mobile financial services in the region, there is a dearth of comparative evidence on the role of such innovations in promoting the financial inclusion phenomenon in various countries situated in the SAARC region. Filling this gap, the study offers a timely insight into policies to be improved by policymakers, regulators, and financial institutions to improve digital finance strategies and enhance equitable access to financial systems. The paper analyses the mobile finance markets as a proportion of the total economy among SAARC countries, focusing on factors affecting financial inclusion. The data has been collected from WDI from 2012 to 2022, demonstrating one of the latest studies focused on SAARC nations regarding MFS and Financial inclusions. After cleaning the data, the indicators from Bangladesh, India, and Pakistan were retained to maintain the accuracy of the results derived from this study. Five indicators, such as financial inclusion, mobile money transactions, GDP growth rate, individuals using the internet, and the number of mobile cellular subscriptions, were adopted from earlier research to compare the MFS market. This study shows that MFS markets have grown significantly over the past decade. However, the growth of a few MFS indicators has been steady since 2020 due to COVID-19 and other global issues. The results of panel regression revealed that mobile money transactions and mobile cellular subscriptions have a significance in improving financial inclusion in SAARC nations. Therefore, this research offers significant perspectives for authorities and mobile financial service providers to use effective mobile money methods in order to attain higher levels of financial inclusion in SAARC countries.

},

year = {2025}

}

TY - JOUR T1 - Comparative Analysis of Mobile Finance Markets in SAARC Nations: Drivers of Financial Inclusion AU - Shekar Shetty AU - Md. Jawadur Rahim AU - Md. Jahidul Islam AU - Subroto Deb Nath AU - Mushfiq Uddin Ahmed Y1 - 2025/10/27 PY - 2025 N1 - https://doi.org/10.11648/j.ijsmit.20251102.12 DO - 10.11648/j.ijsmit.20251102.12 T2 - International Journal of Sustainability Management and Information Technologies JF - International Journal of Sustainability Management and Information Technologies JO - International Journal of Sustainability Management and Information Technologies SP - 76 EP - 90 PB - Science Publishing Group SN - 2575-5110 UR - https://doi.org/10.11648/j.ijsmit.20251102.12 AB - The study was conducted at the time of increasing demand to provide insight into the role of financial technologies in inclusive economic growth among the South Asian economies. Even though there is a rapid growth in mobile financial services in the region, there is a dearth of comparative evidence on the role of such innovations in promoting the financial inclusion phenomenon in various countries situated in the SAARC region. Filling this gap, the study offers a timely insight into policies to be improved by policymakers, regulators, and financial institutions to improve digital finance strategies and enhance equitable access to financial systems. The paper analyses the mobile finance markets as a proportion of the total economy among SAARC countries, focusing on factors affecting financial inclusion. The data has been collected from WDI from 2012 to 2022, demonstrating one of the latest studies focused on SAARC nations regarding MFS and Financial inclusions. After cleaning the data, the indicators from Bangladesh, India, and Pakistan were retained to maintain the accuracy of the results derived from this study. Five indicators, such as financial inclusion, mobile money transactions, GDP growth rate, individuals using the internet, and the number of mobile cellular subscriptions, were adopted from earlier research to compare the MFS market. This study shows that MFS markets have grown significantly over the past decade. However, the growth of a few MFS indicators has been steady since 2020 due to COVID-19 and other global issues. The results of panel regression revealed that mobile money transactions and mobile cellular subscriptions have a significance in improving financial inclusion in SAARC nations. Therefore, this research offers significant perspectives for authorities and mobile financial service providers to use effective mobile money methods in order to attain higher levels of financial inclusion in SAARC countries. VL - 11 IS - 2 ER -

Jesse H. Jones School of Business, Texas Southern University, Texas, United States

Department of Information Technology, Home Health Care Services of New York, New York, United States

Collins College of Business, University of Tulsa, Oklahoma, United States

Collins College of Business, University of Tulsa, Oklahoma, United States

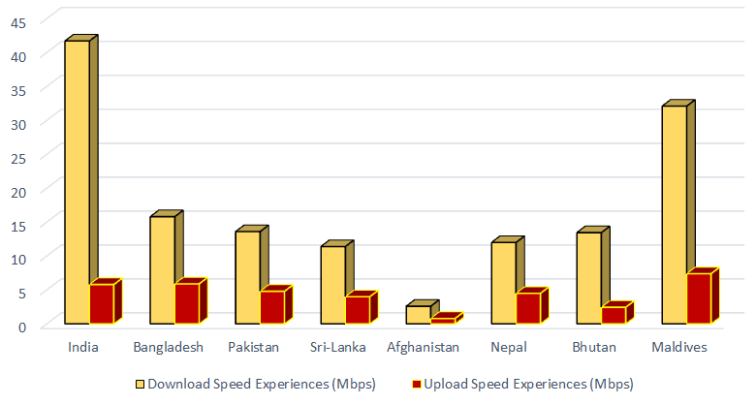

Figure 1. Mobile Network Experience Across SAARC Countries.

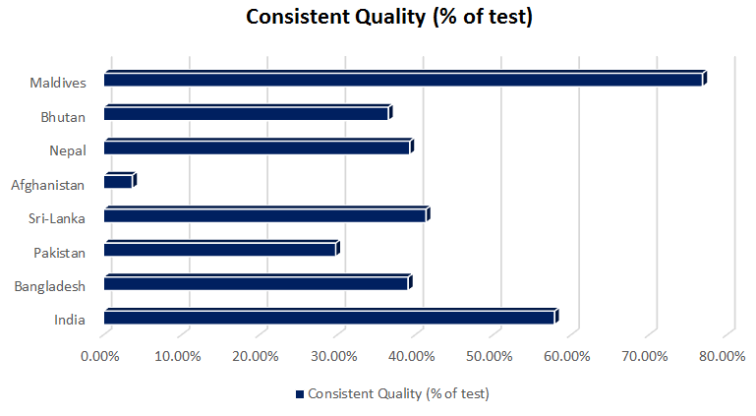

Figure 2. Consistency rate of Mobile Internet Across SAARC.

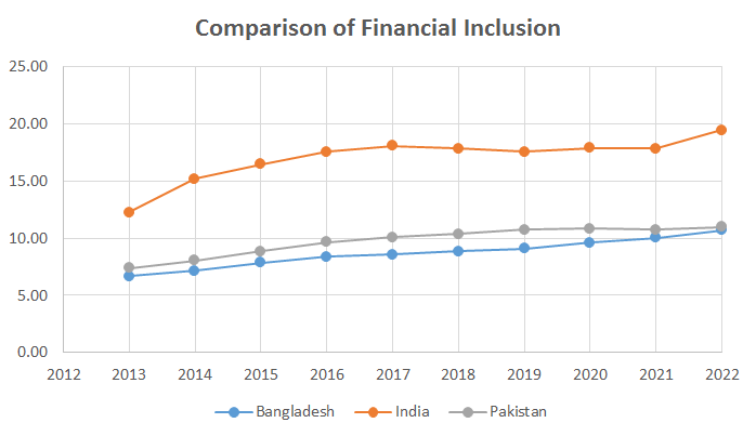

Figure 3. Line Chart of Financial Inclusion.

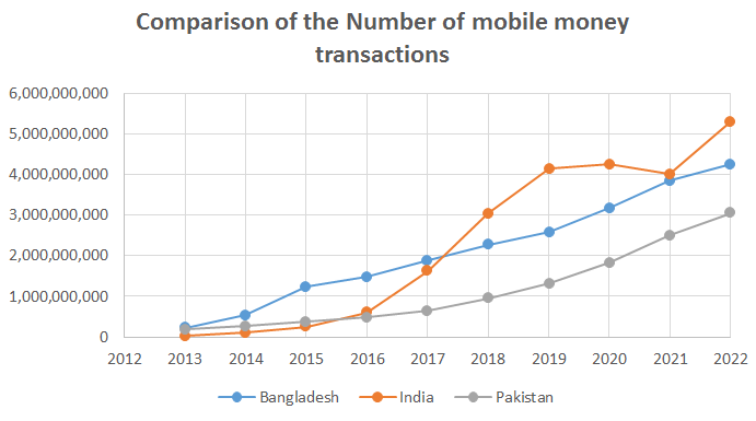

Figure 4. Line Chart of the number of mobile money transactions.

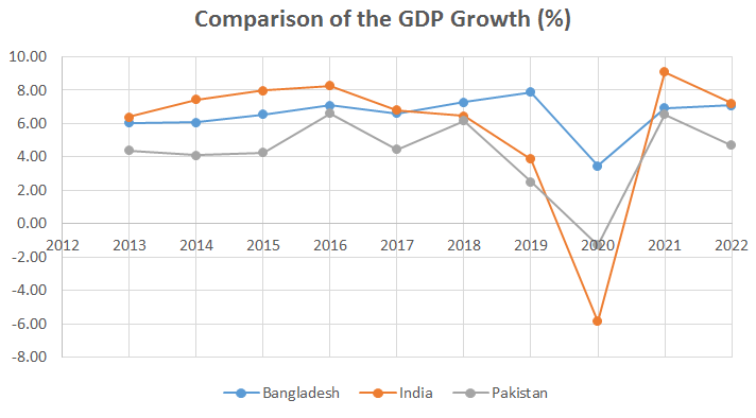

Figure 5. Line Chart of the GDP Growth (%).

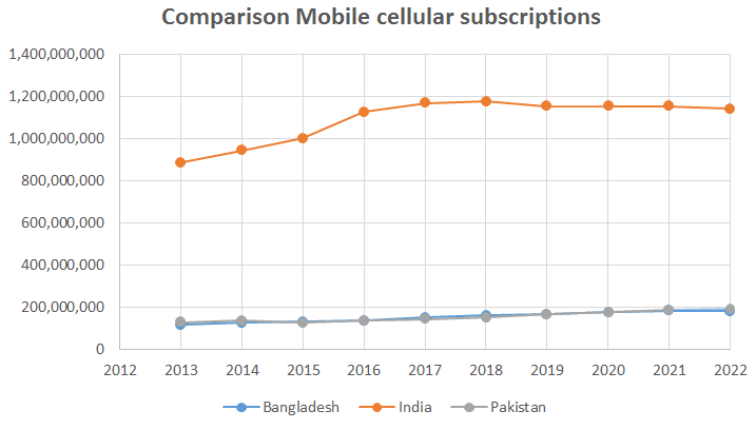

Figure 6. Line Chart of Mobile Cellular Subscriptions.

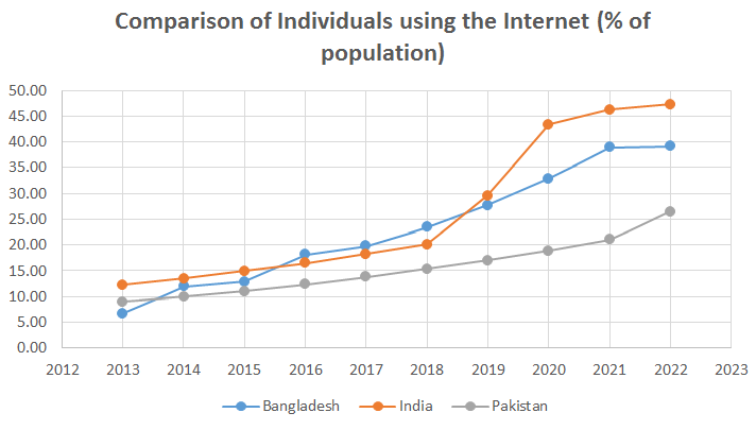

Figure 7. Line Chart of Individuals using the Internet (% of population).

Information