Abstract

Climate change poses significant challenges in regions with inadequate institutional support for climate-sensitive activities. This study examines two key strategies that households adopt to manage climate risks: self-protection measures and climate insurance. Self-protection measures involve proactive actions such as constructing stronger buildings, diversifying business activities, and implementing other protective mechanisms against climate extremes. These measures are often sustainable and empowering, yet they tend to be costly and challenging to implement. On the other hand, climate risk insurance serves as a financial safety net, providing economic recovery after climate-related events have occurred. However, despite being relatively affordable, climate insurance faces low demand due to various barriers, including accessibility issues and a lack of awareness. This study aims to explore the potential for combining these two approaches to enhance household resilience and promote equitable development. Overcoming barriers to adoption requires strategies such as offering grants and reimbursements to adopters, improving access to insurance products, and raising awareness about their benefits. Future research should investigate how these strategies can complement each other and explore ways to strengthen household resilience based on socio-economic differences across various regions.

Keywords

Self-Protection Measures, Climate Insurance, Climate Risk Management, Household Resilience, Developing Economies

1. Introduction

Climate change is a major concern for developing economies due to their increased vulnerability, which results from weak adaptive capacity, poor institutional support, and high sensitivity to climate-related impacts. This vulnerability is largely driven by heavy reliance on climate-sensitive productive activities, particularly agriculture. People in these regions face a greater risk of humanitarian disasters, including severe weather events, famine, and floods. These challenges put significant pressure on their livelihoods, further deepening socio-economic inequalities and hindering sustainable development

. To manage these risks, households typically adopt two main strategies: self-protection measures and climate insurance. Self-protection measures involve actions such as strengthening homes, businesses, or farms to withstand climate impacts, diversifying income sources to reduce reliance on climate-sensitive activities and implementing sustainable farming techniques. These measures empower households by giving them greater control over their resources and energy use. However, they often require significant financial investment and technical expertise, which can be challenging for many households to access

| [20] | Alinovi, L., Mane, E., & Romano, D. (2010). Measuring household resilience to food insecurity: Application to Palestinian households. Agricultural survey methods, 341-368. https://doi.org/10.1002/9780470665480.ch21 |

[20]

. On the other hand, climate insurance provides financial support after adverse events occur, serving as a safeguard against climate-related risks. However, it faces several challenges, including high premiums that make it unaffordable for many households, limited accessibility, and trust issues. Many people are hesitant to adopt climate insurance due to concerns about the reliability of payouts, lack of understanding of the product, and uncertainty about whether the benefits outweigh the costs

| [12] | Hansen, J., Hellin, J., Rosenstock, T., Fisher, E., Cairns, J., Stirling, C.,... & Campbell, B. (2019). Climate risk management and rural poverty reduction. Agricultural Systems, 172, 28-46. https://doi.org/10.1016/j.agsy.2018.01.019 |

| [14] | Polo, L. (2024). Revolutionizing sales and operations planning with artificial intelligence: Insights and results. International Journal For Multidisciplinary Research, 6(6). https://doi.org/10.36948/ijfmr.2024.v06i06.34053 |

[12, 14]

.

When deciding between self-protection measures and climate insurance, households consider several factors, including cost, availability, perceived effectiveness of each strategy, and their own level of risk tolerance. This article evaluates the costs and effectiveness of both self-protection and climate insurance, examining their scalability and long-term sustainability. To achieve its objectives, the study applies theoretical frameworks and empirical evidence to provide insights that can help policymakers develop coherent strategies. These strategies aim to enhance household resilience, stabilize the economy, and promote more equitable development in response to the growing threats posed by climate change.

| [19] | Knippenberg, E., Jensen, N., & Constas, M. (2019). Quantifying household resilience with high frequency data: Temporal dynamics and methodological options. World Development, 121, 1-15. https://doi.org/10.1016/j.worlddev.2019.04.010 |

[19]

.

1.1. Background Context

Climate change significantly impacts economic development, particularly in the global south, through extreme weather conditions, prolonged droughts, and erratic rainfall patterns. These changes have severe consequences for agriculture-dependent households and other sectors reliant on natural resources. As a result, vulnerabilities increase, especially in regions with weak institutional support and inadequate infrastructure, further hindering their ability to adapt and thrive in the face of climate challenges

| [15] | Nkonya, E., Place, F., Kato, E., & Mwanjololo, M. (2015). Climate risk management through sustainable land management in Sub-Saharan Africa. Sustainable intensification to advance food security and enhance climate resilience in Africa, 75-111. https://doi.org/10.1007/978-3-319-09360-4_5 |

[15]

.

Households adopt two primary strategies to mitigate climate risks: self-protection measures and climate insurance. Self-protection measures, also known as safety and safeguards, include various risk management approaches such as diversifying income sources, adopting improved farming practices, and investing in infrastructure to enhance resilience against climate-related challenges. On the other hand, climate insurance serves as a financial safeguard by transferring the risk to insurers. It provides households with financial relief after adverse events, helping them avoid falling into poverty and ensuring a quicker recovery from climate-related shocks

.

However, climate insurance has not seen significant progress in developing countries, and there is still no clear understanding of why many households prefer to remain self-insured. Several factors influence their decisions, including cultural beliefs, levels of knowledge and awareness, and perceptions of the risks involved in investing in insurance products. Understanding these factors is essential for developing effective climate risk management strategies that align with the needs and preferences of households

.

1.2. Importance of the Study

Understanding how households in developing economies navigate between self-protection measures and climate insurance is crucial for several reasons:

1.2.1. Enhancing Resilience

Public authorities recognize both the challenges associated with climate insurance and the limitations of self-insurance practices. This understanding is essential for designing effective interventions that enhance households' ability to cope with climate risks. By addressing these constraints, policymakers can develop targeted strategies that improve access to climate insurance, promote better risk management practices, and strengthen household resilience in the face of climate-related challenges

.

1.2.2. Promoting Equitable Development

Most self-protection activities require significant upfront costs and tend to generate substantial returns, primarily benefiting wealthier households. However, when these measures are effectively structured and made accessible to vulnerable households, they can help mitigate economic inequalities by enhancing resilience and providing long-term financial stability

.

1.2.3. Optimizing Policy Design

Lenders and insurers often face challenges in deciding how to allocate limited resources between promoting insurance products and implementing measures that encourage consumers to adapt their properties to meet coverage requirements. Gaining a deeper understanding of households' specific needs and limitations can help optimize resource allocation and set clear priorities. This approach ensures that efforts are targeted effectively, improving both insurance uptake and household resilience to climate risks.

| [6] | Surminski, S., Bouwer, L. M., & Linnerooth-Bayer, J. (2016). How insurance can support climate resilience. Nature Climate Change, 6(4), 333-334. https://doi.org/10.1038/nclimate2979 |

[6]

1.2.4. Informing Climate Finance

A substantial amount of international climate finance is directed toward developing economies to help them address climate-related challenges. The findings of this study will be highly valuable for donor agencies and governments in formulating effective strategies for utilizing these financial resources. By ensuring that funds are allocated efficiently, these strategies can better protect vulnerable populations and enhance their resilience to climate risks.

| [12] | Hansen, J., Hellin, J., Rosenstock, T., Fisher, E., Cairns, J., Stirling, C.,... & Campbell, B. (2019). Climate risk management and rural poverty reduction. Agricultural Systems, 172, 28-46. https://doi.org/10.1016/j.agsy.2018.01.019 |

[12]

1.3. Research Objectives

The study aims to achieve the following objectives:

1.3.1. Analyze Decision-Making Dynamics

Investigate and describe the rationality and choice of households in developing countries in relation to climate risk management and choices between self-adjustment measures and formal climate insurance.

1.3.2. Evaluate Effectiveness

Compare the effectiveness of self-protection measures and climate insurance in reducing household exposure and enhancing adaptive opportunities.

1.3.3. Policy Recommendations

Develop clear policy recommendations on how to design these interventions and encourage households to adopt the most effective strategies..

1.3.4. Theoretical Insights

Advance knowledge in the economic and behavioral fields of risk management and climate adaptation, from the perspective of the developing countries.

2. Literature Review

2.1. Definition of Key Terms

2.1.1. Self-Protection Measures

Household coping strategies refer to the actions that households take to reduce their exposure to climate risks. These strategies may include diversifying income sources, adopting sustainable agricultural practices, and constructing resilient infrastructure, such as flood-resistant homes and weather-resistant crops. These measures are primarily preventive and require behavioral adjustments to effectively manage climate impacts at the household level.

2.1.2. Climate Insurance

Climate insurance involves the use of financial instruments to manage climate-related risks by transferring them to an insurance company or other financial organizations. Examples of climate insurance include agricultural insurance, catastrophe insurance, and parametric insurance, which provide financial payouts to clients in the event of climate-related disasters affecting their homes or livelihoods. This type of insurance offers protection to households by sharing and distributing risk, ensuring financial stability in the face of climate uncertainties.

| [4] | Silva, M. V. F., Loures, C. D. M. G., Alves, L. C. V., De Souza, L. C., Borges, K. B. G., & Carvalho, M. D. G. (2019). Alzheimer’s disease: risk factors and potentially protective measures. Journal of biomedical science, 26, 1-11. https://doi.org/10.1186/s12929-019-0524-y |

[4]

.

2.2. A Review of Literature on Protective Actions

Various assessments in past literature highlight self-protection measures as a crucial component of climate risk management. Significant attention has been given to strategies such as diversifying agricultural activities, investing in climate-resilient infrastructure, and adopting environmentally friendly farming techniques. Studies have shown that while these protective measures can reduce the likelihood of climate-related risks in the near future, they often require high initial investments and may not provide comprehensive protection against all potential threats

| [2] | Ağalar, C., & Engin, D. Ö. (2020). Protective measures for COVID-19 for healthcare providers and laboratory personnel. Turkish journal of medical sciences, 50(9), 578-584. https://doi.org/10.3906/sag-2004-132 |

| [6] | Surminski, S., Bouwer, L. M., & Linnerooth-Bayer, J. (2016). How insurance can support climate resilience. Nature Climate Change, 6(4), 333-334. https://doi.org/10.1038/nclimate2979 |

| [20] | Alinovi, L., Mane, E., & Romano, D. (2010). Measuring household resilience to food insecurity: Application to Palestinian households. Agricultural survey methods, 341-368. https://doi.org/10.1002/9780470665480.ch21 |

[2, 6, 20]

. Moreover, the effectiveness of self-protection strategies is largely influenced by factors such as financial resources, technological capabilities, and the quality of local governance. Without adequate financial and technical support, households may struggle to implement these measures effectively, limiting their overall resilience to climate risks.

| [1] | Cirrincione, L., Plescia, F., Ledda, C., Rapisarda, V., Martorana, D., Moldovan, R. E., & Cannizzaro, E. (2020). COVID-19 pandemic: Prevention and protection measures to be adopted at the workplace. Sustainability, 12(9), 3603. https://doi.org/10.3390/su12093603 |

[1]

2.3. Previous Research on Climate Insurance

Research on climate insurance has examined its potential as an effective approach for managing various financial risks in developing countries. Studies suggest that climate insurance can provide timely and sufficient financial support, helping households mitigate the impacts of climate-related losses and safeguard their overall well-being. By offering prompt cash payouts or investment opportunities, climate insurance enhances the resilience of vulnerable populations against climate shocks

| [10] | Duus-Otterström, G., & Jagers, S. C. (2011). Why (most) climate insurance schemes are a bad idea. Environmental Politics, 20(3), 322-339. https://doi.org/10.1080/09644016.2011.573354 |

| [15] | Nkonya, E., Place, F., Kato, E., & Mwanjololo, M. (2015). Climate risk management through sustainable land management in Sub-Saharan Africa. Sustainable intensification to advance food security and enhance climate resilience in Africa, 75-111. https://doi.org/10.1007/978-3-319-09360-4_5 |

| [18] | Sarkar, A.., Islam, S. A. M., & Bari, M. S.. (2024). Transforming User Stories into Java Scripts: Advancing Qa Automation in The Us Market With Natural Language Processing. Journal of Artificial Intelligence General Science (JAIGS) ISSN: 3006-4023, 7(01), 9–37. https://doi.org/10.60087/jaigs.v7i01.293 |

[10, 15, 18]

. However, numerous cross-sectional studies have identified persistent barriers to the widespread adoption of climate insurance. These challenges include low insurance penetration, high premiums relative to household income, and limited public awareness and understanding of insurance products

| [20] | Alinovi, L., Mane, E., & Romano, D. (2010). Measuring household resilience to food insecurity: Application to Palestinian households. Agricultural survey methods, 341-368. https://doi.org/10.1002/9780470665480.ch21 |

| [22] | Collier, P., Van Der Ploeg, R., Spence, M., & Venables, A. J. (2010). Managing resource revenues in developing economies. IMF Staff papers, 57(1), 84 https://doi.org/10.1057/imfsp.2009.16 |

| [24] | Fry, M. J. (1982). Models of financially repressed developing economies. World development, 10(9), 731-750. https://doi.org/10.1016/0305-750X(82)90026-2 |

[20, 22, 24]

. Additionally, the design of climate insurance schemes often needs to be tailored to align with local practices and socio-economic conditions to effectively protect vulnerable communities and ensure broader accessibility and acceptance.

2.4. Comparative Studies

Previous research has primarily used cost comparisons between self-protection measures and climate insurance as the key framework for evaluating their effectiveness

| [15] | Nkonya, E., Place, F., Kato, E., & Mwanjololo, M. (2015). Climate risk management through sustainable land management in Sub-Saharan Africa. Sustainable intensification to advance food security and enhance climate resilience in Africa, 75-111. https://doi.org/10.1007/978-3-319-09360-4_5 |

| [17] | Jones, L., & Tanner, T. (2015). Measuring'subjective resilience': using peoples' perceptions to quantify household resilience. https://dx.doi.org/10.2139/ssrn.2643420 |

| [19] | Knippenberg, E., Jensen, N., & Constas, M. (2019). Quantifying household resilience with high frequency data: Temporal dynamics and methodological options. World Development, 121, 1-15. https://doi.org/10.1016/j.worlddev.2019.04.010 |

[15, 17, 19].

Analyzing empirical studies, it can be concluded that while self-protection measures are more effective in the long run, climate insurance offers immediate and tangible financial relief to families affected by climate-related disasters

| [7] | Mills, E. (2005). Insurance in a climate of change. Science, 309(5737), 1040-1044. https://doi.org/10.1126/science.1112121 |

| [9] | Müller, B., Johnson, L., & Kreuer, D. (2017). Maladaptive outcomes of climate insurance in agriculture. Global Environmental Change, 46, 23-33. https://doi.org/10.1016/j.gloenvcha.2017.06.010 |

| [11] | Fünfgeld, H. (2010). Institutional challenges to climate risk management in cities. Current Opinion in Environmental Sustainability, 2(3), 156-160. https://doi.org/10.1016/j.cosust.2010.07.001 |

[7, 9, 11]

. Furthermore, research suggests that combining both strategies in the risk management process can enhance households' overall capacity to manage climate risks effectively. Studies also indicate that the decision to adopt self-protection measures or invest in climate insurance is largely influenced by factors such as access to financial resources, the distribution of capital, and the level of vulnerability experienced by households

| [5] | Van der Weerd, W., Timmermans, D. R., Beaujean, D. J., Oudhoff, J., & Van Steenbergen, J. E. (2011). Monitoring the level of government trust, risk perception and intention of the general public to adopt protective measures during the influenza A (H1N1) pandemic in the Netherlands. BMC public health, 11, 1-12. |

| [16] | Islam, S. M., Bari, M. S., Sarkar, A., Khan, A. O. R., & Paul, R. (2024). AI-Powered Threat Intelligence: Revolutionizing Cybersecurity with Proactive Risk Management for Critical Sectors. Journal of Artificial Intelligence General science (JAIGS) ISSN: 3006-4023, 7(01), 1-8. https://doi.org/10.60087/jaigs.v7i01.291 |

| [18] | Sarkar, A.., Islam, S. A. M., & Bari, M. S.. (2024). Transforming User Stories into Java Scripts: Advancing Qa Automation in The Us Market With Natural Language Processing. Journal of Artificial Intelligence General Science (JAIGS) ISSN: 3006-4023, 7(01), 9–37. https://doi.org/10.60087/jaigs.v7i01.293 |

[5, 16, 18].

2.5. Gaps in Existing Literature

Despite the growing body of research on climate risk management, significant knowledge gaps remain regarding the cost of protection and the comparative effectiveness of self-protection measures versus climate insurance. For example, there is limited evidence on how these strategies interact—whether they function as substitutes or complements—across different climatic conditions. Additionally, most studies focus on rural areas and specific regions, overlooking the broader economic, social, and political contexts that influence decision-making

| [9] | Müller, B., Johnson, L., & Kreuer, D. (2017). Maladaptive outcomes of climate insurance in agriculture. Global Environmental Change, 46, 23-33. https://doi.org/10.1016/j.gloenvcha.2017.06.010 |

| [10] | Duus-Otterström, G., & Jagers, S. C. (2011). Why (most) climate insurance schemes are a bad idea. Environmental Politics, 20(3), 322-339. https://doi.org/10.1080/09644016.2011.573354 |

| [14] | Polo, L. (2024). Revolutionizing sales and operations planning with artificial intelligence: Insights and results. International Journal For Multidisciplinary Research, 6(6). https://doi.org/10.36948/ijfmr.2024.v06i06.34053 |

[9, 10, 14]

. Moreover, there are few comprehensive evaluations that assess the long-term sustainability and effectiveness of these strategies at the community level. Further research is needed to better understand the complexities of household decision-making and the role of government in promoting and facilitating the adoption of these climate risk management strategies.

3. Theoretical Framework

The theoretical foundation for this analysis is drawn from key concepts in risk management economics, consumer decision theories, behavioral economics, and information asymmetry. These theories provide a comprehensive framework to better understand how populations in emerging economies adopt self-protection strategies and climate risk insurance. By applying these perspectives, the analysis can offer valuable insights into the factors influencing household decisions, the challenges they face, and the effectiveness of different risk management approaches.

3.1. Economic Theory of Risk Management

According to economic theory, risk management is the activity involving the identification, evaluation and prioritization of risks, with the subsequent allocation of resources to address those risks with the ultimate objectives of addressing the probability of occurrence and the ramifications of adverse incidents. Under climate change, developing countries remain more at risk as far as geographical exposure, adaptive capacity and financial resources are concerned.

Households often confront two primary strategies to manage climate risks:

3.1.1. Self-Protection Measures

These strategies include structural assets such as flood-resistant housing, water storage facilities, participation in income-generating activities beyond farming, and community resilience initiatives. In regions with limited institutional support, households often prefer self-reliance as a means of coping with climate risks

| [3] | Cipollina, M., & Salvatici, L. (2008). Measuring protection: mission impossible? Journal of Economic Surveys, 22(3), 577-616. https://doi.org/10.1111/j.1467-6419.2007.00543.x |

| [5] | Van der Weerd, W., Timmermans, D. R., Beaujean, D. J., Oudhoff, J., & Van Steenbergen, J. E. (2011). Monitoring the level of government trust, risk perception and intention of the general public to adopt protective measures during the influenza A (H1N1) pandemic in the Netherlands. BMC public health, 11, 1-12. |

| [7] | Mills, E. (2005). Insurance in a climate of change. Science, 309(5737), 1040-1044. https://doi.org/10.1126/science.1112121 |

[3, 5, 7]

. However, this approach typically demands significant financial resources and entails high opportunity costs, making it challenging for many households to implement effectively.

3.1.2. Climate Insurance

Climate-based insurance products work by transferring climate-related risks and financial burdens to insurance companies, with individuals paying premiums in exchange for coverage

| [14] | Polo, L. (2024). Revolutionizing sales and operations planning with artificial intelligence: Insights and results. International Journal For Multidisciplinary Research, 6(6). https://doi.org/10.36948/ijfmr.2024.v06i06.34053 |

| [15] | Nkonya, E., Place, F., Kato, E., & Mwanjololo, M. (2015). Climate risk management through sustainable land management in Sub-Saharan Africa. Sustainable intensification to advance food security and enhance climate resilience in Africa, 75-111. https://doi.org/10.1007/978-3-319-09360-4_5 |

| [18] | Sarkar, A.., Islam, S. A. M., & Bari, M. S.. (2024). Transforming User Stories into Java Scripts: Advancing Qa Automation in The Us Market With Natural Language Processing. Journal of Artificial Intelligence General Science (JAIGS) ISSN: 3006-4023, 7(01), 9–37. https://doi.org/10.60087/jaigs.v7i01.293 |

[14, 15, 18]

. These mechanisms help ensure financial support is available quickly after a disaster, enabling faster recovery and reducing economic hardship. However, the adoption of such products is often hindered by their recurring costs and a lack of trust in insurance providers. Many individuals are reluctant to invest in these products due to concerns about transparency, reliability, and the perceived fairness of payouts.

3.2. Consumer Decision-Making in Households

Household decision-making in the context of climate risks is a dynamic and multi-faceted process involving:

3.2.1. Resource Allocation

Lack of funding means households cannot afford long-term protection against the risks in the future. The decisions are also significantly dictated by the chances and consequences that are associated with climate events

| [2] | Ağalar, C., & Engin, D. Ö. (2020). Protective measures for COVID-19 for healthcare providers and laboratory personnel. Turkish journal of medical sciences, 50(9), 578-584. https://doi.org/10.3906/sag-2004-132 |

| [3] | Cipollina, M., & Salvatici, L. (2008). Measuring protection: mission impossible? Journal of Economic Surveys, 22(3), 577-616. https://doi.org/10.1111/j.1467-6419.2007.00543.x |

[2, 3]

.

3.2.2. Social Norms and Cultural Beliefs

In many developing countries, cultural values and tribal traditions play a significant role in shaping decision-making processes. For example, community-based self-help groups often favor collective, organizational forms of resilience, such as mutual aid and cooperative efforts, over formal insurance solutions. These traditional support systems align more closely with cultural norms and social structures, making them a preferred choice for managing risks

| [5] | Van der Weerd, W., Timmermans, D. R., Beaujean, D. J., Oudhoff, J., & Van Steenbergen, J. E. (2011). Monitoring the level of government trust, risk perception and intention of the general public to adopt protective measures during the influenza A (H1N1) pandemic in the Netherlands. BMC public health, 11, 1-12. |

| [8] | Collier, S. J., Elliott, R., & Lehtonen, T. K. (2021). Climate change and insurance. Economy and Society, 50(2), 158-172. https://doi.org/10.1080/03085147.2021.1903771 |

[5, 8]

.

3.2.3. Temporal Considerations

Non-cash benefits, including easily observable self-protection measures, are often preferred over insurance, even when the latter offers greater long-term benefits. This preference is particularly pronounced in low-income regions, where a prevalent short-term mindset drives decision-making, prioritizing immediate, tangible solutions over future financial security

.

3.2.4. Intergenerational Effects

Households that prioritize the stability and well-being of future generations, as well as long-term risk management and protection, may find self-insurance more appealing, as it offers sustained benefits over time. On the other hand, households that view insurance primarily as a safeguard during emergencies are more likely to opt for traditional insurance policies to address immediate financial risks.

.

3.3. Behavioral Economics: Understanding for Climate Change

The field of behavioral economics offers an understanding of the cognitive attitudes and mental shortcuts that govern household choices under climate risk. Key concepts include:

3.3.1. Loss Aversion

Households often tend to overestimate the costs associated with insurance premiums while undervaluing the benefits of risk transfer. This perception can hinder their willingness to adopt insurance as a viable risk management strategy

| [12] | Hansen, J., Hellin, J., Rosenstock, T., Fisher, E., Cairns, J., Stirling, C.,... & Campbell, B. (2019). Climate risk management and rural poverty reduction. Agricultural Systems, 172, 28-46. https://doi.org/10.1016/j.agsy.2018.01.019 |

[12]

.

3.3.2. Present Bias

Self-control issues which are manifested in the tendency to spend money now rather than to save for the future are also evident by low savings for precautionary purposes and for investment in protection against diseases

| [14] | Polo, L. (2024). Revolutionizing sales and operations planning with artificial intelligence: Insights and results. International Journal For Multidisciplinary Research, 6(6). https://doi.org/10.36948/ijfmr.2024.v06i06.34053 |

| [15] | Nkonya, E., Place, F., Kato, E., & Mwanjololo, M. (2015). Climate risk management through sustainable land management in Sub-Saharan Africa. Sustainable intensification to advance food security and enhance climate resilience in Africa, 75-111. https://doi.org/10.1007/978-3-319-09360-4_5 |

[14, 15]

.

3.3.3. Overconfidence and Optimism Bias

Risks are not well understood by many households, leaving them poorly prepared and often reliant on self-protection strategies to manage their impacts

| [16] | Islam, S. M., Bari, M. S., Sarkar, A., Khan, A. O. R., & Paul, R. (2024). AI-Powered Threat Intelligence: Revolutionizing Cybersecurity with Proactive Risk Management for Critical Sectors. Journal of Artificial Intelligence General science (JAIGS) ISSN: 3006-4023, 7(01), 1-8. https://doi.org/10.60087/jaigs.v7i01.291 |

[16]

.

3.3.4. Social Learning and Peer Effects

It has been observed that the decision to respond to such climatic conditions—whether by purchasing an insurance policy to mitigate risk or by adopting self-protection measures—can be significantly influenced by the actions of others within the community, including local leaders. Policies that take this social dynamic into account are more effective in encouraging the adoption of these measures

| [12] | Hansen, J., Hellin, J., Rosenstock, T., Fisher, E., Cairns, J., Stirling, C.,... & Campbell, B. (2019). Climate risk management and rural poverty reduction. Agricultural Systems, 172, 28-46. https://doi.org/10.1016/j.agsy.2018.01.019 |

| [13] | Hellmuth, M. E., Moorhead, A., & Williams, J. (2007). Climate risk management in Africa: Learning from practice. https://doi.org/10.7916/jrr9-sq53 |

| [16] | Islam, S. M., Bari, M. S., Sarkar, A., Khan, A. O. R., & Paul, R. (2024). AI-Powered Threat Intelligence: Revolutionizing Cybersecurity with Proactive Risk Management for Critical Sectors. Journal of Artificial Intelligence General science (JAIGS) ISSN: 3006-4023, 7(01), 1-8. https://doi.org/10.60087/jaigs.v7i01.291 |

[12, 13, 16]

.

3.4. Information Asymmetry

Lack of information is a critical barrier to effective risk management in developing economies, making information asymmetry a significant challenge. This asymmetry manifests in several ways, including:

3.4.1. Lack of Awareness

Many households are unaware of insurance products and self-protection options available to them. This lack of awareness is further compounded by low literacy levels and inadequate outreach efforts, which fail to effectively communicate the available risk management solutions to those in need. As a result, affected households remain uninformed and unprepared to take advantage of protective measures that could enhance their resilience

| [5] | Van der Weerd, W., Timmermans, D. R., Beaujean, D. J., Oudhoff, J., & Van Steenbergen, J. E. (2011). Monitoring the level of government trust, risk perception and intention of the general public to adopt protective measures during the influenza A (H1N1) pandemic in the Netherlands. BMC public health, 11, 1-12. |

[5]

.

3.4.2. Moral Hazard

Moral hazard presents a significant challenge for insurance companies, making it difficult to accurately assess policyholders' behavior. As a result, insurers may end up offering policies that are either underpriced or subject to excessive use, leading to financial strain. Similarly, once households obtain insurance coverage, they may neglect essential risk management practices, relying solely on their insurance policies instead of taking proactive measures to mitigate risks

.

3.4.3. Adverse Selection

High-risk households will tend to buy the insurance which makes the premium expensive and may make it impossible for low-risk individuals to afford the insurance product

| [15] | Nkonya, E., Place, F., Kato, E., & Mwanjololo, M. (2015). Climate risk management through sustainable land management in Sub-Saharan Africa. Sustainable intensification to advance food security and enhance climate resilience in Africa, 75-111. https://doi.org/10.1007/978-3-319-09360-4_5 |

[15]

.

3.4.4. Trust Deficits

Purchasers lack confidence in insurance providers, in most cases, as they have been let down in the past by some providers not honoring their dues or having obscure procedures. This problem requires clear communication and good regulation, and it is, therefore, crucial to provide information about results as well as good regulation of the institutions involved

.

3.4.5. Access to Risk Information

The composition of climate risks and their likelihood and consequences for households often remain unreported or hidden. Better perception of risks and enhanced means and ways of sharing information can improve decision making.

4. Methodology

The following is a description of the approach that may be used in analyzing economic costs of self-protective mechanisms against climate risk and those of climate insurance products in developing nations. A clear methodological framework provides a solid grounding to relate the way in which households make a decision between these two strategies. It deals with research design, data collection techniques, sampling techniques and analysis methods.

4.1. Research Design

The study uses both quantitative and qualitative research to ensure that a broader view of the household decision making process is captured. This approach is crucial for obtaining not only quantitative economic variables but also those that reflect the quality of decisions made at the individual level in the choice between self-insurance and climate insurance.

Key elements of the research design include:

1) Descriptive Analysis: To draw the distribution of self-protection measures and the climate insurance participation by households.

2) Comparative Analysis: To understand other factors and preferences distinguishing those households that rely on one strategy compared to the other.

3) Causal Inference: To assess factors which compelled households to make certain decisions and whether the approaches used in those recommendations can help reduce climate risks.

The study is designed to analyze cross-sectional data, with the potential to incorporate longitudinal data. This approach allows for tracking changes over a period of time, particularly to observe the effects of new policies or the impact of weather-related disasters.

4.2. Data Collection Methods

The specific data collection techniques used reflect objective as well as behavioral indicators regarding household choices. The following methods are emphasized:

4.2.1. Surveys

Structured surveys are the primary tool for collecting quantitative data on:

Household income and expenditure sources were analyzed separately to assess their relationship with the formation of assets and liabilities. This approach helps to better understand how different income streams and spending patterns contribute to financial stability and debt accumulation within households.

1) Nature and Cost of Self-Protective Measures: The type and expense of self-protection strategies that households implement to safeguard themselves against climate risks, such as building reinforcements, water conservation techniques, or crop diversification.

2) Awareness and Knowledge of Climate Insurance Products: The extent to which households are informed about available climate insurance options, including their benefits, costs, and how they can be utilized to mitigate financial losses from climate-related events.

3) Perceived Climate Risks and Coping Strategies: Households' understanding of climate risks and their chosen methods to cope with them, whether through savings, community support, or alternative adaptive measures to enhance resilience.

Surveys are typically conducted using a fixed set of standardized questions to ensure consistency across all respondents. This standardization allows for uniform data collection, making it easier to compare responses and analyze results accurately. Whenever possible, data is entered directly into a computer system to minimize errors and enhance efficiency in the data entry process.

4.2.2. Interviews

Semi-structured interviews with households and community leaders provide qualitative insights into: behavioral factors including risk perception and culture, as well as barriers to take measures for self-protection or climate insurance.

The following mechanism was established to provide requisite feedback relating to existing policies and programs: Specifically, interviews enable a discussion of contextual factors that include culture and practices in households.

4.2.3. Secondary Data Analysis

To backup primary data, secondary sources include government reports, insurance market data, and climate risks assessments.

It includes historical data of climate events and their effects on the economy, various descriptions of the level of insurance density in development states, and official policy papers and program assessment reports from governmental and other intergovernmental agencies.

Secondary data analysis served to bring the results of the study into perspective and also afforded an independent confirmation of primary data through triangulation processes.

4.3. Sample Selection

The identification of the sample is very important in a way to maintain the representativeness and reliability of the study. In order to analyze the diversity within the households, a stratified sampling method has been used.

4.3.1. Description of the Stratified Sampling Method

Stratified sampling is a probability sampling method that enhances the representativeness of a sample by dividing the population into distinct subgroups, known as strata, which share similar characteristics. This method is particularly effective when the population is heterogeneous, as it ensures that each subgroup is proportionally represented in the final sample, thereby reducing sampling error and increasing the precision of estimates by accounting for variability within and between strata.

The process of stratified sampling involves several key steps. First, the target population must be clearly defined, identifying key characteristics such as age, income level, or geographic location that are relevant to the research objectives. The population is then divided into non-overlapping and exhaustive strata, ensuring that the groups are homogeneous within themselves but distinct from each other. Once the strata are established, the sample size is determined and allocated using methods such as proportional allocation, which assigns sample sizes in proportion to the population size of each stratum; equal allocation, which assigns the same number of samples to each stratum; and optimal allocation, which considers variability and cost factors to maximize precision

| [26] | Neyman, J. (1934). On the Two Different Aspects of the Representative Method: The Method of Stratified Sampling and the Method of Purposive Selection. Journal of the Royal Statistical Society, 97(4), 558-625. https://doi.org/10.2307/2342192 |

[26]

.

Following allocation, a random sampling method, is employed within each stratum to ensure unbiased selection. The collected data is then analyzed by weighting each stratum's results according to its proportion in the population, thereby providing more accurate and reliable estimates.

Stratified sampling offers several advantages, including improved representativeness by ensuring the inclusion of key subgroups, reduced sampling error compared to simple random sampling, and the facilitation of subgroup-specific analysis and comparisons. Additionally, it allows for more efficient use of resources, particularly in studies with heterogeneous populations. However, stratified sampling also presents certain limitations, such as the need for detailed population information to properly define strata, the requirement that strata must be mutually exclusive and collectively exhaustive, and the complexity and time involved in its implementation

| [26] | Neyman, J. (1934). On the Two Different Aspects of the Representative Method: The Method of Stratified Sampling and the Method of Purposive Selection. Journal of the Royal Statistical Society, 97(4), 558-625. https://doi.org/10.2307/2342192 |

| [27] | Cochran, W. G. (1977). Sampling Techniques (3rd ed.). John Wiley & Sons. |

[26, 27]

.

4.3.2. Key Stratification Criteria Include

1) Geographic Location: People in urban, peri-urban, and rural zones, because risk associated with climate change and insurance differs.

2) Income Levels: Employed applicants who are doing low income, middle-, and higher-income earning jobs in order to learn about affordability and preferences.

3) Occupational Groups: Small-scale farmers, petty traders, and salaried employees to enable differentiation of costs according to changes in risk levels and solvency.

4) Gender and Age Dynamics: To give a diverse representation, individuals from different gender and age of the household decision makers should participate.

The required target sample size is calculated from statistical power analysis to attain the necessary sample size needed to make valid decisions.

4.4. Analytical Techniques Used

Two primary analytical techniques are employed to evaluate and compare the effectiveness of self-protection measures and climate insurance:

4.4.1. Cost-Benefit Analysis (CBA)

CBA is used to evaluate the economic feasibility of self-protection measures and climate insurance, because it allows evaluating costs and benefits and making comparison. Cost-benefit analysis (CBA) is a systematic approach used to evaluate the economic feasibility of a project, policy, or investment by comparing the total expected costs to the anticipated benefits

| [28] | Boardman, A. E., Greenberg, D. H., Vining, A. R., & Weimer, D. L. (2018). Cost-Benefit Analysis: Concepts and Practice (5th ed.). Cambridge University Press. |

[28]

. This analytical tool provides a quantitative framework to assess whether the benefits of an action outweigh its costs, thereby aiding in efficient resource allocation and informed decision-making. The process of CBA involves identifying and quantifying all relevant costs and benefits, discounting future values to present terms to account for the time value of money, and calculating key indicators such as the net present value (NPV), benefit-cost ratio (BCR), and internal rate of return (IRR).

A well-conducted CBA accounts for direct, indirect, tangible, and intangible factors, ensuring a comprehensive assessment of economic efficiency. However, the accuracy of CBA depends on the quality of data, the valuation of non-market goods, and assumptions related to discount rates and future uncertainties

| [29] | Pearce, D. W., Atkinson, G., & Mourato, S. (2006). Cost-Benefit Analysis and the Environment: Recent Developments. OECD Publishing. |

[29]

. Despite its limitations, CBA remains a widely used tool in public policy, infrastructure development, environmental planning, and business decision-making. In public sector applications, it helps governments prioritize projects by evaluating social welfare impacts alongside financial considerations

| [28] | Boardman, A. E., Greenberg, D. H., Vining, A. R., & Weimer, D. L. (2018). Cost-Benefit Analysis: Concepts and Practice (5th ed.). Cambridge University Press. |

| [29] | Pearce, D. W., Atkinson, G., & Mourato, S. (2006). Cost-Benefit Analysis and the Environment: Recent Developments. OECD Publishing. |

[28, 29]

.

In our study, key metrics include:

1) Costs: Out-of-pocket and recurrent expenditures on self-insurance; first difference and search costs of insurance.

2) Benefits: Net decrease in property and asset monetarized damages, rate of return to normalcy and enhancement of household coping capacity.

3) Net Present Value (NPV): For evaluating potential future returns on investment in self-protection and insurance contingent on different climatic conditions.

This makes it easy for CBA to give a monetary value of which strategy is producing high returns on investment under which conditions.

4.4.2. Comparative Statics

Comparative statics evaluate the behavior of households in response to shifts in outside parameters. Benchmarking is a widely used comparative analytic technique that systematically evaluates outcomes by comparing them against established standards. It serves as a powerful tool for organizations and policymakers to adopt best practices. Benchmarking involves the collection and analysis of quantitative and qualitative data to identify outcomes from different strategies

| [30] | Camp, R. C. (1989). Benchmarking: The Search for Industry Best Practices that Lead to Superior Performance. Productivity Press. |

[30]

. This method is particularly valuable in economics, business management, and public policy, where organizations seek to improve their competitive advantage and operational effectiveness.

The benchmarking process typically follows several key steps: identification of objectives and key performance indicators (KPIs), selection of benchmarking partners or data sources, data collection, analysis of performance gaps, and the implementation of improvements

| [31] | Spendolini, M. J. (1992). The Benchmarking Book. American Management Association. |

[31]

. Benchmarking can be classified into several types, including internal benchmarking, competitive benchmarking, functional benchmarking, and generic benchmarking. Internal benchmarking compares different departments or units within the same organization, while competitive benchmarking evaluates performance against direct competitors. Functional benchmarking examines processes across similar functions in different industries, and generic benchmarking seeks best practices across any industry

| [30] | Camp, R. C. (1989). Benchmarking: The Search for Industry Best Practices that Lead to Superior Performance. Productivity Press. |

| [31] | Spendolini, M. J. (1992). The Benchmarking Book. American Management Association. |

[30, 31]

. In our study, we use standard costs of different self-protection strategies to make comparisons.

Comparative statics analysis helps to evaluate the significance of economic, social, and policy factors in household decision-making. It provides insights into how changes in these factors influence household choices, allowing for a better understanding of their impact on behavior and decision outcomes. Key analyses include:

1) Income Elasticity: Insurance and self-protection relationships with first and then second household income.

2) Risk Perception: How differences in perceived climate risk change the probability of implementing one approach instead of the other.

3) Policy Changes: Measuring the effectiveness of governmental or organizational encouragement and/or penalties on choices made.

5. Economic Evaluation of Self Protection Measures

Self-protection measures refer to the various strategies households adopt to protect themselves from the adverse effects of climate change risks, such as floods, droughts, or extreme weather events. These measures can vary in complexity and cost, ranging from simple and affordable solutions to more complex and expensive ones. The choice of measures depends on factors such as household income, risk tolerance, and available resources. This section provides a detailed analysis of self-protection measures, their associated costs, and the financial implications of implementing them.

5.1. Classification of Self-Protection Measures

Self-protection measures can be classified into structural, non-structural, and behavioral interventions:

5.1.1. Structural Measures

These include actions that seek to alter either infrastructure or make investments that will help minimize exposure to climate impacts.

Examples include constructing flood-resistant homes, building water storage tanks to deal with problem of water shortages in periods of drought, improving roofs and walls to meet cyclone or high wind stresses, enhancing the system for drainage to decrease the danger of floods in urban regions.

5.1.2. Non-Structural Measures

These strategies are less related to tangible assets than to the idea of strategic positioning and management.

Examples include the diversification of income sources like agricultural and non-agricultural income, keeping grains or other kinds of food produced to help guard against further increases in the wake of a calamity, engaging in community-based disaster risk reduction programs.

5.1.3. Behavioral Measures

These include modification of belief systems and practices for enhanced climate risks preparedness.

Examples include periodic inspection and upgrading of homes and structures to improve the standings of the building systems, learning on the early signals of disasters and how to evacuate, sensitization of children and members of the community on climate risk and preparedness.

5.2. Cost Benefit Analysis of Self-Protection

A cost benefit analysis (CBA) assesses the feasibility of prevention and precautionary measures by comparing its cost with the gains made in the long run.

Costs: List both explicit and indirect costs, which are the tangible costs including construction material, wages, cost of resources, human resource, administrative, and intangible cost including maintenance and other opportunity costs of funds used. For instance, building a house that is resistant to floods entails huge initial costs, but follow-up costs are little.

Benefits: Preventing further or complete loss of resources in extreme climate-sensitive disasters, such as preventing property destruction, helps preserve resources essential for income generation. In addition to financial benefits, these preventive measures contribute to improved psychological well-being by reducing stress and uncertainty. They also enhance social standing by demonstrating resilience and preparedness within the community.

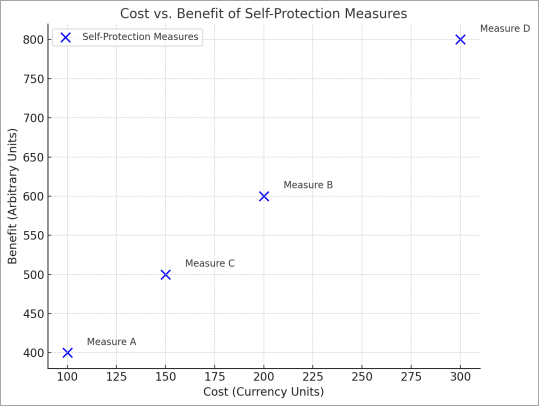

Table 1. CBA Framework for Self-Protection Measures.

Self-Protection Measure | Initial Cost (USD) | Annual Maintenance Cost (USD) | Annual Benefit (USD) | Benefit-Cost Ratio (BCR) |

Flood-Resistant Housing | 5,000 | 100 | 700 | 1.4 |

Water Storage System | 1,000 | 50 | 200 | 2.0 |

Drainage Infrastructure | 10,000 | 500 | 1,500 | 1.5 |

Measures with a Benefit-Cost Ratio (BCR) greater than 1 are economically viable, suggesting that the benefits outweigh the costs.

Figure 1. Cost vs. Benefit of Self-Protection Measures.

A graph plotting the cost on the x-axis and benefits on the y-axis highlights the most effective strategies.

5.3. The Ability of Households to Invest

Households' willingness to invest in self-protection measures depends on several factors:

5.3.1. Income Levels

Households hardly make an investment on costly measures because they have to address their needs in the shortest time possible and most of the time they cannot afford to make an investment due to financial constraints. On the other hand, the higher income families are more likely to embrace protective measures.

5.3.2. Risk Perception

This paper concludes that, consistent with the theory of risk compensation, households that anticipate higher risks of climatic disasters are more inclined to undertake self-protection. For instance, societies in the flood hazard areas will employ massive resources in the construction of flood barriers.

5.3.3. Social Influence

Group dynamics and cultural properties play a large role in capital investments. Some types of measures are catching, in the sense that if many households in a community adopt them, others will also adopt them.

5.3.4. Access to Credit and Resources

Microloans, subsidiaries or community fund availability significantly contributes towards meeting the investment for self-protection.

5.3.5. Government and NGO Support

One indirect method is through use of incentives or subsidies whereby governments and NGOs offer a cheaper-pricing for the security measures in order to encourage the population to adopt the measures.

5.4. Impediments to the Use of Protective Strategies

Self-protection measures against have a number of drawbacks despite the fact that there are so many benefits related to them. The concerns are cost, growth, and side effects.

5.4.1. High Initial Costs

Some structural self-protection measures are capital intensive at inception, costs which low-income households cannot afford. For instance, building housing that can withstand floods is more expensive than the annual income in the many rural functions.

5.4.2. Limited Scalability

Hazard mitigation measures are most of the time personal or household measures and thus cannot reduce community or regional risks adequately. For instance, a drainage system of a single compound cannot reduce floods affecting an entire compound or community.

5.4.3. Knowledge and Skill Gaps

Another limitation of self-protection measures is the lack of technical knowledge, which can prevent households from effectively implementing appropriate strategies. Without the necessary expertise, households may resort to inadequate solutions, such as constructing poorly built barriers to protect against floods, which may ultimately fail to contain the water effectively. This lack of technical know-how can undermine the effectiveness of self-protection efforts and increase vulnerability to climate-related risks.

5.4.4. Behavioral Challenges

Overestimation or underestimation of risk, or simply the absence of insurance awareness, can be an important reason why households do not act. The climate risks are managed in a non-proactive way in most households in many countries.

5.4.5. Environmental Impact

Certain types of self-protection measures may in fact harm the environment in the process. For instance, pumping of groundwater as a way of dealing with water shortage affects will result to long-term shortage of the resource.

6. Economic Evaluation of Climate Insurance

The conceptual framework used in this study reveals that climate insurance is a risk transfer tool purposely intended to safeguard households in the event of climate threats. It should be noted that unlike self-protection measures that require households to invest in advance to be compensated after a climate event, climate insurance entails the provision of financial support following an event, therefore faster recovery. This section discusses the nature, advantages, and drawbacks of climate insurance in developing countries.

6.1. Types of Climate Insurance

Several types of climate insurance products are tailored to the needs and circumstances of households in developing economies:

6.1.1. Index-Based Insurance

Definition: They rely on certain levels of rainfall, certain temperature for example or yield of the crops and not payments or claims.

Advantages: Less costly transactions, quicker payment method, and less moral hazard as payment is made for verifiable external factors and not loss making.

Example: A development of drought insurance policy that provides farmers’ insurance based on rainfall information.

6.1.2. Microinsurance

Definition: While developed for the low-income earners, this product offers protection for small incidents at equally low rates.

Advantages: Custody for the policy by vulnerable population and diversified cover for regional hazards.

Example: Microinsurance product targeting cyclone affected coastal area.

6.1.3. Agricultural Insurance

Definition: Pays for loss which is a crop or livestock or fisher and other valuable produce.

Advantages: Assists during fluctuating income for farmers as well as maintaining agricultural-based income sources.

Example: Products such as crop-pest insurance or drought insurance.

6.1.4. Parametric Insurance

Definition: By design, it is like index-based insurance in the sense that it makes a payout when a given parameter, such as wind speed or an earthquake’s magnitude, is reached.

Advantages: Payments should be prompt, visible, and have a pattern.

Example: Protection for damages caused by typhoon for which wind speed activates insurance.

6.1.5. Catastrophe Insurance Pools

Definition: Individuals or governments pool their financial resources to create a fund that provides financial protection to members of a specific community or jurisdiction in the event of unforeseen incidents. This collective approach helps ensure that individuals affected by such events have access to financial support when needed.

Advantages: Risk is distributed across a large number of individuals, ensuring that financial resources are available to address unpredictable events when they occur. This approach helps to spread the financial burden, making it more manageable and providing a reliable safety net for those affected.

Example: African Risk Capacity (ARC) that is an institution helping African member countries to mitigate risks associated with disasters.

6.2. Cost-Benefit Analysis of Climate Insurance

Climate insurance can be understood to bring specific economic advantages and disadvantages. It is cost effective by doing a cost benefit analysis to find out whether it is economical and beneficial to the households.

Costs: Premium, which is generally made on an annual or seasonal basis. Other extraneous costs which are likely to pose considerable threat to many firms are the administrative and transaction costs. Costs of insurance borne by the household as a result of utilizing less of other goods and services.

Benefits: Prompt remittance after a disaster making recovery faster. Prevention of periodic and frequent severe financial shocks that could otherwise culminate to the loss of a lot of monetary wealth in the long-run. Preservation of the assets and means of living, which can eliminate the necessity of such sales.

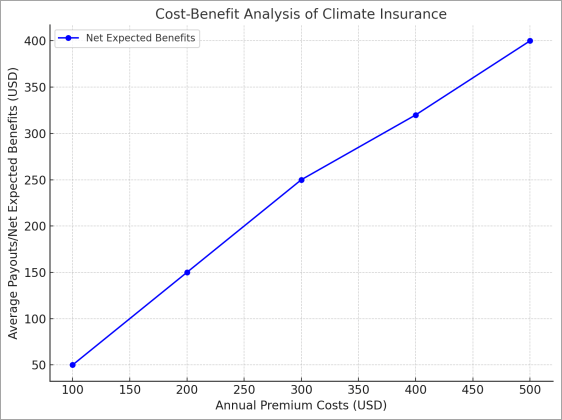

Table 2. CBA Framework for Climate Insurance.

Climate Insurance Product | Annual Premium (USD) | Average Payout (USD) | Probability of Claim (%) | Net Expected Benefit (USD) |

Drought Index Insurance | 50 | 1,000 | 10% | 50 |

Cyclone Parametric Insurance | 100 | 2,000 | 5% | 0 |

Crop Microinsurance | 20 | 500 | 15% | 55 |

Products with a higher N/E ratio have got more economical utility to households. However, affordability and probability of claims have an effect on perceived utility of the policy.

Figure 2. Evaluating the Cost and Benefit of Climate Insurance.

This is an x-y graph depicting annual premium costs on x-axis average payouts or net expected benefits on the y-axis will be easy in identifying the most effective product.

6.3. Factors Leading to Adoption Rates

The adoption of climate insurance in developing economies depends on a mix of economic, social, and institutional factors:

6.3.1. Affordability

Premiums are too costly especially to those in extremely low-income earning brackets. Affordability may be promoted by subsidies or the so-called premium-sharing schemes.

6.3.2. Risk Perception

Insurance awareness is high among the households which expect a higher exposure to climate risk. On the other hand, low risk perception results in underinvestment.

6.3.3. Awareness and Education

The extent to which people do not know about climate insurance, how it operates, the advantages of climate insurance, and how to find their way to make a claim is discouraging. An important part of this is having people know about such methods, such as through pamphlets and educational lessons on money management.

6.3.4. Trust in Providers

Antecedent events involving non-payment or delay in processing claims impact negatively on the reputation of insurers. Transparency in management and regular and timely remunerations are areas which deserve special attention.

6.3.5. Cultural and Social Norms

In some societies, people depend on those basic micro-insurance systems such as relying on the family to mitigate risks, absent the need for any formal insurance.

6.3.6. Government and Policy Support

Adoption rates increase by means of policies such as obligatory insurance of some sectors, subsidies, or tax benefits.

6.3.7. Accessibility

Accessibility of insurance firms, utilization of technology, and registration processes determine utilization.

6.4. Climate Insurance Constraints

While climate insurance provides critical financial protection, it also faces several challenges:

6.4.1. High Costs

Premiums can be too pricey for low-income individuals, which is even worse in an area that is prone to climatic change. However, the penetration increases significantly with subsidies.

6.4.2. Basis Risk

In index-based and parametric insurance, compensation is determined based on predefined benchmarks rather than the actual losses incurred. Specifically, for a farmer experiencing drought in a given region, compensation may not be provided if the average rainfall in the region exceeds the threshold set by the insurance policy. This means that even if the farmer suffers significant losses, they will not receive compensation unless the regional rainfall falls below the predetermined level.

| [1] | Cirrincione, L., Plescia, F., Ledda, C., Rapisarda, V., Martorana, D., Moldovan, R. E., & Cannizzaro, E. (2020). COVID-19 pandemic: Prevention and protection measures to be adopted at the workplace. Sustainability, 12(9), 3603. https://doi.org/10.3390/su12093603 |

| [3] | Cipollina, M., & Salvatici, L. (2008). Measuring protection: mission impossible? Journal of Economic Surveys, 22(3), 577-616. https://doi.org/10.1111/j.1467-6419.2007.00543.x |

[1, 3]

.

6.4.3. Limited Coverage

For some climatic risks, insurance may provide coverage but may not for other related economic risks. For instance, crop insurance may not include market price variation.

6.4.4. Administrative Challenges

Long and complicated enrolment procedures, delayed payment of reimbursements by insurance companies, and poor or ineffective complaint-handling systems discouraged the potential users.

6.4.5. Lack of Long-Term Support

This is because developing countries rely on external support in their operations and no serious effort has ever been made to devise a separate strategy of measurement for this type of establishment. Most insurance programs in developing countries depend on extraneous support or grants, which are perceived to be short-term measures.

6.4.6. Behavioral Barriers

Some psychological factors like optimism bias which compel the household to underestimate risks are the reasons why they cannot afford insurance even with low prices.

6.4.7. Case Studies

Case Study 1: India

PMFBY is an agricultural insurance plan sponsored by the government of India. It has certainly succeeded in deepening insurance access amongst farmers but still remains to be faced with issues like delayed payment for claims and high basis risk

| [19] | Knippenberg, E., Jensen, N., & Constas, M. (2019). Quantifying household resilience with high frequency data: Temporal dynamics and methodological options. World Development, 121, 1-15. https://doi.org/10.1016/j.worlddev.2019.04.010 |

[19]

.

Case Study 2: Kenya

The Kenya Livestock Insurance Program (KLIP) offers pastoralists with insurance that is based on an index. They use it with good results in the protection of livestock during lean season, but its main disadvantage is that it has low coverage in the most isolated communities

| [12] | Hansen, J., Hellin, J., Rosenstock, T., Fisher, E., Cairns, J., Stirling, C.,... & Campbell, B. (2019). Climate risk management and rural poverty reduction. Agricultural Systems, 172, 28-46. https://doi.org/10.1016/j.agsy.2018.01.019 |

[12]

.

7. A Comparison Between Self-Protective Approaches and Climate Insurance

Options provided between self-protection and climate insurance are derived from the viewpoints of households on climate risks. Despite their objectives, the two approaches share some differences based on costs, risk provisions, and viability. This paper will compare two approaches to obtain an understanding of their potential and limitations when undertaking policy interventions.

7.1. Comparative Cost Analysis

Measures related to financial risks involve self-protection costs and insurance costs as the initial costs, and the ongoing costs; it also identifies that different risks entail different types of costs.

7.1.1. Cost Comparison Overview

Self-Protection Measures: Usually requires significant initial commitment of resources, time, capital, for instance, building other forms of homes that are resistant to flood, erecting water storage facilities. However, the cost of carrying out the maintenance is relatively low once all the equipment have been fitted with the system

.

Climate Insurance: Actually, it implies periodic payments for which low to high expenditures may be demanded from the policyholder depending on how often and how much they will be paid out.

7.1.2. Key Observations

Self-protection measures, while expensive upfront, offer long-term cost efficiency. Climate insurance, with lower entry costs, is more accessible but may result in higher cumulative expenses for households facing frequent climate events.

Table 3. Framework for Cost Comparison.

Risk Management Strategy | Initial Cost (USD) | Recurring Costs (USD/Year) | Benefits (USD/Year) | Coverage Duration |

Flood-Resistant Housing | 5,000 | 100 | 700 | 20+ years |

Crop Insurance (Annual) | 0 | 50 | 1,000 (if triggered) | Annual |

Water Storage System | 1,000 | 50 | 200 | 10+ years |

7.2. Risk Assessment and Management Strategies

Risk management strategies differ significantly between self-protection and climate insurance:

7.2.1. Self-Protection Measures

Proactive Approach: Focused on preventing or reducing physical damage before climate events occur.

Risk Mitigation: Provides localized protection tailored to specific risks, such as flood barriers or drought-resistant crops.

Residual Risk: May not fully address all risks, especially those beyond the household’s control (e.g., regional infrastructure failures).

7.2.2. Climate Insurance

Reactive Approach: Provides financial compensation after a disaster occurs.

Risk Transfer: Shifts the financial burden of recovery to insurance providers.

Residual Risk: Relies on accurate risk modeling and timely payouts, with potential gaps due to basis risk or coverage exclusions.

Table 4. Comparison of Effectiveness in Risk Management.

Risk Dimension | Self-Protection Measures | Climate Insurance |

Financial Risk | High initial cost; mitigates future losses | Low upfront cost; recovery dependent on payouts |

Physical Risk | Reduces direct exposure to hazards | Does not reduce exposure; covers financial losses |

Accessibility | Limited by income and knowledge | Limited by premium affordability and availability |

Timeframe | Long-term prevention | Short-term recovery |

7.3. Role of External Factors

Politics, geography as well as social landscape in any given region evident through fiscal and political policies and household responses also affect risk management and the future decisions made by the latter.

| [12] | Hansen, J., Hellin, J., Rosenstock, T., Fisher, E., Cairns, J., Stirling, C.,... & Campbell, B. (2019). Climate risk management and rural poverty reduction. Agricultural Systems, 172, 28-46. https://doi.org/10.1016/j.agsy.2018.01.019 |

[12]

7.3.1. Government Policies

Subsidies and Incentives: Subsidies come under two main categories including grants for building disaster-resistant houses and climate insurance including subsiding premiums for crop insurance. These policies have a great impact on accessibility and usage of the end products

| [20] | Alinovi, L., Mane, E., & Romano, D. (2010). Measuring household resilience to food insecurity: Application to Palestinian households. Agricultural survey methods, 341-368. https://doi.org/10.1002/9780470665480.ch21 |

| [21] | Gadenne, L., & Singhal, M. (2014). Decentralization in developing economies. Annu. Rev. Econ., 6(1), 581-604. https://doi.org/10.1146/annurev-economics-080213-040833 |

[20, 21]

.

Infrastructure Development: Government spending on construction of flood gates or L-shaped gutters is another strategy that can enhance self-protection efforts done at home.

Regulations: Policymakers can initiate building codes or required forms of insurance to spur the use of certain strategies.

7.3.2. Local Economies

Economic Diversification: Some countries prioritize food security, making crop insurance more common, especially in agricultural economies where protecting farmers against losses is crucial. In contrast, other countries, particularly those with large urban populations, may focus on flood-resistant housing to safeguard households from natural disasters. The type of insurance needed depends on the country's primary concerns and economic structure.

Income Levels: The lower classes cannot afford structural interventions since they only get access to insurance at subsidized rates.

7.3.3. Community and Social Networks

Informal Risk-Sharing Mechanisms: Some cultures depend on word-of-mouth support and hence may not fully embrace the insurance concepts or self-protection of individual property.

Information Dissemination: Households are informed about existing choices by community networks who in turn make decisions.

7.3.4. Climate Variability

As a result of many climate events, more incidents may demand both personal protection and assurance while these unpredictable incidences may cause challenges.

7.4. Possibilities and Outcomes in the Long-Term

The future of self-protection efforts and climate insurance is therefore dependent on economic, environmental and institutional aspects.

7.4.1. Self-Protection Measures

1) Economic Sustainability: This can be attributed to the high costs of initial investment, hence small firms and those in low-income classes will find it very hard to scale up. On the other hand, low maintenance needs and long-lasting, make it favorably economically productive in the long run.

2) Environmental Impact: Certain actions or strategies, for example, drawing water out of the aquifers or clearings of forest for flood barriers may prove to be counterproductive environmentally. Therefore, it is mandatory that sustainability is observed in design and implementation processes.

3) Community Resilience: Minimizing household risk, self-protection plays a role in bolstering community protection.

7.4.2. Climate Insurance

1) Economic Sustainability: Insurance schemes may be, in many cases, financed through subsidies or other grants. Sustainability needs better risk aggregation, better pricing, and lower dependency on state aid.

2) Equity and Accessibility: Still, insurance can become an injustice especially when the problem of cost is elevated making it difficult for needy groups to pay for insurance. Targeted subsidies or putting into practice microinsurance models can solve this problem.

3) Adaptability: Climate insurance is subject to shifts in risk occurrence patterns as a result of climate change meaning most risk models and policy frameworks will have to be updated frequently.

8. Policy Recommendations

Managing climate impacts in developing economies requires strengthening two key strategies: self-insurance and climate vulnerability insurance, which complements self-insurance efforts. Governments play a crucial role in creating an enabling environment that supports the effective implementation of these strategies.

To mitigate climate risks in developing countries, policymakers must address financial, informational, and institutional barriers that hinder the adoption of protective measures. Financial support through subsidies, low-interest loans, and public-private partnerships can facilitate access to resilient infrastructure and technologies. Awareness campaigns and community training programs can enhance knowledge and encourage the adoption of effective self-protection strategies. Expanding access to affordable technological solutions and leveraging mobile and digital tools can improve the dissemination of critical information. Additionally, increasing climate insurance uptake through premium subsidies, risk pooling, simplified claims processes, and financial literacy programs can provide a safety net for vulnerable populations.

This section provides policy recommendations that offer a clear and comprehensive approach to addressing the challenges households face in managing climate risks.

8.1 Approaches to Increase Use of Protective Behaviors

Policymakers aiming to promote effective protective measures for households should first identify the financial, informational, and institutional constraints that hinder investment in such measures. Understanding these barriers is essential to developing targeted policies and support systems that enable households to take advantage of available opportunities for enhancing their resilience.

8.1.1. Tuition Fee Exemptions/Sponsorship and Scholarships

Subsidies: It is important to recognize that governments, as stronger centralized institutions, are best positioned to finance resilient infrastructure projects such as flood-proof housing and rainwater harvesting systems. Governments can provide financial support through grants and tax rebates, which can help offset the high initial costs and encourage widespread adoption of these resilience measures.

Low-Interest Loans: Banks should offer concessional financing with low or zero interest rates to facilitate the adoption of protective measures against climate risks. Microfinance institutions, in particular, can play a crucial role in extending financial support to low-income households, ensuring that vulnerable communities have access to resources needed for resilience-building initiatives.

Public-Private Partnerships: Governments and private companies could also work together to lower purchase costs.

8.1.2. Awareness Campaigns and Education

Risk Communication: It is essential to consistently communicate the long-term financial benefits of self-protection measures and clearly illustrate ways to minimize the risk of losses in a manner that is easily understood by households. Highlighting successful local and regional examples can serve as an effective strategy to build awareness and encourage adoption.

Community Training: Knowledgeable members of the community, including local governments and non-governmental organizations (NGOs), are well-positioned to facilitate the verification and implementation of cost-effective personal and community protection measures. These measures may include flood-proof construction techniques and agricultural practices designed to mitigate the impact of drought. By engaging with communities and providing guidance, these organizations can ensure the adoption of practical and sustainable resilience strategies.

8.1.3. Technological Accessibility and Development

Affordable Solutions: Encourage innovations and distribution of cheap and available technological mechanisms of self-protection.

Mobile and Digital Tools: Make information about self-protection measures available through electronic means with information guides and calculators on costs and disaster risk alerts.

8.1.4. Cooperation with Other Initiatives of Community Interest

Community-Led Initiatives: Ensure community-based innovations for pooled resources in the provision of protection and individual inputs that may include water storage or flood protection.

Partnerships with Local Organizations: partner with centralized NGOs and small grassroots groups to enact self-protection strategies that meet the general regional threats and poverty levels.

8.2. Approaches to Increase Climate Insurance Intake

Achieving improvements in climate insurance requires developing special strategies aimed at enhancing affordability, trust, and use.

Reducing Premium Costs: Governments can partly facilitate the premiums through subsidies and exemptions to the affected vulnerable persons to bridge the gap in the insurance costs.

Risk Pooling: Promote the largest premium base by insisting on regional or national insurance schemes enabling distribution of risks at a population level.

Bundling with Other Services: Increasing the availability of any kind of insurance might be achieved by bundling insurance with other related financial services which include agricultural credit or deposit items.

Trust and transparency can be pointed out as the main reasons that make it crucial to establish and maintain appropriate working relationships.

Reliable Payouts: The insurance system can be trusted if there is timely and accurate payment of the insurance claims. Delay in compensation removes the confidence and thus lowers future use level.