1. Introduction

The application of open budgeting systems in development is becoming more and more popular. People's lives are directly impacted by decisions made about government spending and how those decisions are carried out in practice

| [1] | Abers, R. I., Brandão, R. K., & Votto, D. (2018). Porto Alegre: Participatory Budgeting and the Challenges of Sustaining Transformative Change. Washington DC: World Resource Institute (WRI). |

[1]

. There is mounting evidence that open, inclusive budgetary systems overseen by powerful, independent supervisory organizations are the most effective means of managing public monies in an efficient and equitable manner

| [2] | Lapsley, I., & Ríos, A. M. (2015). Making sense of government budgeting: an internal transparency perspective. Qualitative Research in Accounting & Management., 12(4), 377-394. https://doi.org/10.1108/QRAM-01-2015-0014 |

[2]

. On the other hand, a lack of fiscal transparency combined with a lack of public involvement and monitoring can erode fiscal restraint, raise borrowing costs, and create a climate that encourages corruption and other leakages

| [3] | World Bank. (2015). The State of Budget Transparency, Participation and Accountability: Findings from the Open Budget Survey 2015. Washington DC: World Bank. |

[3]

.

The emergence of budget systems can be traced back to the sixteenth and seventeenth century in Europe, during which the escalating expenses of warfare necessitated higher taxation

| [4] | Krause, P. (2013). The origins of Modern Finance Ministries- An Evolutionary account based on the history of Britain and Germany. Overseas Development Institute Working, 30. |

[4]

. The United Kingdom was the pioneer in implementing a yearly national budget in the 1780s. Since then, other countries have followed suit, demonstrating an improved and more focused approach to managing public expenditure. In the early phases, budgeting mostly involved the preparation and facilitation of a thorough evaluation of performance and the subsequent incentives. From that standpoint, the enhancement in performance was driven by the need to achieve financial goals, which required organizations to function within their allocated budget. Conversely, the structure of the budget system of developing nations is secondary to the challenges of eradicating the remnants of colonial influence

| [5] | Brautigam, D., Fjeldstad, O-H., and Moore, M. (2008). Taxation and State-Building in Developing Countries: Capacity and Consent, Cambridge University Press, |

[5]

.

The increasing need to address public demands, curb corruption, and boost public sector confidence characterizes many Sub-Saharan African (SSA) nations

| [6] | Ayuso, S., Rodríguez, M. A. and Ariño, M. A. (2017). Maximizing Stakeholders’ Interests: An Empirical Analysis of the Stakeholder Approach to Corporate Governance, Business & Society, 53(3): 379-396. https://doi.org/10.1177/0007650311433122 |

[6]

. The budget has varying degrees of impact on the lives of social groupings and individuals. Nevertheless, the bulk of the impoverished, vulnerable, and socially excluded people frequently find their lives not sufficiently improved by public spending in many developing nations, including Ghana

. This could be the result of poor participatory decision-making, including a lack of accountability and misapplication of resources, among others

| [8] | Agyemang-Duah, W., Gbedoho, E. K., P, P., Arthur, F., Sobeng, A. K., & Dokbila, J. (2018). Reducing poverty through fiscal decentralisation in Ghana and beyond; A review. Cogent Economics & Finance, 6(1), 15. https://doi.org/10.1080/23322039.2018.1476035 |

[8]

.

Ghana has established legislative tools and policy frameworks to encourage public involvement in county-level financial processes; nevertheless, District Assemblies have not properly executed these policies

| [9] | SEND Ghana. (2013, December 30). Accountability Forum. Citizens' Watch, 13(32), 8. Accra, Ghana: SEND Ghana. Retrieved 3 2020. |

[9]

. Regarding the manner and timing of public engagement, the policy and legal documents likewise make generalizations without going into great depth. Some of the obstacles preventing citizens from effectively participating in the budget process have been noted by SEND Ghana

| [10] | SEND Ghana Send, G. (2016). Participatory monitoring & evaluation: SEND’s Approach to Promoting Social Accountability: Implementation Manual. https://www.google.com.gh/search |

[10]

. According to SEND Ghana

| [11] | FAO (2014). Analysis of public expenditure in support of the food and agriculture sector in Ghana, 2006-2012, FAO, Rome, www.fao.org/in-action/mafap |

[11]

, these include the politicization of the budgeting process, the lack of transparency in budget information, the absence of a structured mechanism for participation, the inadequate legislation on citizen demands for accountability, the lack of effective remedy avenues, and the insufficient capacity of citizens.

Consequently, a large portion of the population, especially those living in poverty, are not actively involved in the budgeting process or other policy-making procedures that try to tackle the significant levels of poverty and inequality prevalent in the northern parts of Ghana. The management of many Metropolitan, Municipal, and District Assemblies (MMDAs) often encounters this dilemma. The Tamale Metropolitan Assembly (TaMA) has not yet created a definitive criterion for incorporating public comments into the process of budget creation and execution. It appears that Ghana has not yet implemented a policy in this regard (SEND Ghana

| [10] | SEND Ghana Send, G. (2016). Participatory monitoring & evaluation: SEND’s Approach to Promoting Social Accountability: Implementation Manual. https://www.google.com.gh/search |

[10]

. The consequence or connotation of this situation is the pervasive discontent among the general population towards the local administration, which significantly hampers the progress and growth of local communities. In addition, citizens lack comprehension of the functions and jurisdiction of the Assemblies and may struggle to direct concerns that impact them to the right level of government

| [12] | ILGS, & FES. (2016). A Guide to District Assemblies in Ghana (Vol. 2). Accra, Greater Accra, Ghana: Friedrich Ebert Stiftung Ghana. |

[12]

. Inadequate involvement can also impact the MMDAs' revenue streams as a result of insufficient engagement with stakeholders, perhaps leading to conflicts.

Despite the overwhelming hue and cry for public budgeting to be transparent, inclusive, effective, and participatory, little empirical studies have been conducted on the determinants, effects and challenges of participation. Academics seem to shy away from conducting empirical studies on matters pertaining to public sector budgets. The only studies on issues of public budgeting are dominated by NGOs and civil society organizations such as SEND Ghana

| [11] | FAO (2014). Analysis of public expenditure in support of the food and agriculture sector in Ghana, 2006-2012, FAO, Rome, www.fao.org/in-action/mafap |

| [8] | Agyemang-Duah, W., Gbedoho, E. K., P, P., Arthur, F., Sobeng, A. K., & Dokbila, J. (2018). Reducing poverty through fiscal decentralisation in Ghana and beyond; A review. Cogent Economics & Finance, 6(1), 15. https://doi.org/10.1080/23322039.2018.1476035 |

[11, 8]

, and other parastatal units such as the Institute of Local Government Studies

. These studies lack empirical evidence as they were intended to satisfy their “paymasters” or donors.

This current study, therefore, conducts an empirical search on composite budgeting in Ghana, focusing on determinants, effects, and challenges of participation. The study seeks to address the following research questions: i). What are the determinants of stakeholder participation in composite budgeting? ii). Does the participation of all interested groups in composite budgeting have effects on the needs of vulnerable groups? and iii). What are the inherent challenges of stakeholder participation in composite budgeting?

2. Literature Review

2.1. Budget and Government Budget

A budget is typically defined as "a financial plan or a method of quantifying and converting plans for the allocation of tangible resources into monetary terms"

. A strategic plan is a detailed outline of the activities and initiatives that need to be carried out to achieve specific objectives and goals within a specified timeframe. It includes an assessment of the resources needed, as well as a comparison with previous periods and a projection of future requirements

| [15] | Bolton, A. (2021). Ideology, Unionization, and Personnel Politics in the Federal Budget Process, Journal of Public Administration Research and Theory, 31(1): 38–55, https://doi.org/10.1093/jopart/muaa032 |

[15]

. From a business standpoint, it pertains to a projection of expenses, income, and assets during a defined timeframe. It is a highly significant administrative instrument that functions as a strategic tool to accomplish measurable goals. It can serve as a benchmark for evaluating performance and as a tool for managing anticipated unfavourable circumstances. Sicilia and Steccolini

| [15] | Bolton, A. (2021). Ideology, Unionization, and Personnel Politics in the Federal Budget Process, Journal of Public Administration Research and Theory, 31(1): 38–55, https://doi.org/10.1093/jopart/muaa032 |

[15]

define a budget as the comprehensive strategic plan of a government. The statement refers to the consolidation of projected income and planned expenses, which indicates the timeline of planned actions and the methods of funding those actions

| [15] | Bolton, A. (2021). Ideology, Unionization, and Personnel Politics in the Federal Budget Process, Journal of Public Administration Research and Theory, 31(1): 38–55, https://doi.org/10.1093/jopart/muaa032 |

[15]

. According to Bolton

| [16] | Okafor, C., & Ikhatua, O. J. (2018). Budget Process and The Imperative for Institutional Reform In Nigeria: An Empirical Assessment. |

[16]

, it is also defined as "a sequence of actions aimed at achieving specific objectives."

2.2. Government Budget

A government budget, which is often approved by the legislature, is a planning document that shows anticipated public revenue and expenditure. According to Okafor and Ikhatua

, it is one of the most crucial tools for implementing economic policy when it comes to development programs. Many forms of government budgets are indicative of the many tiers of governance within a nation. Government budgets often exist in two formats: local government budgets and central, or federal, government budgets. The budgets from these entities are referred to as government budgets because they are from local government authorities such as counties, municipalities, states, and rural authorities. Typically, government budgets are divided into sectoral budgets for things like economic, health, security, education, and the environment.

Therefore, the priorities of a nation determine how resources are allocated to different sectors, and this is reflected in the budget of a government. It serves as a reliable gauge of the government's dedication to carrying out its domestic and foreign duties.

The public budget is a policy document that outlines the tactics and resources the government will employ to accomplish its goals. Its original purpose was to allocate the resources that were available, but it has gradually changed to become a contract between the government and its people, accounting for how resources are used. Ensuring overall fiscal discipline, efficient allocation, and operational efficiency are the main goals of the public budget.

The integrated budget, known as composite budgeting, incorporates all of the financial goals and programs of decentralised departments or units into the MMDA budgets, fully realising the concept of fiscal decentralisation. Planning, budgeting, financial reporting, auditing, and participation in governance at the MMDA level are all intended to be standardized.

The integrated budget known as composite budgeting incorporates all of the financial goals and programs of decentralized departments or units into the MMDA budgets, fully realizing the concept of fiscal decentralization. Planning, budgeting, financial reporting, auditing, and participation in governance at the MMDA level are all intended to be standardized.

2.3. Overview of Composite Budget in Ghana

One of the key initiatives to guarantee fiscal decentralization and participatory budgeting is the composite budget. The departments and institutions of the MMDAs aggregate their estimated revenue and expenses to create the composite budget. Its objectives have been outlined in the Local Government Act of 2016 (Act 936).

2.4. The Composite Budget System (CBS)

Section 92 Clause 3 of the Republic of Ghana's 1992 Constitution mandates policymakers to promote the overall income and spending of all ministries and agencies under the jurisdiction of individual local governments. According to the 1992 Ghanaian Constitution, a district's budget must include the total income and spending of the departments and organizations under the District Assembly and the district coordinating directorate. This includes the yearly development plans and programs of these departments and organizations. The Republic of Ghana, in the year 1993. In order to achieve effective fiscal decentralization, it is necessary for both government officials and nonprofit organizations to actively participate in the process and encourage the implementation of participatory arrangements

| [18] | Government of Ghana. (2017). Report on Management of Petroleum Revenues for the Year 2017. Accra: Public Interest and Accountability Committee (PIAC). |

[18]

.

District Assemblies can improve budgeting efficiency and accountability by merging departmental budgets using the composite budget system. According to Ghana's Ministry of Finance, a comprehensive and credible local government is necessary to conduct local programs and projects to improve Ghanaians' lives. To ensure Assemblies have appropriate budget, the Composite Budget must be implemented. It would improve district-level public money administration accountability and transparency

.

A proper legislative and regulatory framework for budget and accountability measures underpinned the Composite Budget

. The 1992 Constitution and other legislation compel Assemblies to create and implement district development plans, programs, and strategies

| [20] | Government of Ghana. (2016). Composite Budget for Metropolitan Municipal and District Assemblies. Accra: Ministry of Finance. |

[20]

. Section 92 of the Local Government Act mandates budget creation and approval for MMDAs. These statutes allow Assemblies to set and collect rates, penalties, and fees.

Before the Composite Budget, decentralized department budgets were tightly linked to their parent Ministries' Sector plans but weakly linked to the Assemblies' MTDPs and AAPs. Decentralization was hindered by district-level planning and budgetary chaos. The composite budget technique can merge departmental budgets and Central Administration Budgets of the Assemblies to improve MMDA budgeting coordination, ownership, control, and accountability. The campaign began as a trial in 2003 in Dangme West, East, and North. In 2005, it expanded to 25 districts nationwide. All districts in the nation created Composite Budgets by 2007, but never implemented them. The policy allowed all MMDAs to establish and execute Composite Budgets in 2011.

2.5. Objectives and Structure

The composite budgeting process seeks to achieve several objectives, including cost-effectiveness in the planning and implementation of district programs, comprehensive development of the MMDAs, transparency in resource utilization, efficient resource planning and utilization, a unified approach to district and national budgeting, a standardized system for monitoring, evaluation, and reporting, and determination of the total inflow and outflow of resources

.

The goal is to coordinate the Assembly's goals and programs through the budget. Every budgeting period shapes and implements MMDA policies. The composite budget implementation process must be handled to satisfy stakeholders. Local (local) and central government and agency (downstream) stakeholders interact throughout process implementation. The Ministry of Finance, DACF administrator, and Local Government Ministry are upstream players; MMDAs and decentralized organizations like the Works Department, Youth, and Sports are downstream players

| [22] | Chohan, Usman, & Kerry, J. (2016). A parliamentary budget office in Fiji: Scope and possibility. Australasian Parliamentary Review, 31(2), 117-129. |

[22]

.

3. Materials and Methods

The Tamale Metropolitan Assembly (TaMA) served as the study's location. TaMA is the sole metropolis in Ghana's five northern regions and one of the country's six metropolises. Its decision was motivated by the fact that, after Accra and Kumasi, it was the only metropolis in northern Ghana and one of the country's oldest. It is appropriate for our study because of its distinct rural and urban traits. The Metropolitan Chief Executive, the Coordinating Directors, the Budget Officers, the Planning Officers, and every unit in the Metropolis were all included in the research population. Others include leaders in the fields of tradition and religion, civil society organizations, women's organizations, individuals with disabilities (PWDs), businesspeople, taxpayers, and company owners. The rest were NGO representatives, and opinion leaders, Assembly and Unit Committee members, and heads of decentralized bodies.

To choose a sample of 90 respondents from the research population, this study used a combination of simple random sampling techniques and purposive selection approaches. The primary methods for gathering data for the study were participant observation, in-depth interviews, and questionnaires. In order to contextualize the study, the researchers collected extensive background data from the participants. These included their standing with the Assembly, the duration of their budget-making experience, and their varied roles within the Assembly. Additionally, information about their perceptions of their involvement in the Assembly's budget procedures was recorded. During the budget meetings at the Assembly, they were interviewed. To help verify the information supplied, each participant was questioned twice on different days.

To help verify the information supplied, each participant was questioned twice on different days. The length of each interview was roughly two hours. Testimonies, descriptions, and direct statements from the respondents regarding their opinions, experiences, contributions, and difficulties related to their involvement in the budget procedures were obtained through the interviews. A thorough review of TaMA budget allocation, expenditure, and auditor reports from 2013 to 2019 was also started by the academics.

Through the application of the participant observation technique, the researchers were able to gain a comprehensive picture of their varied responsibilities, engagement levels, contributions, and knowledge and comprehension of the Assembly's budgeting procedures. According to

| [23] | Pratt, B. (2019). Inclusion of marginalized groups and communities in global health research priority-setting. Journal of Empirical Res Hum Res Ethics.14(2):169-181. https://doi.org/10.1177/1556264619833858 |

[23]

participant observation aids in the researcher's comprehension of human behavior patterns and "the catalysts to various activities" that people engage in. With the use of this technique, the researchers were able to have in-depth conversations with a number of respondents, including members of the PWDs Unit Committee, chiefs, religious leaders, women's groups, and civil society organizations—all of whom are not regular employees of the Assembly. Researchers took part in the budgeting processes while immersed in the same setting as the respondents. This was to ensure that the participants understood what drives them and how they responded to stimuli. The researchers designed the interview guide after conducting a detailed and comprehensive review of the literature on composite budget processes.

4. Results and Discussions

4.1. Determinants of Stakeholder Participation in Composite Budgeting

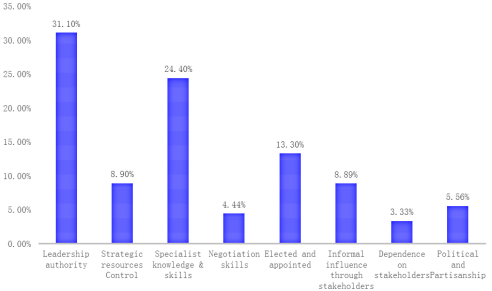

The results, as depicted on

Figure 1, show the influence of stakeholders on the composite budget. The results indicate that the stakeholder group with leadership authority (31.1%) is the main factor influencing the outcome of the composite budget. This category of stakeholders constitutes important assembly officers. They are stakeholders with specialized knowledge and abilities in budgeting (24.4%) and also have a major impact on the budget's result. Subcommittee members constitute the majority of the stakeholders, according to the survey findings. Stakeholders with control over strategic resources and those who hold elected offices or are appointed by the government are also important characteristics; these groups constitute about 4% and 9% of the total stakeholders, respectively. Furthermore, they have some bearing on how the composite budget turns out in the final analyses.

Although political affiliations and party connections have a considerable impact on stakeholders, their representation is restricted to approximately 5% of the overall responses. Generally speaking, people who depend on other parties or have unofficial relationships with others have little to no influence over financial choices.

Stakeholder power and influence on budget, tokenism, and non-participation are the three broad categories of participation and power dynamics that are supported empirically by the results, as shown in

Figure 1. This clarifies the extent of stakeholder participation as well as the real impact that stakeholders have on the process and outcomes. The level of influence possessed by stakeholders in leadership positions, their possession of specialized knowledge and skills, and their control over strategic resources are the main determinants of the impact on the Composite budget. The main participants in this situation include influential assembly members, traditional leaders, businessmen, and people who pay local taxes. Land is an important economic resource that the traditional rulers look after and is essential to the Assembly's development processes. Furthermore, as they are the main source of tax revenue, ratepayers or merchants are pivotal. The results show that there is limited control over the budget for some marginalized groups, such as women, people with disabilities, and other community members whose level of influence is mostly dependent on their representatives, like Assembly members or unit committee members. This finding corroborates Pratt's

| [24] | Gilman H. and Wampler B., (2019) “The Difference in Design: Participatory Budgeting in Brazil and the United States”, Journal of Public Deliberation 15(1). https://doi.org/10.16997/jdd.318 |

[24]

research, which demonstrated that powerful members of a community often try to sway the outcomes of devolution to suit their purposes.

Therefore, when compared to budget models that assign accountability to higher echelons of social organization, those that directly transfer authority to marginalized resource users demonstrate a stronger alignment with local interests and objectives. This research shows that strong local political and organizational power is necessary to improve residents' financial outcomes because it allows citizens to pool resources and achieve greater benefits more efficiently. The government, NGOs, donor partners, and other outside parties are essential in helping to change devolution policy and practice so that it is in line with local demands.

Figure 1. Stakeholder Group interest, importance and Influence (N=90).

4.2. An Analysis of Factors Affecting Stakeholder Engagement in Composite Budgeting

The study found that stakeholder socioeconomic background and institutional connection affect budget idea presentation. Age, knowledgeability, quantity of suggestions, perception of transparency, state and non-state players, and inclusivity are being examined. All of these variables correlate significantly with involvement.

Gilbert and Wampler

| [25] | Knlnkmk Foyeke, O. I. (2013). Employee Participation in Budgeting and Effective Budgetary Control A tool For Enhancing Organisational Performance. Factual Management Research Journal, 1(11), 11. |

| [26] | Siala, E. O. (2015). Factors Influencing Public Participation in Budget Formulation. The Case of Nairobi County. United States International University - Africa. citizens in Brazil. Studies in Comparative International Development, 41(4), 57-78. |

[25, 26]

found that socio-economic factors affect engagement. In a Nairobi County case study,

| [27] | Mabillard, V. and Zumofen, R. (2017). The complex relationship between transparency and accountability: A synthesis and contribution to existing frameworks, Public Policy and Administration, 32(2): 26-37, https://doi.org/10.1177/0952076716653651 |

[27]

revealed that education drives public budgeting involvement. Gilman and Wampler

| [25] | Knlnkmk Foyeke, O. I. (2013). Employee Participation in Budgeting and Effective Budgetary Control A tool For Enhancing Organisational Performance. Factual Management Research Journal, 1(11), 11. |

[25]

say citizens are driven to participate in Participatory Budgeting initiatives because public conversations about decision-making reduce the likelihood of clientelistic resource distribution. These sessions naturally encourage unusual perspectives

| [25] | Knlnkmk Foyeke, O. I. (2013). Employee Participation in Budgeting and Effective Budgetary Control A tool For Enhancing Organisational Performance. Factual Management Research Journal, 1(11), 11. |

[25]

. Mabillard and Zumofen,

declared that government responsibility depends on openness. A democratic government is accountable to its citizens by being transparent. Thus, the public's willingness to participate in budgeting is often attributed to its perceived transparency. This supports the idea that transparency breeds accountability. However, several experts have shown that transparency does not always lead to responsibility. They argue that the growing social science research on transparency and agency behavior should not assume a causal relationship. The claim that "if people can observe what is happening, skilled individuals will need to improve their performances" is subjective

. Transparency can sometimes lead to accountability. Which transparency promotes different accountability? Both concepts share a conceptual difficulty.

However, the budget committee may struggle because the public views the budgeting process as complicated or inaccessible. This view may reduce their involvement

| [29] | Miller, S. A., R. W. Hildreth, and Stewart, L. M., (2017). The Modes of Participation: A Revised Frame for Identifying and Analyzing Participatory Budgeting Practices, Administration and Society, 51(8). https://doi.org/10.1177/0095399717718325 |

[29]

. Annual budget announcements and reviews in Ghana show government revenue and expenditure sources, ensuring openness. However, accountability is lower in the country. Revenue transparency was 69.9% in 2012. This investigation shows that information access affects budgeting participation. Openness and accountability for budget matters can occur throughout planning, execution, auditing, and monitoring. These processes include citizen-led initiatives from CSOs or social movements and state-funded procedures from national, regional, or municipal governments. All budgeting stakeholders must communicate and create capacity. Representation promotes openness and inclusivity but can hinder efficiency and effectiveness

| [30] | Friedrich Ebert Stifung. (2016). A Guide to District Assemblies in Ghana (Vol. 2). Accra: Friedrich Ebert Stifung Ghana. |

[30]

.

4.3. Effects of Participation on the Needs of Vulnerable Groups

This section examines and discusses some of the pro-poor and gender-sensitive budget initiatives of TaMA through budget allocations and prioritization, which are measured against the needs of vulnerable groups.

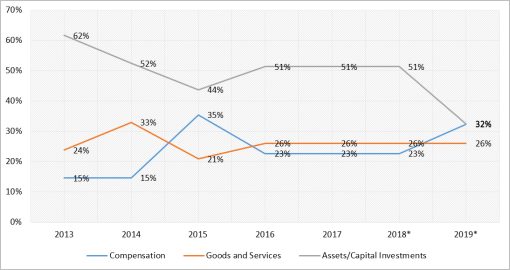

4.3.1. Annual Budget Allocation by Economic Classification

Figure 2 shows expenditure performance by economic category: labor remuneration, product and service use, and investment. Although asset expenditure declined from 62% to 32%, it remained larger than compensation and goods and services spending, except in 2019 when it equaled compensation expenditure. Product, service, and asset spending decreased between 2014 and 2015, while compensation spending rose from 15% to 35%. These findings match Ghanaian district public fund allocation. The

| [12] | ILGS, & FES. (2016). A Guide to District Assemblies in Ghana (Vol. 2). Accra, Greater Accra, Ghana: Friedrich Ebert Stiftung Ghana. |

[12]

classified budget spending as staff emoluments, traveling and transportation, general, maintenance, repairs and renewals, miscellaneous, subventions, and capital. Recurrent costs outpaced capital spending in all Ghanaian District Assemblies from 1994 to 2002. Since 2000, Metropolitan Assemblies' capital expenditures have lagged behind recurring ones. Miscellaneous recurrent expenditures have increased more

| [12] | ILGS, & FES. (2016). A Guide to District Assemblies in Ghana (Vol. 2). Accra, Greater Accra, Ghana: Friedrich Ebert Stiftung Ghana. |

[12]

.

Metropolitan Assemblies spend approximately two-thirds of total expenses, while smaller districts spend about a fifth, according to a report. Metropolitan Assemblies spend 27.5% of their budgets on human emoluments

| [8] | Agyemang-Duah, W., Gbedoho, E. K., P, P., Arthur, F., Sobeng, A. K., & Dokbila, J. (2018). Reducing poverty through fiscal decentralisation in Ghana and beyond; A review. Cogent Economics & Finance, 6(1), 15. https://doi.org/10.1080/23322039.2018.1476035 |

[8]

. Tamale's spending pattern is unique. From 2013 to 2019, capital investment expenditure averaged 51% of budgetary commitments. In 2019, it dropped to 32% to match compensation spending.

Figure 2. Annual Allocation by budget programme Economic Classification.

4.3.2. Annual Budget Allocation by Social Intervention Programmes

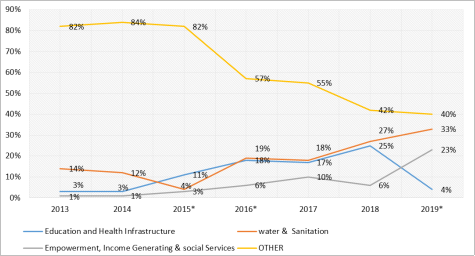

Figure 3 compares social intervention project budgets over seven years. Annual allocations show that other sectors receive significant shares compared to social intervention expenses for water and sanitation, education, health, empowerment, income production, and social and community development. Management, administration, works, physical planning, budget, and finance are the other areas. These sectors prioritize compensation and products and services over capital assets and investments. Despite large allocations to other sectors, the share of yearly expenditure has decreased from 84% in 2014 to 40% in 2019.

Empowerment, income generation, and social services have always been the lowest spending, until 2019, when they overtook health and education infrastructure. Empowerment from income-generating allocations is modest. The composite budget did not prioritize those regions due to power dynamics during budget formulation and implementation. Non-state players have little effect, while state actors and technical experts make more valuable decisions. National government investment on social intervention projects is ubiquitous. Ghana allocates 0.5% of GDP for social assistance, according to a 2016 World Bank assessment. Sub-Saharan African countries spend 2.1 percent of GDP, whereas the 35-country lower-middle-income group spends 1.6 percent.

The World Bank

| [31] | International Labour Organisation. (2014b). World Social Protection Report 2014/2015: Building economic recovery, inclusive development, and social justice. Geneva: ILO. |

[31]

reported that Lesotho spent 6.6% of its 2010 GDP on social assistance. According to available data, the Ghana School Feeding Programme has consistently received more social assistance funds than other services

| [32] | Fasona, M., Adeonipekun, P. A., Agboola, O., Akintuyi, A., Bello, A., Ogundipe, O., & Omojola, A. (2019). Incentives for collaborative governance of natural resources: A case study of forest management in southwest Nigeria. Environmental Development, 30, 78-88. https://doi.org/10.1016/j.envdev.2019.04.001 |

[32]

. This analysis does not include these expenses because the MMDAs do not have jurisdiction over them.

According to the research above, development partners can engage heavily in social intervention initiatives without using district assembly finances. The data in this area exclusively covers Tamale Metropolitan Assembly spending. Other companies undertaking their objectives without the Tamale Metropolis budget may be saving for similar products. The Assembly cannot directly monitor agency spending, but it can be informed of its type and scope.

Figure 3. Expenditure by the Social Intervention Programme.

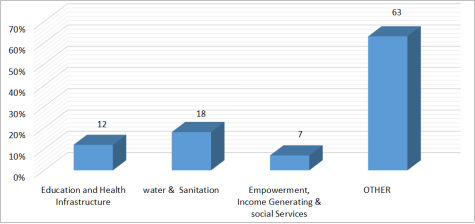

Figure 4 indicates that the expenditure on empowerment, income production, and social services, which are important factors in social intervention programs, had the lowest average performance. The Tamale Metropolitan Assembly's allocation of sixty-three percent of its expenditure to other areas, such as administration, physical planning, budgeting, and related expenses, indicates a lower emphasis on social intervention programs. The reason for these substantial expenditures is mostly due to the fact that the majority of them are classified as capital expenditures.

Figure 4. Average percentage Expenditure by Programme for 7 years.

4.4. Challenges of Stakeholder Participation in Composite Budgeting

Respondents identified three main constraints. Participants were asked to explain their biggest issues with Assembly budgets. Do you have any constraints that prevent collaboration? What factors affect women’s and disabled people's participation?

The results reveal that apathy and lack of awareness are the biggest barriers to most stakeholders' participation in the Tamale Metropolitan Assembly's Composite budgeting process. As depicted on Table 1, over 47% of state actors say stakeholders' apathy to meetings or lack of incentives is the main hurdle to effective involvement, while 28% believe insufficient information is a major barrier. An inferiority mentality and widespread female illiteracy are the biggest barriers to women's engagement. Insufficient data and political prejudice hinder efforts to help disadvantaged and vulnerable communities.

Participatory budgeting literature supports these findings. In their study "Challenges for stakeholder participation and communication within regional environmental governance,"

| [12] | ILGS, & FES. (2016). A Guide to District Assemblies in Ghana (Vol. 2). Accra, Greater Accra, Ghana: Friedrich Ebert Stiftung Ghana. |

[12]

found that a lack of adequate, timely, and exact information hinders stakeholder budgeting participation. List five Baltic Sea ecological dangers around Sweden. The study showed how difficult it is to find budgeting data. Without a clear protocol timeline, stakeholders have trouble planning their participation

| [12] | ILGS, & FES. (2016). A Guide to District Assemblies in Ghana (Vol. 2). Accra, Greater Accra, Ghana: Friedrich Ebert Stiftung Ghana. |

[12]

. Another study found that incentives for stakeholders improve governance

| [33] | Hong, S. (2015). Citizen Participation in Budgeting: A Trade‐Off between Knowledge and Inclusiveness? Public Administration Review, 75(4), 572-582. https://doi.org/10.1111/puar.12377 |

[33]

. A well-functioning company needs incentives. In exchange for individual work, successful organizations offer concrete or intangible benefits. The poor and vulnerable are hardest to prioritize due to a lack of data and politicization.

Table 1. Challenges of stakeholder participation – State Actors (N=72).

Challenge | Most important Reason/Explanation | Frequency | Percent |

Effective participation of all stakeholders | Meetings Apathy/No incentives | 34 | 47.2 |

Inadequate access to information | 20 | 27.8 |

Extreme Partisanship | 14 | 19.4 |

Inadequate resources/Funding | 4 | 5.6 |

Total | 72 | 100.0 |

Effective participation of women | Difficulty in reaching out to them | 9 | 12.5 |

Inferiority complex/low morale | 43 | 59.7 |

High level of illiteracy among women | 20 | 27.8 |

Total | 72 | 100.0 |

Targeting the needs of poor & vulnerable | Inadequate data | 45 | 33.3 |

Extreme Partisanship | 24 | 60.4 |

Inadequate resources/Funding | 3 | 6.3 |

Total | 72 | 100 |

Source: authors’ elaboration from the survey 2024

Non-state actors face similar fiscal challenges as states. The majority of respondents believed that a lack of budget technical knowledge is the largest barrier to participation. The study found the following barriers to stakeholder budgeting engagement based on narratives.

Lack of timely, accurate, and sufficient budget information and the Assembly's claimed lack of citizen accountability FGD results reflect varied attitudes on effective involvement. Some group members said they plan and budget with the assembly, but others said the local community isn't involved. Locals don't participate enough and sometimes don't know the technique. They are unaware of any public discussion the assembly plans to organize to obtain budget input.

As stated by a Hair Dressers and Tailors' Association official:

"As far as we know, there is no process. Although it may be the case in theory, they have never notified us of this type of gathering in my neighborhood” (Mr. Musah, a participant in FGD).

That was mentioned by another Petty Traders Association member.

“Although we are the main and most significant stakeholders in the decentralization process, we receive no information from our assembly members regarding the actions of the assembly. Despite the fact that we pay numerous fees annually, what does the money get used for? The results of Assembly Town Hall meetings are occasionally unknown to us.

It is quite challenging to obtain important budget information from elected Assembly members”. As per the assertion made by a Traditional authority...

These members must ensure the budget meets public needs. Representatives provide neighborhood members limited information. Directly from the audio recording transcript.

Lack of public participation was a major focus group issue. One said: "People have become indifferent towards matters of the Assembly's business due to many years of living in poverty as well as perceived government ineptitude and corruption."

Due to this, people often ignore government information, even when it is readily available, and they believe the budget has no impact on their basic needs. Directly from the audio recording transcript.

According to the analysis, stakeholders' inability to make a meaningful contribution to the planning, development, and execution of the composite budget, poor communication between the Assembly and the community, and an unclear understanding of non-state actors' budgeting obligations are the main barriers to their effective involvement in the Tamale Metropolitan Assembly's Composite Budgeting process. As argued by

| [34] | Sulemana, M., Musah, A. B, Kanlisi, K. S. (2018). An assessment of stakeholder participation in monitoring and evaluation of district assembly projects and programmes in the Savelugu- Nanton Municipality Assembly, Ghana, Ghana Journal of Development Studies, 15(1): 344-346 https://doi.org/10.4314/gjds.v15i1.9 |

[34]

, the Porto Alegre participatory governance model

| [1] | Abers, R. I., Brandão, R. K., & Votto, D. (2018). Porto Alegre: Participatory Budgeting and the Challenges of Sustaining Transformative Change. Washington DC: World Resource Institute (WRI). |

[1]

does not accurately represent the government in Sub-Saharan Africa. These findings match theirs.

5. Conclusions and Recommendations

Composite budgeting is mandatory in Ghana as per the law. It is supported by the Local Government Act of 2016 (Act 936). Composite budgeting necessitates the involvement of all dispersed entities and stakeholders. The extent to which stakeholders engage in the budgeting process is greatly impacted by their knowledge, age, and sense of the Assembly's transparency and inclusivity in the process. Additionally, the significance of the total number of proposals that each member is permitted to make during the budgeting process cannot be overlooked. The study, however, discovered that a significant level of indifference among stakeholders, limited availability of information, polarization and partisanship of the process, and insufficient funding pose substantial obstacles to composite budgeting.

In all years except for 2019, the Metropolis typically allocates a greater portion of its resources into compensation, commodities, and services. Between 2014 and 2015, there was a decrease in spending on products, services, and assets, while spending on compensation climbed from 15% to 35%. The Metropolitan Assembly's recurring expenses accounted for approximately 66% of the total expenditures, while the district legislatures' recurrent expenditures accounted for around 20% of the same cost. Throughout the time, expenditure on empowerment, income generation, and social services has consistently been the lowest, until in 2019 when it surpassed the expenditure on health and education infrastructure. The level of allocations for income production and empowerment is insufficient. Indeed, the Metropolis has not allocated funds to enhance revenue production and empowerment in the overall budget. While composite budgeting is mandated by law, the involvement and impact of non-state actors, women's groups, persons with disabilities (PWDs), and civil society organizations are taken into account. This is because power dynamics come into play during the budget planning and execution process, where decisions made by state actors and individuals with technical expertise are given more weight compared to the limited influence of marginalized non-state actors on the budget.

The study suggests that it is important to strictly follow the procedures of composite budgeting and minimize any bias in order to maintain trust and impartiality in the budgeting process. It is important to empower marginalized groups, such as women's groups, persons with disabilities (PWDS), unit committees, and assembly members, so that they can actively participate in budgeting procedures and monitoring.