Abstract

Illicit financial flows (IFFs) pose a critical threat to fiscal sustainability and development in many low-income countries, including Mozambique. Characterized by tax evasion, trade misinvoicing, offshore transfers, and corruption, IFFs have led to significant public revenue losses, particularly in the extractive sector. According to recent estimates, Mozambique loses approximately US$1.4 billion annually to these flows—undermining investments in health, education, and infrastructure. In response, the government has introduced a range of fiscal transparency reforms, including the digitalization of tax systems, creation of specialized tax units, and adherence to international standards such as the Extractive Industries Transparency Initiative (EITI). However, the effectiveness of these measures remains uncertain. This study aims to assess the extent to which fiscal transparency reforms have contributed to combating IFFs in Mozambique. Using a mixed-methods approach, the research integrates qualitative data from policy documents and interviews with key stakeholders, along with descriptive statistical analysis of revenue and compliance trends. The findings indicate modest progress in improving transparency and revenue mobilization, particularly through digital platforms and increased reporting requirements. Nevertheless, structural and institutional challenges—such as limited legal enforcement, weak coordination among oversight bodies, and the absence of a beneficial ownership registry—continue to hinder reform impact. The study concludes that while fiscal transparency initiatives are necessary, they are insufficient in isolation. A more comprehensive strategy is required—one that includes legal reforms, technological investment, capacity building, and stronger citizen engagement. The article provides policy recommendations to address these gaps and contributes to the broader debate on how developing economies can mobilize domestic resources by curbing illicit financial flows and promoting accountable fiscal governance.

|

Published in

|

Journal of World Economic Research (Volume 14, Issue 2)

|

|

DOI

|

10.11648/j.jwer.20251402.12

|

|

Page(s)

|

120-126 |

|

Creative Commons

|

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited.

|

|

Copyright

|

Copyright © The Author(s), 2025. Published by Science Publishing Group

|

Keywords

Illicit Financial Flows, Mozambique, Tax Evasion, Tax Reform, Tax Transparency

1. Introduction

Illicit financial flows (IFFs) represent one of the most pressing challenges to fiscal stability and development in low- and middle-income countries. Characterized by illegal or illegitimate movements of capital—such as tax evasion, trade misinvoicing, and money laundering—IFFs significantly reduce domestic revenues and weaken public service delivery. In the case of Mozambique, these flows are particularly concentrated in the extractive and commercial sectors, where under-invoicing of exports, offshore transfers, and corruption are recurrent practices. According to Global Financial Integrity and the Ministry of Economy and Finance, the country loses approximately US$1.4 billion annually due to IFFs, an amount that severely undermines investments in health, education, and infrastructure.

While the international literature has increasingly emphasized the role of fiscal transparency in addressing IFFs, empirical studies on its actual effectiveness remain scarce, especially in fragile and developing contexts such as Mozambique. Authors highlight the importance of open fiscal data, beneficial ownership disclosure, and international cooperation in combating evasion and improving governance

| [2] | Cobham, A., & Janský, P. (2021). Estimating Illicit Financial Flows: A Critical Guide. Global Tax Justice Journal, 3(1), 15–29. https://doi.org/10.1093/oso/9780198854418.001.0001 |

| [7] | Gaspar, V., & Mauro, P. (2022). Transparency for Development: Fiscal Institutions and the Public Trust. IMF Publications. |

[2, 7]

. However, in Mozambique, despite formal adherence to the EITI and the implementation of e-Tax systems, there is limited understanding of the real outcomes and obstacles associated with these reforms. Gaps in legal enforcement, institutional coordination, and technological capacity remain largely unaddressed in the literature.

This study aims to assess the extent to which fiscal transparency reforms have contributed to curbing illicit financial flows in Mozambique. It investigates the mechanisms that sustain IFFs, evaluates the scope and effectiveness of ongoing reforms, and identifies institutional and technical barriers that compromise progress.

By bridging the gap between normative recommendations and empirical realities, this research contributes to the academic discourse on tax justice, public sector reform, and anti-corruption strategies in developing countries. It also provides actionable policy insights for national authorities and international partners engaged in strengthening domestic resource mobilization, transparency, and accountability. The findings are particularly relevant in the context of Mozambique’s post-pandemic fiscal recovery and its commitments to global financial integrity frameworks.

The central research question is: To what extent have fiscal transparency reforms contributed to reducing illicit financial flows in Mozambique? This core inquiry is supported by the following sub-questions:

1) What are the main mechanisms of IFFs in Mozambique?

2) What fiscal transparency reforms have been implemented?

3) To what extent have these reforms contributed to the reduction of IFFs?

4) What institutional and technical challenges persist?

5) What policies can be adopted to strengthen fiscal transparency?

By answering these questions, the paper aims to offer evidence-based insights that are relevant for policymakers, international partners, and researchers interested in tax justice, public finance, and institutional reform in sub-Saharan Africa.

2. Literature Review

2.1. Concept and Mechanisms of Illicit Financial Flows

IFFs refer to the illegal or illegitimate outflow of capital from a country, compromising fiscal stability. These flows result mainly from transfer pricing manipulation, tax havens, and trade fraud

| [12] | Ndikumana, L., & Boyce, J. K. (2020). Capital Flight from Africa: Updated Methodology and New Estimates. PERI Working Paper, No. 523. |

[12]

. It is estimated that IFFs cost Africa more than US$88 billion annually

| [14] | UN (2021). Financial Integrity for Sustainable Development. United Nations. |

[14]

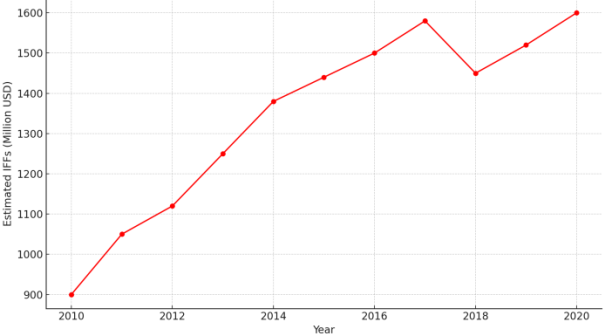

. Between 2006 and 2015, Mozambique lost an average of US$1.4 billion per year in IFFs, especially in the mining sector

. Around 30% of the state's potential revenue is nullified by tax evasion and avoidance practices

| [11] | Ministry of Economy and Finance (MEF). (2023). Annual Report on Fiscal Risks and Public Revenue. Maputo. |

[11]

.

Figure 1. Estimated illicit financial flows in Mozambique (2010-2020).

2.2. Fiscal Transparency as a Combating Strategy

Fiscal transparency is defined as the openness of fiscal, budgetary, and financial data to society. Measures such as automatic information exchange and beneficial ownership registries are crucial to curb evasion

. Fiscal transparency also improves public spending efficiency and strengthens citizen trust

| [7] | Gaspar, V., & Mauro, P. (2022). Transparency for Development: Fiscal Institutions and the Public Trust. IMF Publications. |

[7]

. Mozambique joined the EITI in 2009, leading to the periodic publication of reports on resource revenue. However, significant gaps remain in contract disclosure and beneficial ownership identification

| [5] | EITI Mozambique. (2022). Extractive Industry Transparency Report. Maputo: EITI National Committee. |

[5]

. These trends are illustrated below in the evolution of estimated illicit financial flows over a decade, with data from Global Financial Integrity (GFI) and the Ministry of Economy and Finance (MEF)

| [8] | Global Financial Integrity (GFI). (2023). Illicit Financial Flows and Developing Countries: Updated Regional Profiles. https://gfiintegrity.org/issue/illicit-financial-flows |

| [11] | Ministry of Economy and Finance (MEF). (2023). Annual Report on Fiscal Risks and Public Revenue. Maputo. |

[8, 11]

.

2.3. Institutional Challenges in Mozambique

Institutional fragility is a central obstacle to reform effectiveness. Lack of coordination between the Tax Authority, Central Bank, and Public Prosecutor’s Office hampers oversight

| [13] | Nhantumbo, E. (2024). Corruption and Fiscal Transparency in Mozambique. Mozambican Economic Journal, 8(1), 66–83. |

[13]

. The mining and petroleum sectors still operate with low transparency

. The absence of effective sanctions and weak civil society engagement worsen the situation. More than 50% of identified tax evasion cases between 2019 and 2022 did not result in sanctions

| [15] | Administrative Court. (2023). Audit and Public Accounts Report. Maputo. |

[15]

. Corruption and political interference in fiscal processes further complicate the fight against IFFs.

3. Materials and Methods

In addition to the qualitative exploratory approach already mentioned, this study incorporated quantitative elements to strengthen the analysis:

1)

Mixed Methods: Combining qualitative and quantitative data enables a more comprehensive understanding and cross-validation of results

| [3] | Creswell, J. W., & Poth, C. N. (2022). Qualitative Inquiry and Research Design: Choosing Among Five Approaches. SAGE. |

[3]

. While interviews reveal institutional perceptions and challenges, statistical data provide concrete evidence on the effectiveness of reforms.

2)

Descriptive Statistical Analysis: Applied to map the evolution of tax revenues and evasion rates, drawing on data from the MEF and GFI

| [8] | Global Financial Integrity (GFI). (2023). Illicit Financial Flows and Developing Countries: Updated Regional Profiles. https://gfiintegrity.org/issue/illicit-financial-flows |

| [11] | Ministry of Economy and Finance (MEF). (2023). Annual Report on Fiscal Risks and Public Revenue. Maputo. |

[8, 11]

.

3)

Triangulation: Triangulation across multiple sources and techniques reinforces the study's reliability and minimizes bias

| [4] | Denzin, N. K., & Lincoln, Y. S. (2021). The SAGE Handbook of Qualitative Research. SAGE. |

[4]

.

3.1. Data Collection

Reports from the Mozambican Tax Authority (ATM), MEF, GFI, Bank of Mozambique, EITI, and Administrative Court were analyzed. Interviews were conducted with 12 key informants, including ATM technicians, NGO representatives, investigative journalists, and fiscal auditors.

According to Flick, qualitative interviews capture in-depth subjective perceptions, while source triangulation strengthens the validity of findings

| [6] | Flick, U. (2022). Qualitative Inquiry – A Systematic Approach. SAGE. |

[6]

.

Table 1. Categories of Interviewees.

Category | Nº of Interviewers |

ATM Technicians | 4 |

NGO Representatives | 3 |

Investigative Journalists | 2 |

Independent Auditors | 3 |

3.2. Data Analysis

Thematic analysis was used to categorize data into themes such as “institutional progress,” “technical barriers,” and “policy proposals”

. NVivo software assisted in coding and organizing interviews. Triangulation between documents and interviews identified recurring patterns and points of divergence.

3.3. Results Analysis

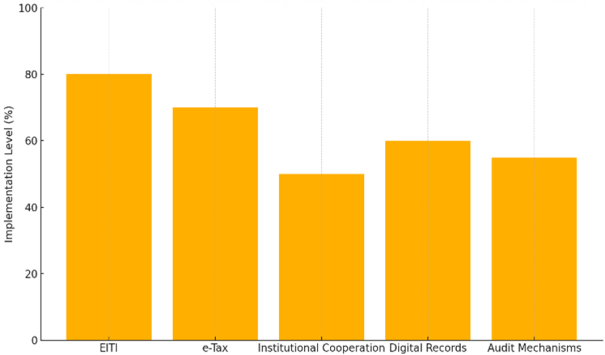

The results address each of the research sub-questions in turn. First, regarding the main mechanisms of IFFs, participants highlighted trade misinvoicing, offshore transfers, and manipulation of contract values in the extractive industries. Second, on reforms implemented, the data reveal institutional efforts such as the creation of the Large Taxpayers Unit, introduction of the e-Tax system, partial digitalization of fiscal records, and adherence to initiatives like EITI. Third, regarding the contribution of reforms, some improvements in tax compliance and revenue transparency were noted, but with uneven implementation. Fourth, institutional and technical challenges persist, such as the lack of a central beneficial ownership registry, absence of clear penalties, and low integration among key institutions, all of which continue to facilitate IFFs. Finally, the interviews and document analysis point to several policy measures needed to reinforce fiscal transparency. These findings are further illustrated through two key visual aids:

figure 2, demonstrates the progress in implementing various fiscal transparency measures between 2015 and 2023, including the deployment of e-Tax systems, EITI compliance, digital audit mechanisms, and improvements in inter-agency coordination. The bars represent annual progress scores based on institutional indicators extracted from government reports and EITI assessments. While

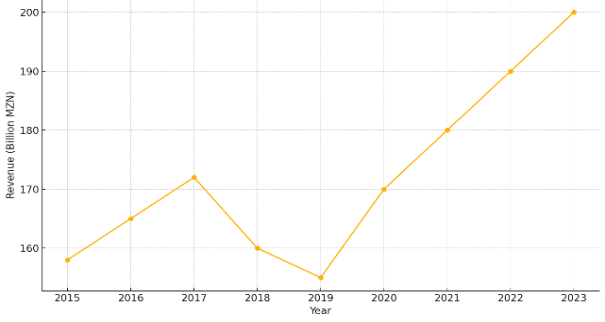

figure 3 presents the corresponding evolution in fiscal revenue over the same period, offering insight into the practical outcomes of these reforms. The visual data support the argument that despite setbacks, particularly in 2020, there is a general positive trajectory linked to reform initiatives.

Figure 2. Progress in Implementing Fiscal Transparency Measures (2015 2025).

Figure 3. Evolution of Fiscal Revenue in Mozambique (2015-2023).

The revenue trend depicted in

figure 3 reveals a general upward trajectory in Mozambique’s fiscal revenue over the nine-year period. While there is a notable dip in 2020—largely attributable to the economic slowdown caused by the COVID-19 pandemic—the overall pattern indicates positive growth. This suggests that fiscal transparency reforms and improved compliance mechanisms, despite their limitations, have started to yield tangible results. The recovery post-2020 highlights institutional resilience and signals potential for further revenue enhancement if remaining gaps in transparency and enforcement are addressed.

4. Recommendations

A comparative perspective with peer African countries further contextualizes Mozambique’s progress and limitations. For instance, Ghana has implemented a national beneficial ownership register since 2020, making corporate ownership more transparent and traceable. Kenya, on the other hand, has strengthened its Revenue Authority through the integration of Artificial Intelligence tools for tax auditing and introduced the iTax platform, which facilitates real-time taxpayer services and monitoring. Compared to these countries, Mozambique’s reforms—such as its partial digitalization of tax systems and adherence to EITI—represent a positive but incomplete step toward fiscal transparency. The absence of a fully operational beneficial ownership registry and the limited integration of Information and Communication Technologies (ICTs) in compliance monitoring remain key constraints. Drawing lessons from Ghana and Kenya could help Mozambique accelerate its institutional reforms, enhance revenue collection, and reduce illicit financial flows more effectively.

Based on the research findings and the gaps identified in institutional coordination, technological capacity, and enforcement mechanisms, a set of targeted recommendations is proposed to enhance fiscal transparency and reduce illicit financial flows in Mozambique. These measures aim to strengthen governance, promote accountability, and align the country with international best practices. The following policy actions are proposed and strategically sequenced into short-term, medium-term, and long-term measures to guide policymakers:

Short-Term: Foundational and Immediate Actions

1) Implement a national public register of beneficial ownership, as adopted in countries like Ghana and Nigeria, prioritizing the extractive and banking sectors. This measure increases transparency and deters the use of anonymous shell companies for illicit transfers.

2) Strengthen cooperation among tax, central bank, judicial oversight institutions, and financial intelligence by creating formal data sharing protocols.

3) Adopt legal provisions for mandatory disclosure of corporate structures and politically exposed persons (PEPs) in high-risk sectors.

4) Increase citizen participation and access to fiscal data, through online portals, budget dashboards, and simplified fiscal reports to boost citizen oversight.

Medium-Term: Institutional Development and Enforcement

1) Modernize the technological infrastructure of the Tax Authority, including investment in digital auditing tools and staff training on data analytics.

2) Develop an automated risk-based audit system using predictive analytics to detect anomalies in taxpayer behavior and cross-border transactions.

3) Create an independent oversight mechanism to monitor enforcement of tax-related sanctions and evaluate transparency initiatives.

4) Institutionalize public engagement mechanisms, such as participatory budget forums and whistleblower protection platforms.

Long-Term: Structural and Cultural Transformation

1) Embed fiscal transparency principles in national legislation, aligning with African Union and UN frameworks on illicit financial flows.

2) Promote a culture of compliance and tax morality, through national campaigns, civic education, and fiscal transparency in local governments.

3) Develop regional cooperation platforms with countries like Ghana, Kenya, and South Africa for joint audits, information exchange, and harmonization of tax rules to prevent profit shifting and base erosion.

4) Conduct periodic impact assessments of transparency reforms to ensure sustainability and adapt strategies based on evidence.

This strategic phasing allows Mozambique to address urgent transparency gaps while gradually building a robust institutional and technological framework to combat illicit financial flows and foster inclusive economic governance.

5. Conclusion

Fiscal transparency reforms in Mozambique represent an important step forward in addressing the systemic loss of public resources due to illicit financial flows. The implementation of digital platforms, the adherence to international initiatives like EITI, and institutional reforms such as the creation of specialized tax units are indicative of meaningful progress. However, these advances remain insufficient in isolation. Effectively combating IFFs requires not only technical solutions but also a robust institutional environment marked by accountability, inter-agency coordination, and citizen engagement. Persistent gaps in the identification of beneficial ownership, enforcement of sanctions, and political independence continue to weaken reform efforts. For transparency reforms to yield sustainable outcomes, Mozambique must invest in long-term institutional capacity, promote a culture of compliance and integrity, and strengthen partnerships with civil society and international actors. Only through such a comprehensive and inclusive approach will the country succeed in curbing IFFs and securing the revenue necessary for equitable development.

Abbreviations

ATM | Mozambique Revenue Authority |

EITI | Extractive Industries Transparency Initiative |

GFI | Global Financial Integrity |

ICTs | Information and Communication Technologies |

IFFs | Illicit Financial Flows |

IRB | Institutional Review Board |

MEF | Ministry of Economy and Finance |

MoUs | Memoranda of Understanding |

Author Contributions

Bruno Rodolfo is the sole author. The author read and approved the final manuscript.

Limitations and Ethical Considerations

The research faced notable limitations, particularly in accessing sensitive or classified data from institutions involved in fiscal oversight. Several interviewees expressed concerns about professional repercussions, resulting in reluctance to share detailed information on specific IFF-related cases. Moreover, the scarcity of recent and disaggregated statistics posed challenges to a more robust quantitative analysis.

From an ethical standpoint, the study followed all academic research standards, including voluntary participation, informed consent, and data confidentiality. Interviews were conducted with prior explanation of the research purpose, with all participants assured of anonymity and that their responses would be used exclusively for academic purposes. Data storage and processing were handled securely, and participants were given the right to withdraw at any stage of the research. These measures ensured compliance with ethical research norms and reinforced the integrity and trustworthiness of the findings.

To overcome these challenges in future research, scholars should consider the following: (i) establishing formal data-sharing agreements or with relevant fiscal and judicial institutions; (ii) leveraging anonymized administrative datasets through collaboration with public agencies oversight; and (iii) incorporating secure digital platforms for remote interviews that protect identity while enabling deeper insights. Additionally, building partnerships with civil society organizations and investigative journalists may help triangulate data sources and access case-level evidence on illicit financial flows in a safe and ethical manner.

Data Availability Statement

To craft a comprehensive Data Availability Statement for this research on illicit financial flows and fiscal transparency reforms in Mozambique, it's essential to consider the nature of data sources. Given that the study utilizes both publicly available datasets and sensitive information obtained through interviews, a combined approach is appropriate.

The data supporting the findings of this study are available from the following sources:

1) Public Datasets: Statistical data were obtained from the MEF and GFI. These datasets are publicly accessible at:

2) MEF: https://www.mef.gov.mz

3) GFI: https://gfintegrity.org

4) Qualitative Data: Due to confidentiality agreements and ethical considerations, interview transcripts and related qualitative data are not publicly available. However, anonymized excerpts relevant to the study's conclusions can be provided by the corresponding author upon reasonable request.

Conflicts of Interest

The authors declare no conflicts of interest.

References

| [1] |

Braun, V., & Clarke, V. (2021). Thematic Analysis: A Practical Guide. SAGE.

https://uk.sagepub.com/en-gb/eur/thematic-analysis/book248481

|

| [2] |

Cobham, A., & Janský, P. (2021). Estimating Illicit Financial Flows: A Critical Guide. Global Tax Justice Journal, 3(1), 15–29.

https://doi.org/10.1093/oso/9780198854418.001.0001

|

| [3] |

Creswell, J. W., & Poth, C. N. (2022). Qualitative Inquiry and Research Design: Choosing Among Five Approaches. SAGE.

|

| [4] |

Denzin, N. K., & Lincoln, Y. S. (2021). The SAGE Handbook of Qualitative Research. SAGE.

|

| [5] |

EITI Mozambique. (2022). Extractive Industry Transparency Report. Maputo: EITI National Committee.

|

| [6] |

Flick, U. (2022). Qualitative Inquiry – A Systematic Approach. SAGE.

|

| [7] |

Gaspar, V., & Mauro, P. (2022). Transparency for Development: Fiscal Institutions and the Public Trust. IMF Publications.

|

| [8] |

Global Financial Integrity (GFI). (2023). Illicit Financial Flows and Developing Countries: Updated Regional Profiles.

https://gfiintegrity.org/issue/illicit-financial-flows

|

| [9] |

Kar, D., & Spanjers, J. (2020). Illicit Financial Flows to and from Developing Countries: 2005–2014. GFI.

https://gfintegrity.org/report/illicit-financial-flows-to-and-from-developing-countries-2005-2014

|

| [10] |

Matavele, M., & Mussagy, F. (2021). Transparency in Mozambique’s Extractive Industry. CIP Working Paper, 12(3), 45–61.

https://www.cipmoz.org/wp-content/uploads/2023/03/EXTRACTIVE-SECTOR-TRANSPARENCY-INDEX-20212022.pdf

|

| [11] |

Ministry of Economy and Finance (MEF). (2023). Annual Report on Fiscal Risks and Public Revenue. Maputo.

|

| [12] |

Ndikumana, L., & Boyce, J. K. (2020). Capital Flight from Africa: Updated Methodology and New Estimates. PERI Working Paper, No. 523.

|

| [13] |

Nhantumbo, E. (2024). Corruption and Fiscal Transparency in Mozambique. Mozambican Economic Journal, 8(1), 66–83.

|

| [14] |

UN (2021). Financial Integrity for Sustainable Development. United Nations.

|

| [15] |

Administrative Court. (2023). Audit and Public Accounts Report. Maputo.

|

Cite This Article

-

APA Style

Rodolfo, B. (2025). Combatting Illicit Financial Flows in Mozambique: The Role of Tax Transparency Reforms. Journal of World Economic Research, 14(2), 120-126. https://doi.org/10.11648/j.jwer.20251402.12

Copy

|

Copy

|

Download

Download

ACS Style

Rodolfo, B. Combatting Illicit Financial Flows in Mozambique: The Role of Tax Transparency Reforms. J. World Econ. Res. 2025, 14(2), 120-126. doi: 10.11648/j.jwer.20251402.12

Copy

|

Download

AMA Style

Rodolfo B. Combatting Illicit Financial Flows in Mozambique: The Role of Tax Transparency Reforms. J World Econ Res. 2025;14(2):120-126. doi: 10.11648/j.jwer.20251402.12

Copy

|

Download

-

@article{10.11648/j.jwer.20251402.12,

author = {Bruno Rodolfo},

title = {Combatting Illicit Financial Flows in Mozambique: The Role of Tax Transparency Reforms

},

journal = {Journal of World Economic Research},

volume = {14},

number = {2},

pages = {120-126},

doi = {10.11648/j.jwer.20251402.12},

url = {https://doi.org/10.11648/j.jwer.20251402.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.jwer.20251402.12},

abstract = {Illicit financial flows (IFFs) pose a critical threat to fiscal sustainability and development in many low-income countries, including Mozambique. Characterized by tax evasion, trade misinvoicing, offshore transfers, and corruption, IFFs have led to significant public revenue losses, particularly in the extractive sector. According to recent estimates, Mozambique loses approximately US$1.4 billion annually to these flows—undermining investments in health, education, and infrastructure. In response, the government has introduced a range of fiscal transparency reforms, including the digitalization of tax systems, creation of specialized tax units, and adherence to international standards such as the Extractive Industries Transparency Initiative (EITI). However, the effectiveness of these measures remains uncertain. This study aims to assess the extent to which fiscal transparency reforms have contributed to combating IFFs in Mozambique. Using a mixed-methods approach, the research integrates qualitative data from policy documents and interviews with key stakeholders, along with descriptive statistical analysis of revenue and compliance trends. The findings indicate modest progress in improving transparency and revenue mobilization, particularly through digital platforms and increased reporting requirements. Nevertheless, structural and institutional challenges—such as limited legal enforcement, weak coordination among oversight bodies, and the absence of a beneficial ownership registry—continue to hinder reform impact. The study concludes that while fiscal transparency initiatives are necessary, they are insufficient in isolation. A more comprehensive strategy is required—one that includes legal reforms, technological investment, capacity building, and stronger citizen engagement. The article provides policy recommendations to address these gaps and contributes to the broader debate on how developing economies can mobilize domestic resources by curbing illicit financial flows and promoting accountable fiscal governance.},

year = {2025}

}

Copy

|

Download

-

TY - JOUR

T1 - Combatting Illicit Financial Flows in Mozambique: The Role of Tax Transparency Reforms

AU - Bruno Rodolfo

Y1 - 2025/08/13

PY - 2025

N1 - https://doi.org/10.11648/j.jwer.20251402.12

DO - 10.11648/j.jwer.20251402.12

T2 - Journal of World Economic Research

JF - Journal of World Economic Research

JO - Journal of World Economic Research

SP - 120

EP - 126

PB - Science Publishing Group

SN - 2328-7748

UR - https://doi.org/10.11648/j.jwer.20251402.12

AB - Illicit financial flows (IFFs) pose a critical threat to fiscal sustainability and development in many low-income countries, including Mozambique. Characterized by tax evasion, trade misinvoicing, offshore transfers, and corruption, IFFs have led to significant public revenue losses, particularly in the extractive sector. According to recent estimates, Mozambique loses approximately US$1.4 billion annually to these flows—undermining investments in health, education, and infrastructure. In response, the government has introduced a range of fiscal transparency reforms, including the digitalization of tax systems, creation of specialized tax units, and adherence to international standards such as the Extractive Industries Transparency Initiative (EITI). However, the effectiveness of these measures remains uncertain. This study aims to assess the extent to which fiscal transparency reforms have contributed to combating IFFs in Mozambique. Using a mixed-methods approach, the research integrates qualitative data from policy documents and interviews with key stakeholders, along with descriptive statistical analysis of revenue and compliance trends. The findings indicate modest progress in improving transparency and revenue mobilization, particularly through digital platforms and increased reporting requirements. Nevertheless, structural and institutional challenges—such as limited legal enforcement, weak coordination among oversight bodies, and the absence of a beneficial ownership registry—continue to hinder reform impact. The study concludes that while fiscal transparency initiatives are necessary, they are insufficient in isolation. A more comprehensive strategy is required—one that includes legal reforms, technological investment, capacity building, and stronger citizen engagement. The article provides policy recommendations to address these gaps and contributes to the broader debate on how developing economies can mobilize domestic resources by curbing illicit financial flows and promoting accountable fiscal governance.

VL - 14

IS - 2

ER -

Copy

|

Download