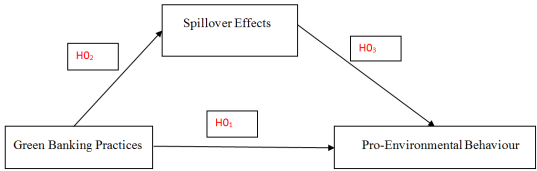

This study investigates the Impact of Green Banking Practices on the Pro-environmental behaviour of bankers in the Greater Accra Region of Ghana. Utilizing a quantitative research design, the study employs SMART PLS-SEM, SPSS version 25, and Excel to analyze the data in line with the stated objectives. The findings suggest that banks actively engage in environmental protection planning and execution, offering financing to businesses involved in eco-friendly and energy-saving programs. Furthermore, banks demonstrate a commitment to environmental sustainability by fostering a sense of responsibility and dedication to environmentally friendly operations among employees. The study highlights a pronounced positive impact of Green Banking practices on pro-environmental behaviours. Additionally, it identifies the mediating role of the spillover effect in the relationship between Green Banking practices and pro-environmental behaviour. The research suggests raising customer awareness, implementing tax reductions for green bonds, and providing subsidies for environmental preservation activities will encourage additional subscription to green banking practices. Practically, a successful green banking system in Ghana will necessitates collaboration between financial and fiscal institutions to accelerate development of a legal framework, and regulatory mechanisms for green finance, including revisions to the commercial banking law to establish environmental legal responsibilities and crafting regulations on compulsory liability insurance for environmental damages that are likely to occur as a result of non-compliance to the legal regimes for the green banking practices.

| Published in | International Journal of Accounting, Finance and Risk Management (Volume 10, Issue 1) |

| DOI | 10.11648/j.ijafrm.20251001.11 |

| Page(s) | 1-22 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Green Banking Practice, Spillover-effects, Pro-environmental Behaviour, Partial-Least Square-Structural Equation Modelling (PLS-SEM), Environmental Protection Planning, Green Finance, Employee Green Behaviour, Sustainability Performance of Banks

Frequency | Percent | ||

|---|---|---|---|

Gender | Male | 49 | 45.8 |

Female | 58 | 54.2 | |

Total | 107 | 100.0 | |

Age group | 20-29 years | 12 | 11.2 |

30-39 years | 39 | 36.4 | |

40-49 years | 38 | 35.5 | |

Over 5 0ears | 18 | 16.8 | |

Total | 107 | 100.0 | |

Years in organisation | Below one year | 7 | 6.5 |

1-3 years | 36 | 33.6 | |

4-6 years | 30 | 28.0 | |

Above 6 years | 34 | 31.8 | |

Total | 107 | 100.0 | |

Educational level | Diploma | 8 | 7.5 |

Degree | 34 | 31.8 | |

Masters | 43 | 40.2 | |

Others | 22 | 20.6 | |

Total | 107 | 100.0 | |

Current position | Officer | 21 | 19.6 |

Principal officer | 17 | 15.9 | |

Senior principal officer | 22 | 20.6 | |

Junior Officer | 15 | 14.0 | |

Manager | 32 | 29.9 | |

Total | 107 | 100.0 | |

Years in position | 1-4 years | 10 | 9.3 |

5-10 years | 24 | 22.4 | |

10+ years | 73 | 68.2 | |

Total | 107 | 100.0 | |

Item | ITEM | LOADING | CA | CR | AVE |

|---|---|---|---|---|---|

Pro-Environmental Behaviour | PEB1 | .971 | 0.783 | 0.860 | 0.606 |

PEB2 | .825 | ||||

PEB3 | .865 | ||||

PEB4 | .904 | ||||

PEB5 | .973 | ||||

Green Banking Practices | GBP1 | .864 | 0.805 | 0.871 | 0.630 |

GBP2 | .881 | ||||

GBP3 | .872 | ||||

GBP4 | .839 | ||||

GBP5 | .772 | ||||

GBP6 | .896 | ||||

Spillover Effect | SPI | .941 | 0.837 | 0.884 | 0.605 |

SP2 | .904 | ||||

SP3 | .774 | ||||

SP4 | .999 | ||||

SP5 | 1.000 |

Green Banking Practices | Pro-Environmental Behavior | Spillover | |

|---|---|---|---|

Green Banking Practices | 0.779 | ||

Pro-Environmental Behavior | 0.739 | 0.793 | |

Spillover Effect | 0.573 | 0.543 | 0.778 |

Green Banking Practices | Pro-Environmental Behaviour | Spillover Effect | |

|---|---|---|---|

GBP1 | 0.769 | 0.582 | 0.397 |

GBP2 | 0.806 | 0.613 | 0.511 |

GBP3 | 0.797 | 0.538 | 0.484 |

GBP4 | 0.741 | 0.568 | 0.383 |

PEB1 | 0.705 | 0.821 | 0.448 |

PEB3 | 0.467 | 0.752 | 0.449 |

PEB4 | 0.460 | 0.744 | 0.371 |

PEB5 | 0.657 | 0.852 | 0.454 |

SP2 | 0.443 | 0.404 | 0.775 |

SP3 | 0.442 | 0.427 | 0.780 |

SP4 | 0.579 | 0.468 | 0.798 |

SP5 | 0.394 | 0.388 | 0.777 |

SPI | 0.321 | 0.414 | 0.758 |

Green Banking Practices | Pro-Environmental Behavior | Spillover Effect | |

|---|---|---|---|

Green Banking Practices | |||

Pro-Environmental Behavior | 0.607 | ||

Spillover Effect | 0.688 | 0.657 |

VIF | |

|---|---|

GBP1 | 1.638 |

GBP2 | 1.639 |

GBP3 | 1.735 |

GBP4 | 1.490 |

PEB1 | 1.652 |

PEB3 | 1.593 |

PEB4 | 1.544 |

PEB5 | 1.918 |

SP2 | 1.815 |

SP3 | 1.715 |

SP4 | 1.732 |

SP5 | 1.807 |

SPI | 1.785 |

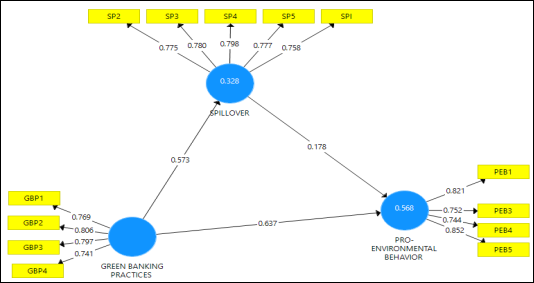

R Square | R Square Adjusted | |

|---|---|---|

Pro-Environmental Behavior | 0.568 | 0.560 |

Spillover Effect | 0.328 | 0.322 |

Total effect | Direct effect | Indirect effect | |||||||

|---|---|---|---|---|---|---|---|---|---|

coefficient | p-value | coefficient | p-value | coefficient | SD | T-value | P-value | BI (2.5%-97.5) 97.5) | |

0.739 | 0.000 | 0.637 | 0.000 | GBP-SP-PEB | 0.102 | 0.057 | 1.778 | 0.076 | 0.012-.240 |

Green Banking Practices | Pro-Environmental Behavior | Spillover | |

|---|---|---|---|

Green Banking Practices | 0.632 | 0.489 | |

Pro-Environmental Behavior | |||

Spillover Effect | 0.049 |

SSO | SSE | Q² (=1-SSE/SSO) | |

|---|---|---|---|

Green Banking Practices | 428.000 | 428.000 | |

Pro-Environmental Behavior | 428.000 | 282.911 | 0.339 |

Spillover Effect | 535.000 | 435.492 | 0.186 |

Saturated Model | Estimated Model | |

|---|---|---|

SRMR | 0.082 | 0.082 |

d_ULS | 0.609 | 0.609 |

d_G | 0.266 | 0.266 |

Chi-Square | 153.682 | 153.682 |

NFI | 0.766 | 0.766 |

Green Banking Practices | Pro-Environmental Behavior | Spillover Effect | |

|---|---|---|---|

Green Banking Practices | 1.000 | 0.739 | 0.573 |

Pro-Environmental Behavior | 0.739 | 1.000 | 0.543 |

Spillover Effect | 0.573 | 0.543 | 1.000 |

ATMs | Automated Teller Machines |

AVE | Average Variance Extracted |

CR | Composite Responsibility |

EGB | Employee Green Banking |

GBP | Green Banking Practices |

GOF | Goodness of Fit |

GB | Green Banking |

HTMT | Heterotrait-Monotrait Ratio |

PEB | Pro-Environmental Behaviour |

PLS-SEM | Partial Least Square – Structural Equation Modelling |

SPB | Sustainability Performance of Banks |

SPSS | Statistical Package for the Social Sciences |

VIF | Variance Inflation Factor |

| [1] | Akhter, I., Yasmin, S., & Faria, N. (2021). Green Banking Practices and Its Implication on Financial Performance of the Commercial Banks in Bangladesh. Journal of business administration, 42(1), 1–23. |

| [2] | Aldeen, K. N., Herianingrum, S., & Ryandono, M. N. H. (2020). Green Banking Practices: The Case of XYZ Bank in Syria. TEST Engineering & Management, 83(1), 3663–3669. |

| [3] | Ali, Q., Parveen, S., Senin, A. A., & Zaini, M. Z. (2020). Islamic bankers’ green behaviour for the growth of green banking in Malaysia. International Journal of Environment and Sustainable Development, 19(4), 393–411. |

| [4] | Tanima, S. S., & Imrul, J. (2017). Factors Influencing Customers ’ Expectation Towards Green Banking Practices Factors Influencing Customers ’ Expectation Towards Green Banking Practices in Bangladesh. European Journal of Business and Management, 9(12), 140–152. |

| [5] | Iheonu, C. O., Asongu, S. A., Odo, K. O., & Ojiem, P. K. (2020). Financial sector development and Investment in selected countries of the Economic Community of West African States: empirical evidence using heterogeneous panel data method. Financial Innovation, 6(1). |

| [6] | Okyere-Kwakye, E., & Khalil, M. N. (2021). The intention of banks to adopt green banking in an emerging market: the employees’ perspective. Economic and Political Studies, 9(4), 497–504. |

| [7] | Islam, M. S., & Hasan, M. M. (2014). Reasons behind the Practices of Green Banking by Commercial Banks: A case study on Bangladesh. European Journal of Business and Management, 7(22), 51–60. |

| [8] | Chen, J., Siddik, A. B., Zheng, G. W., Masukujjaman, M., & Bekhzod, S. (2022). The Effect of Green Banking Practices on Banks’ Environmental Performance and Green Financing: An Empirical Study. Energies, 15(4), 1–22. |

| [9] | Julia, T., & Kassim, S. (2020). Exploring green banking performance of Islamic banks vs conventional banks in Bangladesh based on Maqasid Shariah framework. Journal of Islamic Marketing, 11(3), 729–744. |

| [10] | Lien-Wen, L., & Altankhuyag, D. (2019). Impact of banking supervision on the cost-efficiency of banks: A study of five developing Asian countries. Asian Economic and Financial Review, 9(2), 213–231. |

| [11] | Setyoko, S. S., & Wijayanti, R. (2022). Green banking dan kinerja bank: mekanisme corporate governance. 10(1). |

| [12] | Khairunnessa, F., Vazquez-Brust, D. A., & Yakovleva, N. (2021). A review of the recent developments of green banking in bangladesh. Sustainability (Switzerland), 13(4), 1–21. |

| [13] | Sustainable Banking Network, & IFC. (2017). Greening the Banking System - Experiences from the Sustainable Banking Network (SBN) (Input Paper for the G20 Green Finance Study Group). 1–19. |

| [14] | Bukhari, S. A. A., Hashim, F., Amran, A. Bin, & Hyder, K. (2020). Green Banking and Islam: two sides of the same coin. Journal of Islamic Marketing, 11(4), 977–1000. |

| [15] | Campiglio, E. (2016). Beyond carbon pricing: The role of banking and monetary policy in financing the transition to a low-carbon economy. Ecological Economics, 121, 220–230. |

| [16] | Alshebami, A. S. (2021). Evaluating the relevance of green banking practices on Saudi Banks’ green image: The mediating effect of employees’ green behaviour. Journal of Banking Regulation, 22(4), 275–286. |

| [17] |

Korkmaz, S. (2015). Impact of Bank Credits on Economic Growth and Inflation. Journal of Applied Finance & Banking, 5(1), 1792–6599.

https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.1039.9346&rep=rep1&type=pdf |

| [18] | Sharma, M., & Choubey, A. (2022). Green Banking Initiatives: A Qualitative Study on Indian Banking Sector. Environment, Development and Sustainability, 24(1), 293–319. |

| [19] | Amir, K. M. (2021). Banker Attitudes and Perception towards Green Banking: An Empirical Study on Conventional Banks in Bangladesh. International Journal of Finance & Banking Studies, 10(2), 1–13. |

| [20] | Uddin, M. M. M. (2020). Green Banking Practices in Bangladesh: Bankers ’ Perception of Southeast Bank Limited. March 2019, 0–14. |

| [21] | Arumugam, D., & Chirute, T. (2018). Factors determining the adoption of green banking amongst commercial banks in Malaysia. Electronic Journal of Business & Management, 2, 50–62. |

| [22] |

Mandagie, Y. R. O., Hatta, I. H., Wahyoeni, S. I., & Ahmar, N. (2024). Development of a Green Banking and Green Financing Practice Model for Enhancing Sustainability Development Goals (SDGS). Journal of Lifestyle and SDGs Review, 5(1), e02775.

https://doi.org/10.47172/2965-730X.SDGsReview.v5.n01.pe02775 |

| [23] | Kalyar, M. N., Shoukat, A., & Shafique, I. (2019). Enhancing firms’ environmental performance and financial performance through green supply chain management practices and institutional pressures. Sustainability Accounting, Management and Policy Journal, 11(2), 451–476. |

| [24] | Owais, S., & Khan, M. (2020). Factors Affecting Bankers’ Behavioral Intention to Adopt Green Banking: An Empirical Analysis of Banks in Pakistan. Journal of Business and Social Review in Emerging Economies, 6(2), 835–843. |

| [25] | Garg, B. (2014). Human Resource-Driving Force of Sustainable Business Practices. International Journal of Innovative Research & Development, Forthcoming, Available at SSRN: |

| [26] | Rivera, J. (2014). Institutional Pressures and Voluntary Environmental Behavior in Developing Countries: Evidence From the Costa Rican Hotel Institutional Pressures and Voluntary Environmental Behavior in Developing Countries: Evidence From the Costa Rican Hotel Industry. January. |

| [27] | Jarreau, P. B. (2014). When Quotes Matter: Impact of Outside Quotes in a Science Press Release on News Judgment JCOM 13(04), A02. |

| [28] | Bhardwaj, B. R., & Malhotra, A. (2013). Green Banking Strategies: Sustainability through Corporate Entrepreneurship. Greener Journal of Business and Management Studies, 3(4), 180–193. |

| [29] | Iqbal, M., Suviitawat, A., Nisha, N., & Rifat, A. (2016). The role of commercial banks in green banking adoption: a Bangladesh perspective. International Journal of Green Economics, 10(3/4), 226. |

| [30] | Franzoni, S. (2015). Measuring the sustainability performance of the tourism sector. Tourism Management Perspectives, 16, 22–27. |

| [31] | Scott, W. (2015). Public understanding of sustainable development: Some implications for education. International Journal of Environmental and Science Education, 10(2), 235–246. |

| [32] | Sultana, N., Islam, A., & Nakib, M. (2020). Behavioural Determinants of Green Managerial Practices: A Study on Bangladeshi Bankers. International Journal of Financial Research, 11(6), 87. |

| [33] | Kitsis, A. M., & Chen, I. J. (2019). Do motives matter? Examining the relationships between motives, SSCM practices and TBL performance. Supply Chain Management, 25(3), 325–341. |

| [34] | Ahuja, N. (2015). Green banking in India: A Review of Literature. International Journal for Research in Management and Pharmacy, 4(1), 11–16. |

| [35] | Chang, R. D., Zuo, J., Zhao, Z. Y., Zillante, G., Gan, X. L., & Soebarto, V. (2017). Evolving theories of sustainability and firms: History, future directions and implications for renewable energy research. Renewable and Sustainable Energy Reviews, 72(May), 48–56. |

| [36] | Freeman, R. E. (1984). Strategic Management: A Stakeholder Approach. Boston, MA: Pitman. |

| [37] | Ackerman, F., & Eden, C. (2011). Strategic Management of Stakeholders: Theory and Practice. Long Range Planning, 44, 179-196. |

| [38] | Freeman, R. E. (1994) The Politics of Stakeholder Theory. Business Ethics Quarterly, 4, 409-421. |

| [39] | Syed, A. A. B., Hashim, F., & Amran, A. (2019). Determinants of Green Banking Adoption: A Theoretical Framework. KnE Social Sciences, 2019, 1–14. |

| [40] | Redwanuzzaman, M. (2021). The Determinants of Green Banking Adoption in Bangladesh: An Environmental Perspective. Khulna University Business Review, 24(December), 18–26. |

| [41] | Chung, P. S. (2019). Race, Social Contract Theory, and Social Darwinism. In Critical Theory and Political Theology. |

| [42] | Abuka, C., Alinda, R. K., Minoiu, C., Peydró, J. L., & Presbitero, A. F. (2019). Monetary policy and bank lending in developing countries: Loan applications, rates, and real effects. Journal of Development Economics, 139(February 2018), 185–202. |

| [43] | Jain, P., & Sharma, B. K. (2023). Impact of Green Banking Practices on Sustainable Environmental Performance and Profitability of Private Sector Banks. International Journal of Social Ecology and Sustainable Development, 14(1), 1-19. |

| [44] | Febriyanto, A., Nabiela, L. F., & Agisti, F. N. (2023). Impact of Green Financing and Financial Factors on Islamic Banks' Performance in Indonesia: A Regression Analysis. Journal of Islamic Economic Scholar, 4(2), 62-77. |

| [45] | Akomea-Frimpong, I., Adeabah, D., Ofosu, D., & Tenakwah, E. J. (2021). A review of studies on green finance of banks, research gaps and future directions. Journal of Sustainable Finance and Investment, 0(0), 1–24. |

| [46] | Mishra, K., & Aithal, P. S. (2023). Assessing the Association of Factors Influencing Green Banking Practices. International Journal of Applied Engineering and Management Letters (IJAEML), 2581-7000. |

| [47] | Karyani, E., & Obrien, V. V. (2020). Green Banking and Performance: The Role of Foreign and Public Ownership. Jurnal Dinamika Akuntansi Dan Bisnis, 7(2), 221–234. |

| [48] | Risal, N., & Joshi, S. K. (2018). Measuring Green Banking Practices on Bank’s Environmental Performance: Empirical Evidence from Kathmandu valley. Journal of Business and Social Sciences, 2(1), 44–56. |

| [49] | Malsha, K. P. P. H. G. N., Anton Arulrajah, A., & Senthilnathan, S. (2020). Mediating role of employee green behaviour towards sustainability performance of banks. Journal of Governance and Regulation, 9(2), 92–102. |

| [50] | Saunders, M., Lewis, P., & Thornhill, A. (2019). Section 4: Understanding research philosophy and approaches to theory development. In Research Methods for Business Students (Issue January). |

| [51] | Baiden, B. K., Price, A. D. F. & Dainty, A. R. J. (2006). “The Extent of Team Integration within Construction Projects,” International Journal of Project Management, Vol. 24, No. 1, pp. 13-23. |

| [52] | Creswell, J. W., & Creswell, J. D. (2018). Qualitative, Quantitative, and Mixed Methods Approaches. |

| [53] | Leavy, P. (2017). Research Design, Quantitative, Qualitative, Mixed Methods, Arts-Based and Community-Based Particularly Research Approved. The Guilford Press. |

| [54] | Elkatawneh, H. H. (2016) Comparing Qualitative and Quantitative Approaches. SSRN Electronic Journal. |

| [55] | Moore, D. F. (2016) Applied Survival Analysis Using R. Use R. Springer, Berlin. |

| [56] | Owens-Ibie, N. (2002). Socio-Cultural Considerations in Conflict Reporting in Nigeria. In U. A. Pate (Ed.), Introduction to Conflict Reporting in Nnigeria (pp. 30-44). Lagos: Frankad Publishers. |

| [57] | Mackey, A. & Gass, S. M. (2005). Second Language Research: Methodology and Design. 1st Edition, Routledge. New York. ISBN9781410612564. |

| [58] | Abawi, K. (2008). Qualitative and Quantitative Research. WHO for Medical and Educational Research. Kabul, Afghanistan. |

| [59] | Kerlinger, F. N. (1986) Foundations of Behavioral Research. 3rd Edition, Holt, Rinehart and Winston, New York. |

| [60] | Rosenthal, R., & Rosnow, R. L. (1991). Essentials of behavioral research: Methods and data analysis (2nd ed.). New York: McGraw Hill. |

| [61] | Jongbo, O. C. (2014). The Role of Research Design in a Purpose Driven Enquiry. Review of Public Administration and Management, 3(6), 87-94. |

| [62] | Sileyew, K. J. (2019). Research Design and Methodology. In Cyberspace (pp. 1-12). IntechOpen. |

| [63] | Akhtar, I. (2016). Research Design. In Research in Social Science: Interdisciplinary Perspectives (p. 17). |

| [64] | Saunders, M., Lewis, P. and Thornhill, A. (2016). Research Methods for Business Students. 7th Edition, Pearson, Harlow. |

| [65] | Muijs, D. (2015). Quantitative research. In Doing Quantitative Research in Education with SPSS (Vol. 29, Issue 31). |

| [66] | Al-Saadi, H. (2014). Demystifying Ontology and Epistemology in Research Methods. Research Gate, 1(1), 1-10. |

| [67] | Asiamah, N., Mensah, H. K., & Oteng-abayie, E. F. (2017). Do Larger Samples Really Lead to More Precise Estimates? A Simulation Study. 5(January), 9–17. |

| [68] | Krejcie, R. V. and Morgan, D. W. (1970) Determining Sample Size for Research Activities. Educational and Psychological Measurement, 30, 607-610. |

| [69] | Creswell, J. W. (2003) Research Design: Qualitative, Quantitative, and Mixed Method Approaches. Sage Publications, Thousand Oaks. |

| [70] | Creswell, J. W. (2009). Research Design: Qualitative, Quantitative, and Mixed Methods Approaches (3rd ed.). Thousand Oaks, CA: Sage Publications. |

| [71] | Oliver, R. L. (2010). Satisfaction: A Behavioural Perspective on Consumer (2nd ed.). Routledge. |

| [72] | Thomas, D. R. (2006). A General Inductive Approach for Analyzing Qualitative Evaluation Data. American Journal of Evaluation, 27, 237-246. |

| [73] | Doyle, L., Brady, A. M., & Byrne, G. (2009). An overview of mixed methods research. Journal of Research in Nursing, 14(2), 175–185. |

| [74] | Koopmans, L., Bernaards, C. M., Hildebrandt, V. H., De Vet, H. C. W., & Van Der Beek, A. J. (2014). Construct validity of the individual work performance questionnaire. Journal of Occupational and Environmental Medicine, 56(3), 331–337. |

| [75] | Rogers, J. M., Duckworth, J., Middleton, S., Steenbergen, B. & and Wilson, P. H. (2019). Elements Virtual Rehabilitation Improves Motor, Cognitive, and Functional Outcomes in Adult Stroke: Evidence from a Randomized Controlled Pilot Study. Journal of Neuro Engineering and Rehabilitation 16(56). |

| [76] |

Microsoft Excel (2016) (KB4011684) 64-Bit Edition, version 1.0. Microsoft 365

https://www.microsoft.com/en-us/download/details.aspx?id=56547. |

| [77] | Brown, T. E., Davidsson, P., & Wiklund, J. (2001). An operationalization of Stevenson's conceptualization of entrepreneurship as opportunity‐based firm behavior. Strategic management journal, 22(10), 953-968. |

| [78] | Bryman, A. (2012). Social Research Methods. Oxford: Oxford University Press. |

| [79] | Hussain, S., Fangwei, Z., Siddiqi, A. F., Ali, Z., & Shabbir, M. S. (2018). Structural Equation Model for evaluating factors affecting quality of social infrastructure projects. Sustainability (Switzerland), 10(5), 1–25. |

| [80] | Hair, J F, Hult, G. T. M., Ringle, C., Sarstedt, M., Danks, N., & Ray, S. (2021). Partial least squares structural equation modeling (PLS-SEM) using R: A workbook. In Springer. |

| [81] | Hair, J. F, Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. |

| [82] | Durrah, O. (2021). How to Use Smart PLS Software: Structural Equation Modelling ( SEM ). March. |

| [83] | Purwanto, A., Asbari, M., & Santoso, T. I. (2021). Education Management Research Data Analysis: Comparison of Results between Lisrel, Tetrad, GSCA, Amos, Smartpls, Warppls, And SPSS for Small Samples. Nidhomul Haq: Jurnal Manajemen Pendidikan Islam, 6(2), 382–399. |

| [84] | Hair, J. F., Sarstedt, M., Hopkins, L., & Kuppelwieser, V. G. (2014). Partial least squares structural equation modeling (PLS-SEM): An emerging tool in business research. European Business Review, 26(2), 106–121. |

| [85] | Kwong-Kay Wong, K. (2013). Partial Least Squares Structural Equation Modeling (PLS-SEM) Techniques Using SmartPLS. Marketing Bulletin, 24(1), 1–32. |

| [86] | Richter, N. F., Cepeda Carrión, G., Roldán, J. L., & Ringle, C. M. (2016). European Management Research Using Smart Partial Least Squares Structural Equation Modeling (PLS-SEM): Editorial. European Management Journal, 34(6), 589-597. |

| [87] | Sun, L., Ji, S., & Ye, J. (2018). Partial Least Squares. In Multi-Label Dimensionality Reduction. ISBN: 9780429148200 |

| [88] | Hair, J. F., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory and Practice, 19(2), 139–152. |

| [89] | Hair, J. F., Bush, R. P., & Ortinau, D. J. (2003). Marketing Research. Within a Changing Information Environment. In Journal of Product Innovation Management. |

| [90] | Cheah, J. H., Thurasamy, R., Memon, M. A., Chuah, F., & Ting, H. (2020). Multigroup analysis using smartpls: Step-by-step guidelines for business research. Asian Journal of Business Research, 10(3), 1–12. |

| [91] | Huang, C. (2021). Education Sciences Using PLS-SEM Model to Explore the Influencing Factors of Learning Satisfaction in Blended Learning. |

| [92] | Nath, V., Nayak, N., & Goel, A. (2014). Green Banking Practices – a Review. International Journal of Research in Business Management, 2(4), 2321–2886. |

| [93] | Jahanger, A., Balsalobre-Lorente, D., Ali, M., Samour, A., Abbas, S., Tursoy, T., & Joof, F. (2023). Going away or going green in ASEAN countries: Testing the Impact of Green Financing and Energy on Environmental Sustainability. Energy & Environment. |

| [94] | Prabhu, N., & Aithal, P. S. (2023). Quantitative ABCD Analysis of Green Banking Practices and its Impact on Using Green Banking Products. International Journal of Applied Engineering and Management Letters (IJAEML), 7(1), 28-66. |

| [95] | Latifi, M. A., Nikou, S., & Bouwman, H. (2021). Business model innovation and firm performance: Exploring causal mechanisms in SMEs. Technovation. |

| [96] | Bukhari, S. A. A., Hashim, F., & Amran, A. (2022). Pathways towards Green Banking Adoption: Moderating Role of Top management commitment. International Journal of Ethics and Systems, 38(2), 286–315. |

| [97] | Nallaluthan, K., Kamaruddin, S., Thurasamy, R., Ghouri, A. M. & Kanapathy, K. (2024). Quantitative Data Analysis using PLS-SEM (SmartPLS): Issues and Challenges in Ethical Consideration. International Business Education Journal, 17(2). |

| [98] | Ringle, C. M., da Silva, D. & Bido, D. (2014). Structural Equation Modeling with the Smartpls. Brazilian Journal of Marketing - BJM Revista Brasileira de Marketing – ReMark Edição Especial Vol 13, No. 2. Maio. |

APA Style

Zubairu, I., Atiawin, P. A., Amanquah, B. A. (2025). Examining the Impact of Spillover Effects on the Relationship Between Green Banking Practices and Pro-Environmental Behaviours Among Bankers in Ghana's Greater Accra Region. International Journal of Accounting, Finance and Risk Management, 10(1), 1-22. https://doi.org/10.11648/j.ijafrm.20251001.11

ACS Style

Zubairu, I.; Atiawin, P. A.; Amanquah, B. A. Examining the Impact of Spillover Effects on the Relationship Between Green Banking Practices and Pro-Environmental Behaviours Among Bankers in Ghana's Greater Accra Region. Int. J. Account. Finance Risk Manag. 2025, 10(1), 1-22. doi: 10.11648/j.ijafrm.20251001.11

AMA Style

Zubairu I, Atiawin PA, Amanquah BA. Examining the Impact of Spillover Effects on the Relationship Between Green Banking Practices and Pro-Environmental Behaviours Among Bankers in Ghana's Greater Accra Region. Int J Account Finance Risk Manag. 2025;10(1):1-22. doi: 10.11648/j.ijafrm.20251001.11

@article{10.11648/j.ijafrm.20251001.11,

author = {Ibrahim Zubairu and Patrick Akeba Atiawin and Benjamin Amoako Amanquah},

title = {Examining the Impact of Spillover Effects on the Relationship Between Green Banking Practices and Pro-Environmental Behaviours Among Bankers in Ghana's Greater Accra Region

},

journal = {International Journal of Accounting, Finance and Risk Management},

volume = {10},

number = {1},

pages = {1-22},

doi = {10.11648/j.ijafrm.20251001.11},

url = {https://doi.org/10.11648/j.ijafrm.20251001.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijafrm.20251001.11},

abstract = {This study investigates the Impact of Green Banking Practices on the Pro-environmental behaviour of bankers in the Greater Accra Region of Ghana. Utilizing a quantitative research design, the study employs SMART PLS-SEM, SPSS version 25, and Excel to analyze the data in line with the stated objectives. The findings suggest that banks actively engage in environmental protection planning and execution, offering financing to businesses involved in eco-friendly and energy-saving programs. Furthermore, banks demonstrate a commitment to environmental sustainability by fostering a sense of responsibility and dedication to environmentally friendly operations among employees. The study highlights a pronounced positive impact of Green Banking practices on pro-environmental behaviours. Additionally, it identifies the mediating role of the spillover effect in the relationship between Green Banking practices and pro-environmental behaviour. The research suggests raising customer awareness, implementing tax reductions for green bonds, and providing subsidies for environmental preservation activities will encourage additional subscription to green banking practices. Practically, a successful green banking system in Ghana will necessitates collaboration between financial and fiscal institutions to accelerate development of a legal framework, and regulatory mechanisms for green finance, including revisions to the commercial banking law to establish environmental legal responsibilities and crafting regulations on compulsory liability insurance for environmental damages that are likely to occur as a result of non-compliance to the legal regimes for the green banking practices.

},

year = {2025}

}

TY - JOUR T1 - Examining the Impact of Spillover Effects on the Relationship Between Green Banking Practices and Pro-Environmental Behaviours Among Bankers in Ghana's Greater Accra Region AU - Ibrahim Zubairu AU - Patrick Akeba Atiawin AU - Benjamin Amoako Amanquah Y1 - 2025/02/05 PY - 2025 N1 - https://doi.org/10.11648/j.ijafrm.20251001.11 DO - 10.11648/j.ijafrm.20251001.11 T2 - International Journal of Accounting, Finance and Risk Management JF - International Journal of Accounting, Finance and Risk Management JO - International Journal of Accounting, Finance and Risk Management SP - 1 EP - 22 PB - Science Publishing Group SN - 2578-9376 UR - https://doi.org/10.11648/j.ijafrm.20251001.11 AB - This study investigates the Impact of Green Banking Practices on the Pro-environmental behaviour of bankers in the Greater Accra Region of Ghana. Utilizing a quantitative research design, the study employs SMART PLS-SEM, SPSS version 25, and Excel to analyze the data in line with the stated objectives. The findings suggest that banks actively engage in environmental protection planning and execution, offering financing to businesses involved in eco-friendly and energy-saving programs. Furthermore, banks demonstrate a commitment to environmental sustainability by fostering a sense of responsibility and dedication to environmentally friendly operations among employees. The study highlights a pronounced positive impact of Green Banking practices on pro-environmental behaviours. Additionally, it identifies the mediating role of the spillover effect in the relationship between Green Banking practices and pro-environmental behaviour. The research suggests raising customer awareness, implementing tax reductions for green bonds, and providing subsidies for environmental preservation activities will encourage additional subscription to green banking practices. Practically, a successful green banking system in Ghana will necessitates collaboration between financial and fiscal institutions to accelerate development of a legal framework, and regulatory mechanisms for green finance, including revisions to the commercial banking law to establish environmental legal responsibilities and crafting regulations on compulsory liability insurance for environmental damages that are likely to occur as a result of non-compliance to the legal regimes for the green banking practices. VL - 10 IS - 1 ER -

Department of Accounting & Finance, Accra Technical University, Accra, Ghana

Centre for Global Economic Research, Accra, Ghana

Department of Accounting & Finance, Accra Technical University, Accra, Ghana

Information