1. Introduction

Manufacturing is crucial to Ghana's economic growth

. Manufacturing has long contributed to economic growth, employment, and exports

| [2] | Prempeh, K. B., Sekyere, A. M., & Addy, E. K. A. (2018). A Multivariate Analysis of Determinants of Profitability: Evidence from Selected Manufacturing Companies Listed on the Ghana Stock Exchange. Journal of Accounting, Business and Finance Research, 2(1), 26–33. https://doi.org/10.20448/2002.21.26.33 |

[2]

. Performance is affected by internal and external elements, including macroeconomic variables that drive the economy

. Manufacturing enterprises are heavily impacted by macroeconomic factors as inflation, currency rates, GDP growth, and interest rates

| [4] | Wijaya, L. I., Harjono, J. A., & Mahadwartha, P. A. (2022). Determinants of Profitability for Manufacturing Companies in Indonesia 2018-2020. Jurnal Riset Akuntansi Dan Keuangan, 10(2), 189–198. https://doi.org/10.17509/jrak.v10i2.45199 |

[4]

. Changing these factors can alter manufacturing costs, customer demand, finance access, and profitability

| [5] | Agegnew, A., & Gujral, T. (2022). Determinants Of Profitability: Evidence From Selected Manufacturing Company In Hawassa, Ethiopia. Journal of Positive School Psychology, 2022(6), 8309–8322. http://journalppw.com |

[5]

. Understanding the link between macroeconomic conditions and Ghana Stock Company-listed industrial businesses' profitability is important for various reasons. First, it helps policymakers and industry stakeholders assess manufacturing's vulnerability to economic changes. Second, it aids investors and corporate executives in strategic decisions including growing operations, diversifying goods, and managing risk. Macroeconomic variables affect profitability in numerous industries and nations, but few studies have examined Ghana's manufacturing sector. To my knowledge, no study has examined how macroeconomic factors impact Ghana Stock Exchange manufacturing enterprises. This study addresses this gap and offers insights that can help the manufacturing business thrive. The provided business and economic studies examine profitability, financial performance, and the effects of numerous factors on corporate results. Many studies examine macroeconomic variables and corporate performance. These studies illuminate the complicated relationship between economic conditions and corporation success across industries and locations.

| [6] | Cheong, C., & Hoang, H. V. (2021). Macroeconomic factors or firm-specific factors? An examination of the impact on corporate profitability before, during and after the global financial crisis. Cogent Economics and Finance, 9(1), 1–24. https://doi.org/10.1080/23322039.2021.1959703 |

[6]

Show that Singaporean enterprises are sensitive to macroeconomic swings, whereas

emphasises the need of controlling these elements for sustainable profitability in Nigeria.

| [4] | Wijaya, L. I., Harjono, J. A., & Mahadwartha, P. A. (2022). Determinants of Profitability for Manufacturing Companies in Indonesia 2018-2020. Jurnal Riset Akuntansi Dan Keuangan, 10(2), 189–198. https://doi.org/10.17509/jrak.v10i2.45199 |

[4]

On Indonesia and

| [8] | Mwenda, B., Ngollo, M., & Mwasota, A. (2023). Effects of Macroeconomic Variables On Performance of Listed Firms at Dar es Salaam Stock Exchange, Tanzania. Journal of Accounting Finance and Auditing Studies (JAFAS), 200–223. https://doi.org/10.32602/jafas.2023.019 |

[8]

on Tanzania provide deep insights into how macroeconomic factors including GDP, inflation, interest rates, and currency rates affect company performance. Recent research on consumer goods, healthcare, and agro-food industries

| [9] | Bertuah, E., & Sakti, I. (2019). the Financial Performance and Macroeconomic Factors in Forming Stock Return. Jurnal Riset Manajemen Dan Bisnis (JRMB) Fakultas Ekonomi UNIAT, 4(S1), 511–522. |

| [10] | Ifeyinwa, E., Nwabuisi, O., & Igwe, O. (2021). Effect of o Macr roecono omic Variable es on F inancia al Pe erforma ance of f Health hcare Manufac cturing g Firms in Nigeria a. |

| [11] | Ivković, D. (2021). Influence of Firm-Specific Determinants on the Profitability of Companies in Agri-Food Sector in Bosnia and Herzegovina: Research Project. Open Journal for Research in Economics, 4(1), 31–38. https://doi.org/10.32591/coas.ojre.0401.04031i |

[9-11]

analyse the distinct elements affecting profitability, each studies examined firm-specific and macroeconomic data to show each industries' unique difficulties and possibilities.

| [9] | Bertuah, E., & Sakti, I. (2019). the Financial Performance and Macroeconomic Factors in Forming Stock Return. Jurnal Riset Manajemen Dan Bisnis (JRMB) Fakultas Ekonomi UNIAT, 4(S1), 511–522. |

[9]

Emphasises fundamental and macroeconomic determinants on stock returns, whereas

| [10] | Ifeyinwa, E., Nwabuisi, O., & Igwe, O. (2021). Effect of o Macr roecono omic Variable es on F inancia al Pe erforma ance of f Health hcare Manufac cturing g Firms in Nigeria a. |

[10]

examines how macroeconomic variables affected healthcare manufacturing enterprises' financial performance.

Working capital management and profitability must be examined to see how macroeconomic variables affect listed manufacturing enterprises in Ghana.

| [12] | Akoto, R. K., Vitor, D. A. & Angmor, P. L. (2013) Working Capital Management and Profitability: Evidence from Ghanaian listed Manufacturing Firms. Journal of Economics and International Finance, 5, 373-379. https://doi.org/10.5897/JEIF2013.0539 |

[12]

Observed that listed Ghanaian manufacturing enterprises' profitability is affected by the number of days it takes to transform raw resources into cash. In agreement with

| [13] | Akomeah, J. & Frimpong, S. (2019). Effect of Working Capital Management on Profitability of Listed Manufacturing Companies in Ghana. International Journal of Finance and Banking Research, 5(2), 29-35. https://doi.org/10.11648/j.ijfbr.20190502.13 |

[13]

, working capital management techniques affect the profitability of listed manufacturing enterprises in Ghana.

| [2] | Prempeh, K. B., Sekyere, A. M., & Addy, E. K. A. (2018). A Multivariate Analysis of Determinants of Profitability: Evidence from Selected Manufacturing Companies Listed on the Ghana Stock Exchange. Journal of Accounting, Business and Finance Research, 2(1), 26–33. https://doi.org/10.20448/2002.21.26.33 |

[2]

Also noted that Ghana's macroeconomic climate affects manufacturing enterprises' profitability, emphasising the importance of macroeconomic variables in profitability assessment.

| [14] | Darkwah, E., Marguerite D. & Asumeng, M. (2019). The Impact of Organizational Structure and Funding Sources on the Work and Health of Employed Caregivers in Children’s Homes in Ghana. Occupational Health Science 2(1) https://doi.org/10.1007/s41542-018-0020-x |

[14]

Used logistic regression and discriminant analysis to estimate the impact of working capital management on profit in Ghanaian manufacturing and industrial firms, providing valuable insights.

Evaluated the link between working capital management strategies and returns of listed manufacturing enterprises in Ghana, emphasising the relevance of financial management practices and profitability. Economic background is important in addition to working capital management.

| [16] | Athanasoglou, P., Brissimis, S. N., & Delis, M. D. (2008). Bank-Specific, Industry-Specific and Macroeconomic Determinants of Bank Profitability. Journal of International Financial Markets, Institutions and Money, 18, 121-136. http://dx.doi.org/10.1016/j.intfin.2006.07.001 |

[16]

Explored how bank-specific, industry-specific, and macroeconomic drivers affect bank profitability, emphasising the importance of macroeconomic issues. This emphasises the role of macroeconomic factors on manufacturing business profitability. Additionally,

's study on capital structure and listed business profitability in Ghana emphasises the relevance of financial drivers of profitability. This implies that new research on macroeconomic variables and profitability would offer a more complete picture of Ghanaian manufacturing enterprises' financial performance.

| [14] | Darkwah, E., Marguerite D. & Asumeng, M. (2019). The Impact of Organizational Structure and Funding Sources on the Work and Health of Employed Caregivers in Children’s Homes in Ghana. Occupational Health Science 2(1) https://doi.org/10.1007/s41542-018-0020-x |

[14]

Use logistic regression and discriminant analysis to evaluate how working capital management affects profit in Ghanaian manufacturing and industrial enterprises. This gives useful insights, but a new study on the macroeconomic causes of profitability would broaden this understanding.

| [18] | Emeka Bennett Nwuba, E. B., Omankhanlen, A. E., Chimezie, P. O. & Lawrence Uchenna Okoye, L. U. (2020). Financial Control Systems and Financial Systems Theory: Free Cash Flow and Profitability Nexus: A comparative study of Manufacturing Firms in Nigeria and Ghana. WSEAS TRANSACTIONS on SYSTEMS and CONTROL https://doi.org/10.37394/23203.2020.15.67 |

[18]

evaluated how free cash flow affects manufacturing business profitability in Nigeria and Ghana. This shows how financial control systems affect profitability. New macroeconomic research would analyse external economic issues that may potentially affect profitability, providing a distinct perspective. Thus, a new study on the impact of macroeconomic variables on the profitability of listed manufacturing firms in Ghana is needed to better understand the macroeconomic factors that affect manufacturing companies' financial performance in Ghana's current economy.

1.1. Problem Statement

Despite its importance to Ghana's economy, the manufacturing industry confronts many problems that might hamper its development and profitability

| [19] | Otoo, F. N. K. (2020). Measuring the impact of human resource management (HRM) practices on pharmaceutical industry’s effectiveness: the mediating role of employee competencies. Employee Relations, 42(6), 1353–1380. https://doi.org/10.1108/ER-03-2019-0142 |

[19]

. Addressing these concerns requires understanding how macroeconomic variables affect listed manufacturing businesses' profitability

| [20] | Egbunike, C. F., & Okerekeoti, C. U. (2018). Macroeconomic factors, firm characteristics and financial performance: A study of selected quoted manufacturing firms in Nigeria. Asian Journal of Accounting Research, 3(2), 142–168. https://doi.org/10.1108/AJAR-09-2018-0029 |

[20]

. Specifically, this study addresses the absence of thorough research on the link between chosen macroeconomic factors and the profitability of listed manufacturing enterprises in Ghana. There is research on macroeconomic determinants and company success

| [21] | Caro, E. J. (2017). Effects of Macroeconomic Factors in the Performance of Micro Finance Institutions in Ecuador. International Journal of Economics and Financial Issues, 7(5), 547–551. http:www.econjournals.com |

| [22] | Dewi, V. I., Soei, C. T. L., & Surjoko, F. O. (2019). The impact of macroeconomic factors on firms’ profitability (evidence from fast moving consumer good firms listed on Indonesian stock exchange). Academy of Accounting and Financial Studies Journal, 23(1), 1–6. |

| [23] | Ullah, A., Pinglu, C., Ullah, S., Zaman, M., & Hashmi, S. H. (2020). The nexus between capital structure, firm-specific factors, macroeconomic factors and financial performance in the textile sector of Pakistan. Heliyon, 6(8), e04741. https://doi.org/10.1016/j.heliyon.2020.e04741 |

[21-23]

, but the manufacturing sector's particular dynamics require a specific study. Uncertainty about how inflation impacts Ghanaian listed industrial enterprises' profitability. The research above help explain business profitability across sectors and nations. Their findings reveal many study gaps and discrepancies. Studying Ghanaian manufacturing enterprises' profitability is important for understanding how many factors affect their financial performance.

Studied the link between capital structure and profitability of Ghana Stock Exchange (GSE)-listed enterprises. Working capital management and profitability in Ghanaian listed industrial enterprises have also been thoroughly researched. There is also a growing amount of study on the profitability of Ghanaian manufacturing enterprises, including firm-specific and macroeconomic aspects. The study examined how macroeconomic indicators affect the financial performance of Ghana Stock Exchange-listed manufacturing firms. In this study, GDP growth, inflation, exchange rate changes, interest rates, and government fiscal policies were examined to see how they affected these enterprises' profitability.

The literature needed additional empirical research on how macroeconomic factors affect Ghanaian manufacturing enterprises' profitability. Previous study has examined how macroeconomic factors affect company performance, but little has been done on Ghana's industrial sector. Few research examines how different macroeconomic factors affect company profitability

| [24] | Agyei-Mensah, B. K. 2012. "Association between firm-specific characteristics and levels of disclosure of financial information of rural banks in the Ashanti region of Ghana," Journal of Applied Finance & Banking, SCIENPRESS Ltd, vol. 2(1), pages 1-3. |

| [25] | Quartey, P. (2003) Financing Small and Medium Enterprises (SMEs) inGhana, Journal of African Business, 4: 1, 37-55, https://doi.org/10.1300/j156v04n01_03 |

[24, 25]

. This study was motivated by the need to understand how macroeconomic issues affect Ghanaian manufacturing enterprises' finances. This research examined the link between macroeconomic factors and business profitability to inform manufacturing policymakers, investors, and managers. This study may assist Ghanaian enterprises manage the changing economy

| [24] | Agyei-Mensah, B. K. 2012. "Association between firm-specific characteristics and levels of disclosure of financial information of rural banks in the Ashanti region of Ghana," Journal of Applied Finance & Banking, SCIENPRESS Ltd, vol. 2(1), pages 1-3. |

| [25] | Quartey, P. (2003) Financing Small and Medium Enterprises (SMEs) inGhana, Journal of African Business, 4: 1, 37-55, https://doi.org/10.1300/j156v04n01_03 |

[24, 25]

. This study has a narrow focus to guarantee feasibility and relevance. The research only covers Ghanaian manufacturing. This research examines Ghana Stock Exchange-listed manufacturing enterprises. The research examines inflation, currency rates, GDP growth, and interest rates. To focus on manufacturing trends and profitability, the analysis in this study excludes other industries but used secondary data from listed manufacturing business’s financial reports, economic databases, Bank of Ghana and Ghana Statistical Service publications.

1.2. Research Objectives

In evaluating how certain macroeconomic factors relate to the profitability of Ghanaian listed manufacturing companies, the research attempts to:

1) Examine the impact of inflation on the profitability of listed manufacturing firms in Ghana.

2) Analyse the influence of exchange rate fluctuations on the profitability of listed manufacturing firms.

3) Assess the relationship between GDP growth rates and the financial performance of listed manufacturing firms:

4) Investigate the impact of interest rate changes on the financial performance of listed manufacturing firms:

5) Identify potential moderating factors that may influence the relationship between macroeconomic variables and the financial performance of listed manufacturing firms.

1.3. Research Questions

In attempt to meet the objectives of this study, the paper seeks answers to the following research questions:

1) How does inflation impact the profitability of listed manufacturing firms in Ghana?

2) What is the influence of exchange rate fluctuations on the profitability of listed manufacturing firms in both domestic and international markets?

3) How does GDP growth rate relate to the financial performance of listed manufacturing firms in Ghana?

4) How does interest changes rate impact on the financial performance of listed manufacturing firms?

5) Are there any moderating factors that influence the relationship between selected macroeconomic variables and profitability in the manufacturing sector in Ghana?

This study took into account earlier research on profitability and macroeconomic variables across different sectors and countries. Prioritization was given to earlier Ghanaian manufacturing studies. The research's theoretical framework is explained in this section. The main concepts, variables, and hypothesized relationships between profitability and macroeconomic factors are introduced. The research methodology is described in full in Section Three, which also addresses variables, data analysis, sample selection, data collection, and study design. Data analysis and research findings are covered in Section Four, which also includes specifics of the findings from the regression and correlation analyses. The study's findings, including statistical analysis and explanations of profitability and macroeconomic variables, were presented. The study's findings, summary, conclusion, and suggestions were highlighted in the last part. The results of the study are examined in this section in relation to the goals and questions. The results were evaluated for their impact on Ghanaian manufacturing and contrasted with previous research. The section ends based on the findings of the study. The section outlines study limitations, talks about implications, and summarizes important findings. It ends with helpful suggestions for investors, governments, business executives, and manufacturing companies.

2. Literature Review

2.1. Overview of the Manufacturing Sector of Ghana

Manufacturing in Ghana is vital to the economy, providing jobs, value, and exports

| [26] | Avevor, E. E. (2016). Challenges Faced By SMEs When Accessing Fund From Financial Institutions In Ghana. University of Applied Sciences, 65. |

[26]

. It includes several sectors that turn raw resources into finished commodities for home and international markets. Environment affects sector performance and growth

. Food processing, textiles and garments, chemical and pharmaceutical items, metal and equipment, wood and furniture, and plastic products make up Ghana's manufacturing industry. Each sub-industry boosts sector growth

| [2] | Prempeh, K. B., Sekyere, A. M., & Addy, E. K. A. (2018). A Multivariate Analysis of Determinants of Profitability: Evidence from Selected Manufacturing Companies Listed on the Ghana Stock Exchange. Journal of Accounting, Business and Finance Research, 2(1), 26–33. https://doi.org/10.20448/2002.21.26.33 |

[2]

. Ghana's industrial industry employs a major share of the workforce, especially in cities. SMEs reduce unemployment and poverty, improving social welfare

| [28] | Yanney, J. P. (2014). Business Strategy and Leadership Style: Impact on Organizational Performance in the Manufacturing Sector of Ghana. American Journal of Industrial and Business Management, 04(12), 767–775. https://doi.org/10.4236/ajibm.2014.412083 |

[28]

. Ghanaian manufacturers target regional and worldwide markets with export-oriented products. Export-focused research boosts the country's trade balance and foreign exchange revenues. Ghana's GDP relies on manufacturing

| [29] | Ackah, C., Adjasi, C., & Turkson, F. (2014). Scoping study on the evolution of industry in Ghana. WIDER Working Paper, 2014/075(1), 1–37. |

[29]

GDP share shows the sector's role in economic growth and development. The sector includes huge companies and many SMEs. SMEs drive sector growth through innovation, employment creation, and localised economic development

. The manufacturing sector struggles with poor infrastructure, particularly energy and transportation. Manufacturing enterprises, especially SMEs, struggle to get reasonable finance. Investment in contemporary technology, equipment, and expansion requires sufficient funding

| [26] | Avevor, E. E. (2016). Challenges Faced By SMEs When Accessing Fund From Financial Institutions In Ghana. University of Applied Sciences, 65. |

[26]

. The Ghanaian government has enacted strategies to boost the manufacturing sector, which is vital to economic growth. The government has developed industrialization plans to boost value addition and manufacturing's contribution of GDP. High-growth subsectors are prioritised. Ghanaian export promotion efforts attempt to boost international competitiveness. These activities aim to diversify export profits and minimise raw material dependence. Tax cuts, export incentives, and financing facilities are offered by the government to promote local and international industrial enterprises. Technology transfer and skills development are encouraged by the government to boost sector productivity and technology

| [2] | Prempeh, K. B., Sekyere, A. M., & Addy, E. K. A. (2018). A Multivariate Analysis of Determinants of Profitability: Evidence from Selected Manufacturing Companies Listed on the Ghana Stock Exchange. Journal of Accounting, Business and Finance Research, 2(1), 26–33. https://doi.org/10.20448/2002.21.26.33 |

[2]

. SMEs help the Ghanaian manufacturing sector, however infrastructure, production costs, import rivalry, and funding are issues

| [30] | Osei, A., Yunfei, S., Appienti, W., & Forkuoh, S. (2016). Product Innovation and SMEs Performance in the Manufacturing Sector of Ghana. British Journal of Economics, Management & Trade, 15(3), 1–14. https://doi.org/10.9734/bjemt/2016/29906 |

[30]

. Regional integration, export diversification, and harnessing the country's natural resources and agricultural potential offer economic chances. Manufacturing in Ghana boosts GDP, jobs, and exports. Addressing the sector's issues and maximising its sustainable growth and development requires government assistance and appropriate policies.

2.2. Theoretical Literature Review

The study on the relationship between selected macroeconomic variables and the profitability of listed manufacturing firms in Ghana is likely to draw on several economic and financial theories to provide a theoretical framework and guidance for the research. Some of the key theories that underpin this study include:

2.2.1. Neoclassical Theory

Supply and demand, rational corporate decision-making, and market efficiency underpin neoclassical economics

Neoclassical theory may help explain how macroeconomic variables like inflation and interest rates affect firms' production costs, borrowing costs, and investment decisions, which affect their profitability

| [32] | Brancaccio, E., Garbellini, N., & Giammetti, R. (2018). Structural labour market reforms, GDP growth and the functional distribution of income. Structural Change and Economic Dynamics. https://doi.org/10.1016/j.strueco.2017.09.001 |

[32]

. Neoclassical economic theory, based on supply and demand, rational decision-making, and market efficiency, illuminates the complex link between macroeconomic factors and manufacturing business profitability

| [33] | Priewe, J. (2017). Review of exchange-rate theories in four leading economics textbooks. European Journal of Economics and Economic Policies: Intervention, 14(1), 32–47. https://doi.org/10.4337/ejeep.2017.01.04 |

[33]

. In this study, neoclassical theory helps explain how macroeconomic indices like inflation and interest rates affect manufacturing enterprises. Neoclassical analysis shows how macroeconomic variables might affect manufacturing businesses' decision-making and profitability

| [34] | Fakhry, B. (2016). A Literature Review of the Efficient Market Hypothesis. Turkish Economic Review. |

[34]

. The idea emphasises companies' flexibility to changing economic conditions and reasonable profit-maximization techniques. In this study, neoclassical theory is used to analyse macroeconomic factors and manufacturing business profitability to understand complicated interconnections. Researchers can understand how manufacturing businesses react to inflation, interest rates, GDP growth, and currency rates by recognising rational decision-making, market efficiency, and investment plans.

2.2.2. International Trade Theory

Foreign exchange and comparative advantage theories are important for Ghanaian export-oriented manufacturers

| [35] | Makoni, P. L. (2015). An extensive exploration of theories of foreign direct investment. Risk Governance and Control: Financial Markets and Institutions, 5(2CONT1), 77–84. https://doi.org/10.22495/rgcv5i2c1art1 |

[35]

. These ideas show how exchange rate variations affect export items' competitiveness and enterprises' international profitability. David Ricardo's comparative advantage theory says that states should specialise in providing commodities and services with a lower opportunity cost

. This hypothesis suggests that Ghanaian manufacturers should produce and export items in which they are efficient or advantaged. Abundant natural resources, skilled labour, or technology. Exchange rate variations can influence the cost structure of goods, influencing their overseas market competitiveness. Ghanaian exports may become more affordable with a lower local currency, increasing demand and profitability

. Policymakers and stakeholders need to understand international trade theories and exchange rate dynamics. Manufacturing enterprises may plan export strategy and maintain profitability with a stable exchange rate regime. Promotion of export-oriented sectors, productivity, and competitiveness can help enterprises navigate exchange rate changes. International trade theories can help Ghanaian manufacturers use exchange rate swings to boost export competitiveness and profitability. Understand comparative advantage and currency rate dynamics to make smart decisions to traverse the global market and increase exports sustainably.

2.2.3. Profit Maximization Theory

Firms want to maximise profits

| [38] | Alshebami, A. S. (2021). Evaluating the relevance of green banking practices on Saudi Banks’ green image: The mediating effect of employees’ green behaviour. Journal of Banking Regulation, 22(4), 275–286. https://doi.org/10.1057/s41261-021-00150-8 |

[38]

. Profit maximisation theory states that enterprises optimise production, pricing, and cost management to maximise profits

| [39] | Oduro, S. (2019). Impact of Innovation Types on SMEs’ Performance in the Cape Coast Metropolis of Ghana. Journal of Entrepreneurship and Innovation in Emerging Economies, 5(2), 110–127. https://doi.org/10.1177/2393957519857251 |

[39]

. Understanding how macroeconomic variables affect profitability supports this idea. Effective production, pricing, and cost management are the foundation of profit maximisation theory, which guides corporate behaviour and decision-making. The approach emphasises enterprises' main goal: sustained financial advantages that boost viability and expansion

| [40] | Safitri, J., Fuady, M., Wahyudi, S., Mawardi, W., & Utomo, M. N. (2020). The influence of dividend policy, investment opportunity and capital adequacy to firm value: Evidence in Indonesia banking companies. International Journal of Scientific and Technology Research. |

[40]

. Profit maximisation theory provides useful insights into how macroeconomic factors affect profitability. Production optimisation is key to manufacturing profit maximisation. Companies optimise resource allocation to meet customer demand at low cost

| [41] | Agyemang, E. B. (2013). Determinants of Dividend Payout Policy of listed Financial Institutions in Ghana. Research Journal of Finance and Accounting, 4(7), 2222–2847. https://doi.org/10.2298/PAN1306725N |

[41]

. Macroeconomic variables like inflation and currency rates affect production costs. For instance, high inflation raises raw material and labour prices, lowering manufacturing profits

| [42] | Hashim, S. L., Ramlan, H. & Rosly, M. A. M. (2018). The Impact of Macroeconomic Variables towards Malaysian Stock Market. Global Business and Management Research: An International Journal. |

[42]

. Firms can modify production techniques to preserve or increase profitability by recognising and responding to such factors. Pricing is crucial to profit maximisation. To maximise profit margins, firms balance customer willingness to pay with cost coverage

| [43] | Boateng, K., & Nagaraju, Y. (2020). The impact of digital banking on the profitability of deposit money banks: Evidence from Ghana. International Journal of Research in Finance and Managemen, 3(1), 144–150. https://www.researchgate.net/publication/342551616 |

[43]

. Interest rates effect borrowing costs, altering a firm's cost structure and price. Higher interest rates may increase borrowing costs, which can raise pricing. To maximise profits, firms must evaluate how these characteristics affect pricing strategies

| [2] | Prempeh, K. B., Sekyere, A. M., & Addy, E. K. A. (2018). A Multivariate Analysis of Determinants of Profitability: Evidence from Selected Manufacturing Companies Listed on the Ghana Stock Exchange. Journal of Accounting, Business and Finance Research, 2(1), 26–33. https://doi.org/10.20448/2002.21.26.33 |

[2]

. Profit maximisation theory affects marketing, operations, finance, and investment strategy

| [44] | Mwenda, B., Ngollo, M., Mwasota, A. (2023). An Empirical Studyof the Effect of Managerial Competenceon Firm Profitability. Ilomata International Journal of Tax and Accounting, 4(3), 491-507. https://doi.org/10.52728/ijtc.v4i3.794 |

[44]

. Firms must proactively analyse macroeconomic factors' effects on their operations and use this knowledge into their decision-making

| [38] | Alshebami, A. S. (2021). Evaluating the relevance of green banking practices on Saudi Banks’ green image: The mediating effect of employees’ green behaviour. Journal of Banking Regulation, 22(4), 275–286. https://doi.org/10.1057/s41261-021-00150-8 |

[38]

. Profit maximisation theory matches the study of how macroeconomic factors affect industrial profitability

| [43] | Boateng, K., & Nagaraju, Y. (2020). The impact of digital banking on the profitability of deposit money banks: Evidence from Ghana. International Journal of Research in Finance and Managemen, 3(1), 144–150. https://www.researchgate.net/publication/342551616 |

[43]

. Manufacturing enterprises may make smart judgements to flourish in a fast-changing economy by understanding macroeconomic dynamics and profit optimisation. Profit maximisation drives businesses' attempts to achieve sustained and resilient financial success.

2.3. Empirical Literature Review

The study of

| [11] | Ivković, D. (2021). Influence of Firm-Specific Determinants on the Profitability of Companies in Agri-Food Sector in Bosnia and Herzegovina: Research Project. Open Journal for Research in Economics, 4(1), 31–38. https://doi.org/10.32591/coas.ojre.0401.04031i |

[11]

shows how firm-specific variables affect the profitability of agricultural and food processing enterprises in Bosnia and Herzegovina

. It looked at how size, age, liquidity, leverage, and growth affected agri-food ROA. Financial reports of public firms for the financial year 2015 to 2019 were analysed. A model containing size, age, liquidity, leverage, and growth as independent factors and profitability as the dependent variable was created. The research seeks to identify significant characteristics affecting Bosnia and Herzegovina agri-food enterprises' profitability, guiding management choices and laying the groundwork for future studies with more variables.

They

explored how micro and macro variables affect company performance in Vietnam's transition from subsidised to market economy

| [45] | Kim, D.-G., E. Grieco, A. Bombelli, J. E. Hickman, and A. Sanz-Cobena, 2021: Challenges and opportunities for enhancing food security and greenhouse gas mitigation in smallholder farming in sub-Saharan Africa. A review. Food Security, 13, no. 2, 457-476, https://doi.org/10.1007/s12571-021-01149-9 |

[45]

. STATA was used to study 30 listed food processors from the year 2014 to 2019. For more insight, Blinder-Oaxaca decomposition analysis is used. The results show that total assets turnover ratio (ATR) and sales growth significantly affect financial performance, evaluated by ROE or ROS. Leverage hurts ROI. State-owned businesses (SOEs) and non-SOEs have different financial performance and predictive impacts due to different factors. This research illuminates Vietnam's distinctive economy.

The study looked at how interest rates affected Nigerian manufacturing enterprises' financial performance for the year 2009-2018

. With interest rate (ITR) as the independent variable, the study explored ROA and ROE as dependent variables. Annual reports from 28 manufacturing enterprises and Central Bank of Nigeria records were used. The study used cross-sectional/time series data and panel multiple regression in Eviews-10 to find that interest rates significantly affected ROA but not ROE for listed Nigerian manufacturing enterprises. Setting borrowing rates that don't hurt these companies' finances is advised.

The researchers examined how macroeconomic variables affected Nigeria's healthcare sector's financial performance

| [10] | Ifeyinwa, E., Nwabuisi, O., & Igwe, O. (2021). Effect of o Macr roecono omic Variable es on F inancia al Pe erforma ance of f Health hcare Manufac cturing g Firms in Nigeria a. |

[10]

. Ex-post facto research design, descriptive statistics, completely modified panel regression, and Pearson correlation analysis are used to analyse yearly reports and financial statements. Results show that macroeconomic variables greatly impact Nigerian healthcare manufacturing enterprises' finances. Inflation, currency rate, interest rate, foreign debt, and trade openness have major implications. The findings show economic volatility hurts healthcare manufacturers. Nigerian sector performance may be enhanced by controlling currency rates, managing interest rates, and lowering borrowing and trade openness.

From the Indonesian context, researchers examined dividend policy, employee share distribution programmes, and debt-to-equity ratio in Indonesia Stock Exchange (IDX) industrial enterprises from the year 2013 to 2017,

| [46] | Ichsan, I., Silvia, I., Mahdawi, M., & Syamni, G. (2021). the Financial Performance of Manufacturing Companies in Idx and Some Factors That Influence. Jurnal Aplikasi Manajemen, 19(2), 354–362. https://doi.org/10.21776/ub.jam.2021.019.02.11 |

[46]

. A panel regression model comprising common effect, fixed effect, and random effect models was used to analyse 20 firms' financial statements. Best fit was the fixed effect model. Results show that dividend policy, employee share programmes, and debt-to-equity ratio affect financial success. The debt-to-equity ratio has the largest impact, whereas investment decisions have less.

They examined how macroeconomic and firm-specific factors affected corporate profitability in Singapore and Hong Kong before, during, and after the global financial crisis

| [6] | Cheong, C., & Hoang, H. V. (2021). Macroeconomic factors or firm-specific factors? An examination of the impact on corporate profitability before, during and after the global financial crisis. Cogent Economics and Finance, 9(1), 1–24. https://doi.org/10.1080/23322039.2021.1959703 |

[6]

. The two-step Generalised Method of Moments is used to analyse how these factors affect company profitability (ROA, ROE, and Tobin's Q). The model considers macroeconomic parameters like real GDP growth and inflation rate as well as firm-specific elements like size, leverage, liquidity, sales growth, and profitability. Results show that prior profitability, business size, and leverage greatly affect firm success. Hong Kong enterprises were more vulnerable to macroeconomic issues than Singapore firms during the global financial crisis. The study examines how firm-specific and macroeconomic variables affect firm performance in developed Asia-Pacific countries across time.

The

macroeconomic indices, working capital flows, and financial performance in emerging economies were examined by

| [47] | Hussain, S., Nguyen, V. C., Nguyen, Q. M., Nguyen, H. T., & Nguyen, T. T. (2021). Macroeconomic factors, working capital management, and firm performance—A static and dynamic panel analysis. Humanities and Social Sciences Communications, 8(1). https://doi.org/10.1057/s41599-021-00778-x |

[47]

. The study examines working capital components, gross profit, and cash conversion period using static and dynamic panel analysis. When interest rates are interacted with average payable days, higher interest rates hurt business performance. The study also shows a positive association between average payment term and business performance, contrary to expectations. Cash conversion cycle initially hurts financial performance, but interest rates modify this. Exchange rate changes affect the cash conversion cycle's impact on corporate performance. This study reveals how exchange rates and interest rates affect corporate performance.

Examining how firm-specific and macroeconomic variables affected financial distress risk, the data from Borsa Istanbul SMEs Industrial Index businesses were explored from the year 2010 to 2019

| [48] | Ceylan, I. E. (2021). The impact of firm-specific and macroeconomic factors on financial distress risk: A case study from Turkey. Universal Journal of Accounting and Finance, 9(3), 506–517. https://doi.org/10.13189/ujaf.2021.090325 |

[48]

. The research used the Generalised Method of Moments (GMM) estimator to evaluate how numerous factors may affect financial distress risk, quantified by the Springate S score. We use firm-specific metrics (current ratio, quick ratio, asset turnover, debt ratio, financial leverage, and return on assets) and macroeconomic parameters (economic growth, exchange rate, and inflation rate). Research shows that firm-specific ratios increase distress risk whereas consumer price index changes decrease it. This study analyses Turkish SMEs' financial distress risk using micro and macro parameters and has practical consequences for SME executives. The researchers in sub-Saharan Africa examined how economic conditions affect Nigerian consumer products manufacturers' finances

| [49] | Egbe, I. S., Onuora, U. R., Iteh, A. A., & Onyeanu, E. O. (2021). Effect of economic variables on the financial performance of listed firms manufacturing consumers goods in nigeria. Universal Journal of Accounting and Finance, 9(6), 1235–1246. https://doi.org/10.13189/ujaf.2021.090603 |

[49]

. The study employs an ex-post facto research approach using Ordinary Least Square multiple regression analysis to examine 13 of 20 listed consumer goods corporations' 17-year financial data. Interest rates, currency rates, CPI, and net asset per share are correlated. CPI greatly impacts NAPS, but ARDL coefficients reveal short-term correlations. Exchange and interest rates barely affect NAPS. The data suggest inflation impacts consumer prices, enterprises alter profit margins, and rising interest and currency rates lower NAPS. Business incentives and domestic product promotion are suggested.

In their study,

discovered Dhaka Stock Exchange manufacturing company’s profitability factors. Pearson's correlation and ordinary least squares regression models were employed on the data from the year 2014-2019. The study found that management efficiency, sales growth, and capital intensity boost profitability, but liquidity and leverage lower it. Profitability is unaffected by business size, working capital, yearly inflation, and GDP growth. The study stresses the relevance of these drivers in manufacturing company investment decisions. Theoretical and empirical portions explore factors and survey data from 34 DSE-listed manufacturing businesses, presenting policy implications and investor advice.

They examined corporate profitability in Indonesian manufacturing, particularly consumer products businesses listed on the Indonesia Stock Exchange

| [51] | Susan, M., Winarto, J., & Gunawan, I. (2022). The Determinants of Corporate Profitability in Indonesia Manufacturing Industry. Review of Integrative Business and Economics Research, 11(1), 184. |

[51]

. Internal factors like business size and external factors like interest rates affected profitability. Finding profitability predictors is the research's verification strategy. The results show that business size and interest rate affect profitability. The study's findings might help Indonesian manufacturing organisations identify and prioritise their company profitability aspects to make better strategic decisions.

The financial data for the year 2012-2021 was used by

| [5] | Agegnew, A., & Gujral, T. (2022). Determinants Of Profitability: Evidence From Selected Manufacturing Company In Hawassa, Ethiopia. Journal of Positive School Psychology, 2022(6), 8309–8322. http://journalppw.com |

[5]

to study manufacturing company profitability. The study examines 10 Hawassa manufacturing enterprises with 100 observations using an explanatory research methodology and random panel model regression analysis. According to panel regression research, business size, growth, and fixed asset ratio positively and substantially effect profitability, while liquidity, leverage, and operational cost negatively and significantly affect profitability. Operating cost is important for stakeholders, according to the research. Although confined to the setting, the data can help manufacturing executives make strategic decisions about firm-specific variables.

Autoregressive distributed lag was used to study whether macroeconomic and socio-economic/political factors affect Nigeria's manufacturing subsector

| [52] | Lawal, A. I., Oseni, E., Lawal-Adedoyin, B. B., IseOlorunkanmi, J., Asaleye, A. J., Inegbedion, H., Santanu, M., DickTonye, A., Olagunju, O., & Ogunwole, E. (2022). Impact of macroeconomic variables on the Nigerian manufacturing sector. Cogent Economics and Finance, 10(1). https://doi.org/10.1080/23322039.2022.2090664 |

[52]

. The study uses Solow growth theory and endogenous growth model and examined data from 1986 to 2019. Both hypotheses had short-term validity, but only the endogenous growth model lasted. To sustain economic development fueled by a strong manufacturing sector, macroeconomic variables and socio-political factors must be aligned, according to the research. Policymakers may use the study's findings to boost economic growth.

From the South African perspective,

| [53] | Ajeigbe, K. B., Thomas, H., & Fortune, G. (2022). The impact of the selected macroeconomic indicators’ volatility on the performance of South African JSE-listed companies: a pre-and post- Covid-19 study. International Journal of Research in Business and Social Science (2147- 4478), 11(4), 193–204. https://doi.org/10.20525/ijrbs.v11i4.1805 |

[53]

examined how macroeconomic variables including inflation, economic growth, exchange rate, and share price affect South African listed enterprises. The research assessed the short- and long-term effects of macroeconomic volatility on corporate performance, taking into account the current pandemic, using panel Autoregressive Distributed Lag (ARDL) modelling on yearly data from 2010 to 2020 and the results show that economic growth, exchange rate, and share price positively affect asset returns, with long-term stock returns affected by both. Short-term effects are minor. The study suggests promoting economic development and currency rate stability for corporate performance and evaluating internal elements for short-term performance.

The study examined how macroeconomic circumstances and financial performance affected dividend policy in IDX-listed manufacturing businesses throughout the pandemic

| [54] | Rinanda, Y. (2022). The Influence of Macroeconomic Factors and Financial Performance on Dividend Policy During Pandemic (Manufacturing Company Listed on the IDX). Dinasti International Journal of Economics, Finance & Accounting, 2(6), 637–646. https://doi.org/10.38035/dijefa.v2i6.1300 |

[54]

. The study analysed how inflation, interest rates, and the currency rate affect dividend policy, along with profitability, capital, and liquidity ratios. Indonesia Stock Exchange-listed manufacturing enterprises are the study's population. Multiple regression was done with EVIEWS. Results show that inflation and interest rates do not impact dividend policy very much. Financial performance variables like ROA, ROE, and EPS affect manufacturing businesses' dividend policy.

They examined relevant elements that explain profitability research discrepancies

| [4] | Wijaya, L. I., Harjono, J. A., & Mahadwartha, P. A. (2022). Determinants of Profitability for Manufacturing Companies in Indonesia 2018-2020. Jurnal Riset Akuntansi Dan Keuangan, 10(2), 189–198. https://doi.org/10.17509/jrak.v10i2.45199 |

[4]

. It analysed internal and external profitability variables for Indonesia Stock Exchange-listed manufacturing businesses from 2018-2020. Multiple linear regression is used using profitability as the dependent variable and business size, age, liquidity, capital structure, growth, capital intensity, and macroeconomic indicators as independent variables using secondary data and quantitative approaches. The analysis of 789 observations from 263 enterprises over three years found that firm size, age, liquidity, growth, capital intensity, and macroeconomic factors boost profitability. However, capital structure hurts profitability significantly.

In attempt to answer inconclusive worldwide research

, [8] examined macroeconomic indicators on 21 DSE enterprises from 2006 to 2021. A mixed-sequential explanatory study design used DSE secondary panel data and semi-structured interview qualitative data. Data analysis used random effect and theme analysis. GDP, inflation, and money supply boost company performance, but interest rates and exchange rates hurt it. The study's unique blend of qualitative and quantitative data helps explain how macroeconomic factors affect Tanzanian listed business performance. Considering proactive management of these factors for competitiveness and sustainability, corporate profitability variables were identified

. Financial accounts of Indonesia Stock Exchange-listed manufacturing enterprises from 2015 to 2019 are examined. We employed non-probability purposive sampling. Descriptive statistical analysis, capital estimates, classical assumption tests, and hypothesis testing were used. Firm Size, Leverage, Liquidity, and Sales Growth do not effect profitability, but Working Capital and Company Efficiency do.

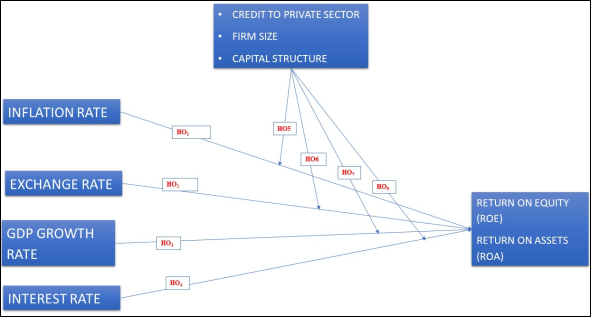

2.4. Conceptual Framework and Hypothesis Formulation

2.4.1. Conceptual Framework

This study shows how chosen macroeconomic variables affect Ghanaian listed manufacturing enterprises' profitability. Changes in macroeconomic circumstances can affect manufacturing enterprises' financial performance, according to the framework. Inflation, exchange rates, GDP growth, and interest rates are chosen macroeconomic variables. Net profit margin, ROE, and ROA were used to evaluate manufacturing enterprises' financial performance. Conceptual framework shows hypothesised variable directionality. This study hypothesised that increasing inflation and interest rates raise manufacturing firm production and borrowing costs, lowering profitability. However, a developing economy and favourable exchange rates can raise demand for manufactured goods and export profits, which should boost profitability.

Figure 1. Conceptual Framework and Hypothesis Formulation of the study variables.

2.4.2. Hypothesis Formulation

Based on the conceptual framework, the following hypotheses are formulated:

H01: There is no significant relationship between inflation and the profitability of listed manufacturing firms in Ghana.

H02: There is no significant relationship between exchange rates and the profitability of listed manufacturing firms in Ghana.

H03: There is no significant relationship between GDP growth rates and the profitability of listed manufacturing firms in Ghana.

H04: There is no significant relationship between interest rates and the profitability of listed manufacturing firms in Ghana.

H05: There is no moderating effect of credit to the private sector on the relationship between interest rate and profitability in the manufacturing sector in Ghana.

H06: Firm size does not moderate the relationship between inflation and profitability in the manufacturing sector in Ghana.

H07: Capital structure does not moderate the relationship between exchange rate and profitability in the manufacturing sector in Ghana.

H08: Capital structure does not moderate the relationship between GDP growth and profitability in the manufacturing sector in Ghana.

3. Data and Methodology

In this section, the study design, study area, the sample procedures, the procedure for data collection and the analytical technique used to analyze the data are discussed. The research methodology focused on the procedures for data collection and analysis that clarify the selected design, variable description and provides the model specification for the study.

3.1. Research Philosophies

Research philosophies underpin a study's approach, technique, and perspective

. Interpretivist and Positivist are popular research philosophies. Positivism studies observable and measurable events objectively

| [56] | Maarouf, H. (2019). Pragmatism as a Supportive Paradigm for the Mixed Research Approach: Conceptualizing the Ontological, Epistemological, and Axiological Stances of Pragmatism. International Business Research. https://doi.org/10.5539/ibr.v12n9p1 |

[56]

. Positive thinking uses empirical observation and data analysis to find generalizable patterns and causal links. Positivist research emphasises objectivity, quantification, and science. Positivists believe in a single reality that can be investigated methodically

| [57] | Saunders, M., Lewis, P., & Thornhill, A. (2016). Research methods for business students (Vol. Seventh). Harlow: Pearson Education. |

[57]

. Interpretivist, on the other hand, seeks to comprehend and interpret individual meanings and subjective experiences

. Positivism encourages structured and systematic research, which is useful for studying a certain collection of variables and their relationships. A positivist research philosophy fits the study's purpose, methods, and empirical nature

| [59] | Cruickshank, J. (2011). The positive and the negative: Assessing critical realism and social constructionism as post-positivist approaches to empirical research in the social sciences. In IMI Working Papers Series. |

[59]

. Positivism is suitable for studying the relationships between financial performance variables and macroeconomic indicators in listed manufacturing firms in Ghana due to its focus on objective analysis, quantification, causal relationships, generalizability, hypotheses testing, data-driven insights, and a structured approach.

3.2. Research Designs

Exploratory, descriptive, and explanatory research designs examine links and phenomena differently

. To explore the relationship between macroeconomic variables and the financial performance of listed manufacturing firms in Ghana, an explanatory research methodology is advised for hypothesis testing and causal relationships. The best research design for this topic is explanatory. In order to establish the links between macroeconomic variables and financial performance indicators with more certainty, this architecture permits hypothesis testing. The study can rigorously examine the hypothesised correlations and identify the causal links that drive profitability indicators by gathering quantitative data on these factors and using statistical analyses. The explanatory research design's capacity to demonstrate causal links illuminates Ghanaian manufacturing enterprises' financial performance. Researchers can account for confounding factors in the explanatory design to ascribe observed effects to the macroeconomic variables under study. Explanatory research designs are well-suited to address research questions and achieve study objectives by providing a structured and systematic approach to analysing the complex relationships between macroeconomic variables and financial performance indicators in Ghana's manufacturing sector. This study used secondary sources including Ghana Stock Exchange (GSE) manufacturing business financial reports and government publications. Bank of Ghana and World Bank development indicators provided macroeconomic data such inflation, exchange, GDP growth, and interest rates. Listed manufacturing enterprises' annual reports, financial statements, and disclosures on the Ghana Stock Exchange's website or their own websites provided financial data. Profitability metrics like net profit margin, ROE, and ROA are included for a certain period. Inflation, exchange, GDP growth, and interest rates were acquired from reliable economic databases and government sources. Data was collected at the same time as manufacturing business financials. These variables are used to analyse data and examine the association between macroeconomic variables and Ghanaian listed manufacturing enterprises' profitability.

3.3. Data-set

This study uses quantitative research. The method collects and analyses numerical data to determine how macroeconomic variables affect Ghanaian listed manufacturing enterprises' profitability. Quantitative methods can test hypotheses and objectively assess variable connections. Secondary data was used for this investigation. Financial data from listed manufacturing enterprises' annual reports, financial statements, and disclosures on the Ghana Stock Exchange's website or their official websites was obtained. Inflation, exchange, GDP growth, and interest rates were obtained from reliable economic databases and official publications from the Ghana Statistical Service and Central Bank of Ghana. The study examined Ghana Stock Exchange-listed manufacturing enterprises. Availability of financial data and manufacturing relevance determined business selection. To apply the findings to all listed manufacturing enterprises in Ghana, a representative sample was selected. The macroeconomic variables (inflation, exchange rates, GDP growth rates, and interest rates) and manufacturing firm financial performance indicators (net profit margin, return on equity, and return on assets) are of interest. Data is rigorously quantified. Manufacturing business financial performance and macroeconomic variables were summarised using descriptive statistics. Variable associations were examined using correlation analysis. Multiple regression analysis was used to examine how macroeconomic variables affect manufacturing business profitability while controlling for other factors. Long-term data trends and patterns can be examined using time-series analysis.

3.4. Variables Description and Measurement

This section provides a detailed description of the key variables used in the study and how they were measured. The variables under consideration are related to the financial performance of listed manufacturing firms and the selected macroeconomic indicators in Ghana.

Table 1. Variables Description and Measurement.

Variables | Definition | Formula | Source |

Financial Performance Variables |

Return on Equity (ROE) | A financial ratio indicating the profitability of equity investments, measured as the percentage of net income earned on shareholders' equity. | ROE = (Net Income / Shareholders' Equity) * 100 | Financial Statements of listed manufacturing firms (GSE) |

Return on Assets (ROA) | A financial metric assessing a firm's efficiency in using assets to generate profits, measured as the percentage of net income earned on total assets. | ROA = (Net Income / Total Assets) * 100 | Annual Reports of listed manufacturing firms (GSE) |

Macroeconomic Variables | |

Inflation Rate | A macroeconomic indicator measuring the percentage change in the Consumer Price Index (CPI) over a specific period. | Percentage (%) | Ghana Statistical Service; Central Bank of Ghana |

Exchange Rate | The value of the local currency relative to a foreign currency, indicating the price at which one currency can be exchanged for another. | Ratio (e.g., 1 USD = X GHS) | Ghana Statistical Service; Central Bank of Ghana |

GDP Growth Rate | A macroeconomic indicator measuring the percentage change in the Gross Domestic Product (GDP) of the country over a specific period. | Percentage (%) | Ghana Statistical Service; Central Bank of Ghana |

Interest Rate | A macroeconomic variable representing the cost of borrowing or return on savings, influencing firms' cost of capital and investment decisions. | Percentage (%) | Ghana Statistical Service; Central Bank of Ghana |

Moderating variables |

Credit to private sector | Volume of credit extended to the private sector | Amount of Credit from banks to private sector | Ghana Statistical Service; Central Bank of Ghana |

Firm size | Measure of the company's scale or revenue | Log of Total Revenue or Assets | Annual Reports of listed manufacturing firms (GSE) |

Capital structure | Composition of a company's financial resources | Debt-to-Equity Ratio | Annual Reports of listed manufacturing firms (GSE) |

Source: Author’s Construct

3.5. Model Specification

The model specification describes the statistical model used to analyse the link between macroeconomic variables and listed manufacturing firm profitability in Ghana. This study examined how macroeconomic variables affect manufacturing firm financial performance indicators using multiple regression analysis. The general form of the multiple regression model can be represented as follows:

Where:

ROE AND ROA= Profitability Indicator represents the financial performance metric of the manufacturing firm, such as net profit margin, return on equity (ROE), or return on assets (ROA).

INF= Inflation is the inflation rate, representing the percentage change in the Consumer Price Index over a specific period.

EXR= Exchange Rate is the value of the local currency against a foreign currency.

GDP= GDP Growth Rate represents the percentage change in the Gross Domestic Product over a specific period.

INT= Interest Rate is the cost of borrowing or return on savings.

β0, β1, β2, β3, β4, β5, β6, β7, and β8 are the regression coefficients, representing the relationship between each macroeconomic variable and the profitability indicator.

ε is the error term, representing the random variability or unexplained factors affecting the profitability indicator.

4. Results and Discussion

4.1. Summary Statistics

Table 1 displays summary data for the variables examined in this study. ROE measures a company's profitability in relation to its shareholder equity. The mean ROE is 24.830, with a median of 19.803, demonstrating considerable variation in entity profitability. The maximum ROE is 463.575, indicating extreme outliers, possibly due to manufacturing enterprises' exceptional financial success. The minimum ROE of -255.022 represents negative returns, which could imply financial trouble or poor performance. Return on Assets (ROA) is another financial metric for a company's asset profitability. Divide net income by total assets to calculate ROA. The dataset's mean ROA is 15.1241, while the median is 13.947. The greatest ROA is 56.961, indicating a considerable range in asset profitability across enterprises. The minimum ROA of -44.2878 indicates negative returns relative to total assets, indicating financial challenges for some businesses. Total assets, market capitalization, and revenue are used to determine a company's size. The dataset's mean SIZE is 8.404, which represents the typical size of these things. The low standard deviation of 0.621 indicates that firm sizes are grouped. Understanding SIZE is required when assessing an entity's economic footprint and market presence. The interest rate (INTER) is the cost of borrowing or return on investment offered to lenders. The mean INTER is 12.2166, which represents the average interest rate among companies. Lower interest rates may be more common due to the slightly left-skewed distribution of -0.2114. The INTER variable is critical for understanding the entities' financial environment, as it influences their cost of capital and financial decision-making. Inflation (INF) reduces purchasing power by increasing prices. In the dataset, the mean INF is 13.762, while the median is 11.666. The distribution has a positive skewness of 1.6381, indicating that greater inflation rates are more likely. Inflation influences consumer behaviour, investment decisions, and economic stability, thus understanding it is critical.

GDP is an important economic indicator since it measures the percentage change in a country's total goods and services over time. The dataset's GDP average is 4.9911, indicating economic expansion. The dataset's high kurtosis of 5.1722 indicates large tails and rapid GDP growth. GDP is critical for evaluating the observed entities' economic performance and direction. The exchange rate (EXR) of currencies is critical for international traders. The dataset's mean EXR is 4.3776, and the median is 4.3505. Lower exchange rates are most likely owing to the slightly right-skewed distribution of 0.4957. Exchange rate variations have a global impact on corporate competitiveness and financial performance. The private sector credit (DCPS) of domestic financial institutions is measured. The dataset's mean DCPS is 15.2124. The distribution's 0.0489 positive skewness indicates a slight right tail. Credit availability for private-sector enterprises influences investment, business expansion, and economic activity, hence DCPS monitoring is critical. These variables reveal the observed entities' financial performance, economic environment, and market dynamics. Understanding each variable's impact is critical for making financial, investment, and economic policy decisions.

Table 2. Summary Statistics of the Variables employed.

| ROE | ROA | SIZE | INTER | INF | GDP | EXR | DCPS |

Mean | 24.830 | 15.1241 | 8.404 | 12.2166 | 13.762 | 4.9911 | 4.3776 | 15.2124 |

Median | 19.803 | 13.947 | 8.474 | 2.0833 | 11.666 | 5.3564 | 4.3505 | 15.2923 |

Maximum | 463.575 | 56.961 | 10.862 | 14.0625 | 31.255 | 9.2927 | 8.2724 | 18.0717 |

Minimum | -255.022 | -44.2878 | 7.584 | 10.0500 | 7.1436 | 0.5139 | 1.8248 | 12.1615 |

Std. Dev. | 78.206 | 18.5771 | 0.621 | 1.05927 | 6.4958 | 2.6555 | 1.7886 | 2.0446 |

Skewness | 2.347 | 0.1013 | 1.967 | -0.2114 | 1.6381 | -0.0221 | 0.4957 | 0.0489 |

Kurtosis | 21.966 | 4.1371 | 9.1345 | 2.7499 | 5.1722 | 1.8633 | 2.9249 | 1.5336 |

Jarque-Bera | 874.914 | 3.0573 | 121.742 | 0.5529 | 35.413 | 2.9653 | 2.2660 | 4.9492 |

Probability | 0.000 | 0.216 | 0.000 | 0.7584 | 0.0000 | 0.2270 | 0.3220 | 0.0841 |

Sum | 1365.66 | 831.830 | 462.255 | 671.914 | 756.926 | 274.513 | 240.771 | 836.682 |

Sum Sq. Dev. | 330279.0 | 18636.00 | 20.867 | 60.591 | 2278.60 | 380.801 | 172.760 | 225.762 |

Observations | 55 | 55 | 55 | 55 | 55 | 55 | 55 | 55 |

Source: Research Output

4.2. Correlation of Study Variables

Table 3 shows how the study variables relate to Return on Equity (ROE) and Return on Assets (ROA). The statistical significance of each correlation coefficient is indicated by its p-value. A correlation coefficient of 0.501 (p-value < 0.001) indicates a positive correlation between ROA and ROE. This positive correlation suggests that companies with higher ROE also have higher ROA, indicating consistent profitability. SIZE is negatively correlated with ROA (-0.325, p-value = 0.015), suggesting that smaller entities may have higher ROA. SIZE, which measures operations, may affect asset profitability. Interest Rate (INTER), Inflation (INF), GDP, Exchange Rate (EXR), and Domestic Credit to Private Sector (DCPS) have weak correlations with ROA (-0.093 to 0.154). These correlations suggest macroeconomic factors have little direct effect on asset returns.

ROE is positively correlated with ROA (0.501, p-value < 0.001), indicating that entities with higher ROA tend to have higher ROE. This positive correlation highlights profitability alignment. SIZE positively correlates with ROE (0.337, p-value = 0.011), suggesting that larger companies may have higher ROE. The relationship suggests that operations scale may boost shareholder profitability. INTER and INF have weak correlations with ROE (0.0512 and 0.0806, respectively). Correlations suggest interest rates and inflation have little direct effect on return on equity. GDP and EXR have weak correlations with ROE (0.143 and -0.224, respectively). Results suggest economic growth and exchange rate fluctuations have a modest effect on return on equity. Although not statistically significant, Domestic Credit to Private Sector (DCPS) has a positive correlation with ROE (0.117, p-value = 0.391), suggesting a relationship between credit availability and return on equity. The correlation analysis illuminates financial and macroeconomic variables' effects on ROE and ROA. The positive correlation between ROE and ROA emphasises profitability consistency. Entity size affects ROE and ROA, and macroeconomic factors have little direct impact, highlighting the complexity of financial performance factors.

Table 3. Correlation matrix of the variables.

| ROE | ROA | SIZE | INTER | INF | GDP | EXR | DCPS |

ROE | 1.000 | | | | | | | |

ROA | 0.501 | 1.000 | | | | | | |

| (0.000) | ----- | | | | | | |

SIZE | 0.337 | -0.325 | 1.000 | | | | | |

| (0.011) | (0.015) | ----- | | | | | |

INTER | 0.0512 | -0.0930 | -0.140 | 1.000 | | | | |

| (0.710) | (0.499) | (0.305) | ----- | | | | |

INF | 0.0806 | 0.154 | 0.051 | 0.254 | 1.000 | | | |

| (0.558) | (0.260) | (0.709) | (0.060) | ----- | | | |

GDP | 0.143 | 0.132 | 0.062 | -0.238 | -0.384 | 1.000 | | |

| (0.294) | (0.336) | (0.651) | (0.079) | (0.003) | ----- | | |

EXR | -0.224 | -0.078 | 0.127 | -0.007 | 0.448 | -0.410 | 1.000 | |

| (0.100) | (0.566) | (0.354) | (0.956) | (0.000) | (0.001) | ----- | |

DCPS | 0.117 | 0.080 | -0.170 | 0.251 | -0.061 | 0.197 | -0.788 | 1.000 |

| (0.391) | (0.561) | (0.213) | (0.064) | (0.653) | (0.148) | (0.000) | ----- |

Source: Research Output

4.3. Unit Root Test Results (ADF)

The Augmented Dickey-Fuller (ADF) unit root test results, presented in the

table 4, assess the stationarity of the study variables at both the level and first difference. Time series analysis relies on the unit root test to determine whether a variable is stationary after differencing or non-stationary. Return on Equity (ROE) has an ADF test statistic of 0.1907 at the level, indicating non-stationarity, and 0.0603 with the first difference, indicating stationarity at 1%. Return on Assets (ROA) also achieves stationarity at 1% significance with a test statistic that decreases from 0.0927 to 0.1512 with the first difference. The firm size (SIZE) variable has a test statistic of 0.6971, indicating non-stationarity, but the first difference makes it stationary at 5%. Time series analyses should account for first differences in variables like Interest Rate (INTER) and GDP, which reach stationarity only after differencing. The unit root test also emphasises Schwartz Information Criterion-based lag length determination. One, two, or three asterisks indicate 10%, 5%, and 1% significance levels, respectively. The ADF results reveal the study variables' stationarity properties, which are essential for building reliable time series models.

Table 4. Unit Root Test Results (ADF).

| At Level | At First Difference |

| With Constant | With Constant & Trend | Without Constant & Trend | With Constant | With Constant & Trend | Without Constant & Trend |

| t-Statistic | t-Statistic | t-Statistic | t-Statistic | t-Statistic | t-Statistic |

ROE | 0.1907 | 0.3444 | 0.0205** | 0.0603*** | 0.1907** | 0.0041*** |

ROA | 0.0927 | 0.3592 | 0.0189*** | 0.1512*** | 0.4259** | 0.0155*** |

SIZE | 0.6971 | 0.0929 | 0.9998 | 0.3365 | 0.7097** | 0.0044** |

INTER | 0.0958* | 0.1009 | 0.7729 | 0.0389** | 0.2326 | 0.0020*** |

INF | 0.7196 | 0.9665 | 0.8167 | 0.8434 | 0.9740 | 0.0018*** |

GDP | 0.0801* | 0.2614 | 0.0906* | 0.0273** | 0.1050 | 0.0016*** |

EXR | 0.9892 | 0.5093 | 0.9976 | 0.2512 | 0.6486 | 0.0021*** |

DCPS | 0.7176 | 0.0548* | 0.1229 | 0.0424** | 0.1072 | 0.0038*** |

Notes: a: (*) Significant at the 10%; (**) Significant at the 5%; (***) Significant at the 1% and (no) Not Significant b: Lag Length based on SIC c: Probability based on | [61] | MacKinnon, J. G. (1996). Numerical Distribution Functions for Unit Root and Cointegration Tests. Journal of Applied Econometrics. Vol. 11, No. 6, pp. 601-618. JSTOR, J. Wiley & Sons Ltd. |

[61] |

Source: Research Output

4.4. Regression Results

The study employed pooled ordinary least squares to estimate the results for the study. These results are presented as follows;

Table 5. Regression results (ROA).

Variable | Coefficient | Prob. |

Direct effect | | |

SIZE | -20.33766 | 0.1104 |

INTER | -16.30661 | 0.6032 |

INF | -8.833198 | 0.6810 |

GDP | -1.133281 | 0.9486 |

EXR | 163.8617 | 0.0373 |

Moderating effect | | |

SIZEINTER | 5.512083 | 0.0124 |

SIZEINF | -2.359657 | 0.0884 |

SIZEGDP | -0.785558 | 0.6129 |

SIZEEXR | -8.261996 | 0.0198 |

DCPSINTER | -1.408293 | 0.4178 |

DCPSINF | 2.214825 | 0.0585 |

DCPSEXR | -6.663968 | 0.1586 |

DCPGDP | 0.867306 | 0.2006 |

R-squared | 0.430646 | |

Adjusted R-squared | 0.267973 | |

S.E. of regression | 15.89436 | |

Sum squared resid | 10610.49 | |

Log likelihood | -222.7539 | |

Durbin-Watson stat | 1.905048 | |

Mean dependent var | 15.12419 | |

S.D. dependent var | 18.57717 | |

Akaike info criterion | 8.572869 | |

Schwarz criterion | 9.047330 | |

Hannan-Quinn criter. | 8.756347 | |

Source: Research Output

Table 6. Regression results (ROE).

Variable | Coefficient | Prob. |

Direct effect | | |

SIZE | -68.48021 | 0.1439 |

INTER | -179.3048 | 0.1259 |

INF | -25.71529 | 0.7454 |

GDP | 79.84166 | 0.2225 |

EXR | 683.9614 | 0.0192 |

Moderating effect | | |

SIZEINTER | 35.58251 | 0.0000 |

SIZEINF | -6.246240 | 0.2174 |

SIZEGDP | -11.11472 | 0.0571 |

SIZEEXR | -55.61509 | 0.0001 |

DCPSINTER | -5.478666 | 0.3928 |

DCPSINF | 6.295273 | 0.1413 |

DCPSEXR | -16.97956 | 0.3270 |

DCPGDP | 1.790474 | 0.4706 |

R-squared | 0.563195 | |

Adjusted R-squared | 0.438393 | |

S.E. of regression | 58.60838 | |

Sum squared resid | 144267.6 | |

Log likelihood | -294.5241 | |

Durbin-Watson stat | 1.974814 | |

Mean dependent var | 24.83021 | |

S.D. dependent var | 78.20663 | |

Akaike info criterion | 11.18270 | |

Schwarz criterion | 11.65716 | |

Hannan-Quinn criter. | 11.36617 | |

Source: Research Output

4.5. Discussion of Results

4.5.1. The Influence of Exchange Rate Fluctuations on the Profitability of Listed Manufacturing Firms

Exchange rate fluctuations affect listed manufacturing firms' financial performance metrics, particularly ROE and ROA. The direct effect coefficient for exchange rate (EXR) is 163.8617 with a probability of 0.0373, indicating a statistically significant positive ROA effect. The results indicate that listed manufacturing firms' return on assets improves as exchange rates rise. The direct effect coefficient for exchange rate (EXR) is 683.9614 with a probability of 0.0192, indicating a statistically significant positive ROE impact. The results show that listed manufacturing firms' return on equity improves as exchange rates rise. Results indicate that exchange rate fluctuations affect listed manufacturing firms' financial performance in two ways. Higher exchange rates directly increase ROE and ROA, indicating that higher exchange rates increase profitability. The positive effect is dampened by firm size, revealing a more nuanced relationship. The findings emphasises the importance of considering exchange rate fluctuations' direct effects and their interaction with other firm-specific characteristics, particularly size, when assessing their impact on financial performance metrics. This information can help manufacturing firms manage their financial strategies in the face of changing exchange rates. The findings illuminate how exchange rate fluctuations affect manufacturing firm profitability.

| [47] | Hussain, S., Nguyen, V. C., Nguyen, Q. M., Nguyen, H. T., & Nguyen, T. T. (2021). Macroeconomic factors, working capital management, and firm performance—A static and dynamic panel analysis. Humanities and Social Sciences Communications, 8(1). https://doi.org/10.1057/s41599-021-00778-x |

[47]

Found that exchange rate fluctuations affect the cash conversion cycle's impact on firm performance, highlighting the complex relationship between macroeconomic variables and working capital dynamics.

| [45] | Kim, D.-G., E. Grieco, A. Bombelli, J. E. Hickman, and A. Sanz-Cobena, 2021: Challenges and opportunities for enhancing food security and greenhouse gas mitigation in smallholder farming in sub-Saharan Africa. A review. Food Security, 13, no. 2, 457-476, https://doi.org/10.1007/s12571-021-01149-9 |

[45]

Examined Vietnam's transitioning economy and found that total assets turnover ratio, sales growth, and leverage negatively affected financial performance and return on sales. The study shows that exchange rate fluctuations affect manufacturing firms in many ways, affecting financial performance metrics and strategic decision-making.

4.5.2. The Relationship between GDP Growth Rates and the Financial Performance of Listed Manufacturing Firms

The results show how GDP growth rates affect listed manufacturing firms' ROE and ROA. GDP growth has no statistically significant effect on ROA, as the effect coefficient is -1.133281 with a probability of 0.9486. The results suggest that GDP growth rates alone do not affect listed manufacturing firms' return on assets. The GDP effect coefficient is 79.84166 with a probability of 0.2225, indicating that GDP growth rates do not affect ROE statistically. These findings suggest that GDP growth rates do not significantly affect listed manufacturing firms' return on equity. The results consistently address GDP growth and manufacturing firm financial performance.

Examined seven Pakistani industries and found that macroeconomic indicators affected them differently. In addition,

| [52] | Lawal, A. I., Oseni, E., Lawal-Adedoyin, B. B., IseOlorunkanmi, J., Asaleye, A. J., Inegbedion, H., Santanu, M., DickTonye, A., Olagunju, O., & Ogunwole, E. (2022). Impact of macroeconomic variables on the Nigerian manufacturing sector. Cogent Economics and Finance, 10(1). https://doi.org/10.1080/23322039.2022.2090664 |

[52]

examined how macroeconomic and socio-economic/political factors affect Nigeria's manufacturing subsector. Their findings showed that macroeconomic variables and socio-political factors must be aligned to sustain manufacturing-driven economic growth. These studies emphasises the importance of macroeconomic indicators, such as GDP growth rates, in assessing manufacturing firm financial performance.

4.5.3. The Impact of Interest Rate Changes the Financial Performance of Listed Manufacturing Firms

The results show how interest rate changes affect listed manufacturing firms' ROE and ROA. Interest rates have no significant negative effect on ROA, as the direct coefficient for INTER is -16.30661 with a probability of 0.6032. This suggests that listed manufacturing firms' return on assets are not statistically affected by interest rate changes. Interest rates have a non-significant negative effect on ROE, as INTER has an effect coefficient of -179.3048 with a probability of 0.1259. This suggests that specific interest rate changes do not significantly affect listed manufacturing firms' return on equity. The findings shed light on how interest rate changes affect manufacturing firms' finances.

Examined how interest rates affect Nigerian manufacturing companies and found that interest rates significantly affected ROA but not ROE. The findings suggest that interest rate changes affect manufacturing firms' financial performance, which could affect profitability metrics.

| [6] | Cheong, C., & Hoang, H. V. (2021). Macroeconomic factors or firm-specific factors? An examination of the impact on corporate profitability before, during and after the global financial crisis. Cogent Economics and Finance, 9(1), 1–24. https://doi.org/10.1080/23322039.2021.1959703 |

[6]

Extended this analysis to Singapore and Hong Kong, finding that past profitability, firm size, and leverage significantly affect firm performance and that Hong Kong firms are more vulnerable to macroeconomic factors during crises. This suggests that manufacturers must carefully manage interest rate dynamics to maintain financial performance.

4.5.4. Potential Moderating Factors that could affect How Macroeconomic Variables Relate to Listed Manufacturing firms' Financial Performance