Abstract

Globalization is undergoing a profound structural transformation driven by rapid digital innovation and intensifying geopolitical rivalry. The international financial system, particularly the global payment architecture, has emerged as a key arena through which states and private actors seek to exercise political and economic influence. As money forms the foundation of payment systems, competing initiatives involving cryptocurrencies, stablecoins, and central bank digital currencies are reshaping the governance of cross-border finance and raising important questions about monetary sovereignty. At the same time, countries are strengthening regional financial safety nets, developing bilateral payment connectivity, and promoting local currency settlement arrangements to reduce dependence on existing financial infrastructures dominated by Western economies. Competition over the international trade invoicing currency has consequently intensified as governments seek greater strategic autonomy and geopolitical leverage. Existing studies rely on SWIFT data to uncover the competition for the invoicing currency in global trade. But such studies will underrepresent the shifts in trade settlement currencies, particularly because they will not capture trade involving sanctioned countries. The article therefore draws on information reported by PBOC on the share of Chinese Yuan used in cross-border goods trade as a proxy to capture the shifts. It then argues that meaningful erosion of dollar dominance will require not only political commitment but also the development of deeper financial markets, correspondent banking networks, trade finance, and foreign exchange hedging infrastructure in alternative currencies. These developments present both opportunities and some challenges for the future evolution of the global financial system.

Keywords

Digital Currencies, Payment Systems, Correspondent Banking, Geopolitics, Trade Invoicing

1. Introduction

Globalization is entering a period of profound transition. Among the most consequential yet under-appreciated dimension of this transition is the changing nature of money itself

. Digital technologies are reshaping how money is created, circulated, and governed, raising fundamental questions about power, sovereignty, and authority in the global political economy. For example, cryptocurrencies, which are designed to operate without central authorities, represent a radical challenge to existing monetary arrangements as they contest the premise that money must be issued or guaranteed by the states. On the other hand, stablecoins pegged to state currencies tend to blur the boundary between public and private authority. By contrast, the interest in promoting central bank digital currencies (CBDCs) by public authorities can be seen as the desire to reassert monetary sovereignty in response to the challenges posed by the emerging private forms of money in exercising monetary control.

It is important to put these developments against the backdrop of the post-World War II monetary architecture, which was centered on the US dollar and overseen by international financial institutions. While these arrangements were never politically neutral or universally beneficial, they provided a degree of predictability of key macroeconomic variables that facilitated cross-border trade, investment and financial flows. Yet, in recent decades the repeated use of unilateral economic and financial sanctions through financial market infrastructures (FMIs) controlled by Western countries to disrupt cross-border trade flows has undermined the usefulness of, and trust in, the existing monetary architecture. In response to the structural power exercised through the financial system by Western powers, many countries are building regional and bilateral payments network that can support cross-border local currency settlement

. Additionally, countries are also strengthening existing regional financial safety net (RFSN) arrangements. These initiatives are aimed at building greater financial autonomy in conducting cross-border trade and in responding to balance of payment crisis.

While building regional payments connectivity and strengthening RFSNs promote financial autonomy, there is shared belief among the Global South that the cogwheels in the global financial system are the FMIs that process financial messages to facilitate cross-border payments. By controlling these FMIs, Western powers determine who will be allowed to use the infrastructure to make cross-border payments to facilitate trade. Because the US dollar is the preferred invoicing currency for global trade, the United States gains significant leverage over nation states in enforcing its political agenda by granting or denying access to its domestic currency. Clawing away this political leverage requires the adoption of credible alternative invoicing currencies for global trade. Progress so far in this area has been slow as it faces significant geopolitical rivalry.

The novel contribution of this article is to view the developments discussed above from the geopolitical perspective. For example, in the case of newer forms of money, the emphasis is on understanding what the political forces or monetary sovereignty concerns might be driving these developments, and whether the economic role of money has been undermined in the process as different actors compete for market dominance and political influence. In the case of the invoicing currency for global trade, the focus is on what the key challenges are in reducing reliance on the US dollar and what institutional developments might be needed to adopt an alternative invoicing currency to the US dollar. These important issues are less well debated and articulated in the existing literature.

The rest of the article is organized as follows. Section 2 discusses the driving forces behind the newer forms of money and what the economic risks are if the existing two-tier monetary architecture with commercial banks providing a large share of the credit for real economic activities by taking retail deposits loses its importance. Section 3 examines the geopolitical considerations that underpin the regional initiatives to gain financial autonomy and the challenges they face in the process to achieve this objective. The hurdles to reducing the reliance on the US dollar as a vehicle currency in trade invoicing, and the institutional developments needed to facilitate this are explored in Section 4. The final section concludes.

2. Digital Money and Monetary Sovereignty

Over many centuries, money has served as the medium of exchange for trade, be it within or across borders. The ability to control the issuance and distribution of money therefore bestows exorbitant privilege to exert influence and power. Until recently, this privilege and the power to issue money and regulate its supply rested with sovereign states providing them authority over monetary sovereignty. This power, in turn, was delegated to central banks that had the mandate to regulate banks which served as the conduit for creation and distribution of money to the public. While central banks were entrusted with operational independence, the appointment of senior management of the central bank by the Parliament ensured that the government agenda remained in focus when central banks implemented monetary policy within their mandate. To the extent that settling payments for goods and services were done either through central bank money (cash) or commercial bank money (bank deposits), the states’ control over the economy and public at large remained influential.

In recent years, the private sector has increasingly used monetary sovereignty as a channel for influence. With digitalization in rapid progress across all sectors, the notion that cash and commercial bank money are the only means to settle claims for good and services is being challenged. Moreover, rapid advances in technology are fundamentally altering the architecture of payment systems. Users expect payments to be faster and cheaper as smart phones are increasingly used to facilitate financial transactions. These are being delivered through fintech innovations leading to widespread adoption of fast payment systems in domestic transactions. At the same time, advances in blockchain and distributed ledger technologies have led to the birth of newer forms of private money as an alternative to the traditional deposit-based commercial bank money.

Given the influential role money plays in our daily lives, the proliferation of private money in the form of cryptocurrencies and stablecoins can be interpreted as an attempt by the private sector to reconfigure power and governance arrangements to gain political influence. Under this premise, the narratives these actors employ to promote new forms of money are more likely intended to serve their interests and agenda rather than the public good. This section briefly discusses the different forms of digital money with the objective to understand both the driving forces behind them as well as what economic benefits they may bring, which the existing money forms held as cash or in bank deposits cannot do.

2.1. Cryptocurrencies

Cryptocurrencies are a class of digital or virtual assets designed to function as decentralized medium of exchange that have gained prominence since the introduction of Bitcoin in 2008. The claims on cryptocurrency one holds are not based on the identity of ownership we are familiar with in an account-based monetary system. Rather, they employ methods from cryptography and store the claims to our ownership in a distributed ledger in a tokenized form with identity established through a private key. This decentralized architecture reduces reliance on central authorities and the role of intermediaries. In contexts where trust in national currencies or institutions remains weak, cryptocurrencies can appear to offer a better store of value. But as cryptocurrencies often experience large and unpredictable price fluctuations, they are less reliable as a store of value or medium of exchange. This feature makes cryptocurrencies behave more as speculative assets rather than as money.

Proponents of cryptocurrencies argue that potential benefits of cryptos include faster cross-border payments and fostering financial inclusion for the unbanked population. However, both these arguments can be contested. Today, fast payment systems within the domestic networks have become a common feature. In some cases, they have also been extended to cross-border transactions using bilateral connectivity without employing blockchain technology. Further, smart phone penetration even in remote villages in many developing countries have had a more consequential impact on financial inclusion using traditional forms of money. Scalability and transaction efficiency also remain as key technological limitations of cryptocurrencies. Blockchain networks may struggle to process large volumes of transactions quickly and at low cost, which can hinder their practicality for global payment systems.

To the financial system, cryptocurrencies pose several risks that include fraud, money laundering, misappropriation and misleading disclosures to the investor. It is therefore no surprise that more than 53% of all cryptocurrencies listed on Gecko Terminal have failed, with the majority the of failures occurring in 2025

. Moreover, as cryptocurrencies operate outside of the regulatory perimeter lacking traditional financial safeguards, users may permanently lose funds if private keys are stolen or misplaced. Finally, environmental concerns cannot be ignored, particularly for cryptocurrencies that rely on energy-intensive consensus mechanisms for transaction validation such as proof-of-work.

2.2. Stablecoins

The shortcomings of cryptocurrencies to serve as a medium of exchange is being addressed by the private sector by promoting stablecoins. By pegging the value of stablecoins to some fiat currency, typically the US dollar, their monetary value is kept stable, and this allows them to be used as a medium of exchange. Stablecoins use the same distributed ledger and blockchain technology of cryptocurrencies allowing them to be exchanged on the same platforms that support crypto asset trading. This feature is used to promote stablecoins as a market response to meet the demand for reliable digital money for settlement on distributed ledger systems employing blockchain technology. Stablecoins effectively serve as digital cash within these ecosystems.

The business model employed by stablecoin issuers is to offer the public unremunerated liabilities in the form of a tokenized asset and then investing those liabilities in income yielding assets to generate a high net interest margin

. Essentially, this model tries to capture a share of the central banks’ monopoly income that is generated by issuing unremunerated liabilities in the form of currency notes, which are now on the decline. To provide incentives to the public to hold stablecoins, issuers work closely with crypto wallet providers and exchanges that take these stablecoins and offer attractive interest rates. The financial engineering is done by lending the stablecoins deposited in the crypto platforms’ custodial accounts to margin traders at high interest rates.

The initiatives being taken to introduce private forms of money are not being driven simply by a profit motive or to provide a public good. They are an attempt to shift power and influence over monetary sovereignty from the public authorities to the private sector. If a private currency achieves significant scale in international trade or retail payments, it can reduce demand for sovereign currencies, alter capital flows, and affect the transmission of monetary policy. For example, proposals such as Facebook’s Libra project—later rebranded as Diem—demonstrated how a consortium of private firms could attempt to construct a global currency infrastructure parallel to existing sovereign systems. Although regulatory push back ultimately derailed the initiative, it revealed the vulnerability of monetary sovereignty in the face of digital innovation.

There is a general recognition among authorities that a growing use of stablecoins as a settlement asset and in cross-border transactions can also pose risks to financial stability. Moreover, as stablecoins bypass the traditional financial network of banks, wider circulation of dollar-denominated stablecoins can make capital controls difficult to impose in many emerging and developing economies, and through that also undermine monetary sovereignty. In its Annual Report 2025, the Bank for International Settlements (BIS) warned that stablecoins have the potential to undermine monetary sovereignty and exacerbate the risk of capital flight from emerging economies

. But an increased circulation of stablecoins, say denominated in the US dollar, can also pose risks to advanced economies. For example, an ECB blog post mentions that if US dollar stablecoins become more widely used in the euro area, ECB’s control over monetary conditions could be weakened

.

While many countries see a wider circulation of stablecoins as a risk, the United States sees it as an opportunity because the use of stablecoins pegged to the US dollar in cross-border transactions will create demand for US dollar-denominated assets. It has therefore introduced the Genius Act to encourage the private sector to issue US dollar stablecoins that are backed primarily by US Treasury securities

. By doing so, the US is creating demand for Treasury securities at a time when its deficit is growing. It is therefore in the interest of the United States that the private sector grows the volume of US dollar stablecoins and makes them available for cross-border trade settlement. Indeed, the US Administration has made it clear that its support for stablecoins goes beyond encouraging technological innovation. Its goal is to protect the US dollars’ global dominance by expanding its use on digital platforms

, and to reduce borrowing costs by increasing the demand for US Treasuries through stablecoin reserve holdings.

As a countermeasure to this and to reduce the proliferation of US dollar stablecoins that may undermine monetary sovereignty, different central banks are in the process of promoting stablecoins in their local currencies through regulation. The ECB, the Hong Kong Monetary Authority and Monetary Authority of Singapore are prime examples of central banks in this camp

. The geopolitical competition is now playing out in the digital money space and in building the supporting infrastructure.

2.3. Central Bank Digital Currencies

The rise of the interest in CBDC can be linked to the Libra project proposal. The consensus view among central banks has been that if private money outside the remit of central banks is widely used in financial transactions and in cross-border payments, it can undermine monetary sovereignty. Against this backdrop, retail and wholesale CBDC projects represent state responses to the digitalization of money. Their objectives include: preserving monetary sovereignty; ensuring availability of state-backed digital settlement assets; and reducing the reliance on private digital currencies.

The first wave of experimentation revolved around retail CBDC intended for the domestic audience. The decline in use of cash and the desire of citizens to have digital cash for transactions were used to justify the need to introduce retail CBDC. But it has also been promoted as a safe settlement asset for transactions done on emerging digital and blockchain enabled platforms. Several countries, including China, India, Nigeria and the Bahamas have introduced retail CBDC pilot projects. Yet, among the countries that have already launched retail CBDCs, adoption remains slow and limited as existing domestic payment systems are efficient, fast and cheap.

With declining interest among the public to hold retail CBDC, central banks are now shifting their focus on wholesale CBDCs. Their impetus for this is the rise of distributed ledger technology (DLT) and asset tokenization, which raises important questions about the future role of central bank money. If DLT becomes more prevalent in future payment systems, central banks see demand for wholesale CBDC to settle tokenized assets on these platforms. At the same time, central banks can ensure that private money, like stablecoins, will not dominate such ecosystems and undermine the central banks’ ability to control macroeconomic outcomes. Central banks are also seeing wholesale CBDCs as having the potential to promote local currency settlements in cross-border financial transactions. Towards this goal, several initiatives involving the BIS have explored multi-CBDC platforms that allow participating central banks to transact directly with each other, reducing reliance on correspondent banking networks

.

2.4. Digital Money and the Economy

The earlier sub-sections in this chapter highlighted various forms of money and money-like instruments. The main role of money in the economy is to settle claims from trade in goods and services that result from consumption or investment. Classical economic theory categorizes money into two forms: inside money and outside money. Inside money is derived from the business of commercial banks issuing bank debt or bank deposits, whereas outside money is issued by the monetary authority. The distinction between the two is that outside money is an asset for the economy but is not a liability of anyone within the private sector, whereas inside money is backed by private credit

. Inside money is the one that funds economic activities of the private sector and it would disappear if all the claims held by banks on private creditors were to be settled.

Turning now to the different forms of money discussed earlier, only CBDCs will fall under the category of outside money. Because cryptocurrencies and stablecoins are not outside money, it is tempting to categorize them as inside money. But if we take the stricter definition that inside money is associated with private credit creation, cryptocurrencies and stablecoins fail to meet the test of inside money. As noted above, inside money created by commercial banks under the fractional reserve banking system is the one that supports the real economic activities by lending to businesses and investment projects. Unbacked cryptocurrencies, for example, are a pure form of speculative asset with no role in the real economic activities. Stablecoins that are backed by safe assets in compliance with regulatory requirements, also do not facilitate investment activities that require supply of private credit. More importantly, when private sector savings that are traditionally used by banks to supply credit to the economy shift to the newer forms of money, fractional reserve banking that facilitates private credit creation will be adversely affected. If the share of the newer forms of money in the economy rises, the conduct of monetary policy operations as well as the tools to be employed to steer macroeconomic outcomes will require a paradigm shift.

3. Building Financial Autonomy

In a speech delivered to the World Economic Forum's Annual Meeting 2026 in Davos

| [14] | Carney M. (2026). Davos 2026: Special address by Mark Carney, Prime Minister of Canada. World Economic Forum. |

[14]

, Canada’s Prime Minister Mark Carney summarized eloquently why the international rules-based order we have lived under for many decades is in the midst of a rupture and not a transition. He argued that many knew that the story of the international rules-based order was partially false and that the strongest would exempt themselves when convenient. Yet this fiction was useful, and American hegemony, in particular, helped provide public goods, open sea lanes, a stable financial system, collective security and support for frameworks for resolving disputes. But more recently, great powers have begun using economic integration as weapons, tariffs as leverage, financial infrastructure as coercion, supply chains as vulnerabilities to be exploited. Consequently, one cannot live within the lie of mutual benefit through integration, when integration becomes the source of one’s subordination.

Set against this backdrop, this section discusses how Western powers have exercised structural power through the financial system to pursue their interests, and how other countries have been building safeguards to dilute this structural power.

3.1. Exercising Structural Power

The hegemonic power of a country is often imagined to be derived from its military superiority. For example, from its ability to impose unilaterally a blockade of sea lanes for cargo ships of non-compliant countries using naval power, or their ability to conduct covert military operations to dislodge the elected leader of a sovereign state. The use of such military power, though effective, is used only in exceptional circumstances. The most consequential form of influence operates quietly through structural power that is exercised by the control over payment rails and FMIs. Payment rails are the channels through which financial messages and funds travel. They also denote the systems, which include cross-border messaging systems and correspondent banking networks, that enable the transfer of funds between parties. FMIs encompass a broader category: payment systems, central counterparties, securities settlement systems, and trade repositories.

Control over these infrastructures confers structural power by shaping the options available to access them. For example, in 2012, the European Union sanctioned banks in Iran, disconnecting them from the Society for Worldwide Interbank Financial Telecommunication (SWIFT) network that they control. The sanctioning authority does not have to compel every foreign bank individually. Instead, it shapes the structure within which those banks operate. Because the costs of exclusion from the dominant currency system are high, private actors internalize the constraints and adjust their behavior accordingly. The FMIs then become the conduit to project power and impose economic costs on sovereign states.

This mechanism illustrates how structural power differs from direct coercion. Structural power is embedded in everyday practices: the opening and maintenance of correspondent accounts; the clearing of trades; the settlement of securities; and the processing of payment instructions. These routine operations are used to control who can participate in global markets and on what terms. By shaping the architecture of access to dominant currencies, hegemons can influence trade patterns, investment flows, and even domestic policy trajectories.

The structural character of this power relies on the asymmetry between those who control FMIs and those who depend on them. For many emerging and developing economies, their banks rely on correspondent banking relationships with institutions in financial centers. When access to these institutions is curtailed—whether due to sanctions, regulatory concerns, or de-risking by global banks—the economic impact can be severe. The governance arrangements and operational control over the FMIs are therefore a critical conduit through which geopolitical power can be projected and enforced. As long as a small number of currencies and financial centers anchor the flows through global FMIs, those who host and regulate them will retain significant structural power.

3.2. Safeguards Through Regional Safety Net

In light of the intensifying geopolitical tensions and exercise of structural power through the financial system, one of the safeguards countries are building is to strengthen existing RFSN arrangements. A key motivation behind establishing RFSNs is the desire for greater regional autonomy in crisis management as relying solely on global institutions could be slow, politically sensitive, or insufficiently responsive to regional circumstances. For example, the Chiang Mai Initiative Multilateralization (CMIM), a regional safety net of $240 billion in the ASEAN region, and the Contingent Reserve Arrangement (CRA) of $100 billion between BRICS economies (Brazil, Russia, India, China, South Africa and newer members) are designed to provide a safety net during balance of payments and currency crisis. Under the current arrangements, 40 percent of CMIM and 30 percent of CRA can be drawn independent of IMF support or intervention.

In general, the goals of RFSNs are broader and include the following: to mobilize regional resources more quickly and design support programs that reflect shared economic structures and policy priorities; to build confidence in regional financial markets by demonstrating the availability of credible financial backstops; risk sharing among countries with closely connected financial systems; and to strengthen financial resilience by promoting regional surveillance and policy coordination. The RFSNs are usually part of a multi-layered safety net mechanism to be activated during a financial crisis, which also include the countries’ international reserves, central bank swap lines and the IMF backstop.

In a stocktaking paper, the IMF notes that while the global safety nets have become larger over the years, the various layers are fragmented, tend to operate in silos and offer uneven protection to countries in a crisis

. Moreover, many RSFNs were never used in a crisis as their swap-based framework can introduce uncertainty in financing and limit the duration of crisis support. To address this, the ASEAN+3 members have begun in recent years exploring the potential transition of the RFSN, which is now based on a contractual arrangement, to a paid-in-capital structure with its own balance sheet and governance framework

.

3.3. Safeguards Through Payments Connectivity

Section 3.1 emphasized how FMIs can be used to exercise structural power. To dilute this structural power, many countries are pursuing different strategies to build safeguards. One strategy is to promote local currency settlement in bilateral trade agreements. By invoicing trade in domestic currencies, states can reduce the reliance on intermediary currencies and associated clearing systems. Countries belonging to regional trade blocs, such as the ASEAN, are increasingly exploring such arrangements. One such arrangement involves Project Nexus

, an initiative of the BIS, to support local currency settlement and reduce reliance on correspondent banking. Nexus introduces a standardized connection model in which each country’s payment system only needs to connect once to the Nexus platform. This eliminates the need for numerous bilateral links between countries and simplifies the technical and operational processes involved in cross-border payments.

Across Russia, India, China and the United Arab Emirates (UAE), the emerging bilateral payments connectivity agenda is also designed to keep trade flowing outside dollar- and SWIFT-centric channels. On the messaging layer, Russia’s System for Transfer of Financial Messages (SPFS) works alongside China’s Cross-Border Interbank Payment System (CIPS) to route renminbi payments for trade in energy and other commodities. The UAE is positioning Dubai as a clearing hub for Asian currencies. Settlement is increasingly pushed into local currencies (RUB, INR, CNY, AED), supported by bilateral payment rails, prefunding, and netting arrangements. For trade with Russia, India has promoted rupee-denominated settlement via special rupee vostro accounts. When Indian importers pay for Russian goods, funds are credited in rupees to the Russian bank’s vostro account in India. The Russian bank can then use those balances to pay Indian exporters, invest in Indian assets, or convert the currency via approved channels. This mechanism enables local-currency trade without routing through dollars and thus avoiding the correspondent banking network.

Another area where several countries have sought to build financial autonomy is in the networks used for cashless payments. Many Asian countries have introduced cashless payments using quick response (QR) codes that bypass networks of credit card operators like Visa and Mastercard. Russia has developed the Mir payment card, a domestic alternative for cashless payments after Visa and Mastercard payments could not be used following financial sanctions imposed in 2014. India has also introduced the RuPay card using domestic payment rails as an alternative to Visa and Mastercard. In China, Alipay and WeChat Pay dominate the cashless payments market, which also use domestic payment networks.

4. Reducing Reliance on US Dollar

The belief that the existing monetary framework and rules-based international order requires a complete overhaul is now well-entrenched among decision-makers in many countries. There is broad consensus that one of the mechanisms through which this can be achieved is by establishing alternative payment networks and messaging platforms that are not subject to unilateral sanctions. But it is also recognized that achieving these objectives will require promoting alternative currencies to the US dollar in international trade invoicing. Still, available evidence based on a recent working paper by the IMF suggests that the share of invoicing currencies in global trade have broadly remained stable despite rising geopolitical tensions

. This section examines key challenges to reducing reliance on the US dollar in trade invoicing. But we will first start with some observations and cautionary note on trade invoicing patterns documented in the literature as reliable data on trade invoicing is difficult to obtain.

4.1. Data on Trade Invoicing

Most global trade is invoiced in just a few currencies with the US dollar being the dominant currency

. That said, identifying shifts in invoicing currency in global trade is challenging as the relevant information is not available in standard cross-country datasets. For example, the Direction of Trade statistics compiled by the IMF does not provide information on invoicing currency patterns. Information on the invoicing currency in trade is generally recorded in customs declarations forms, but these are not disseminated or stored as such information is not mandatory for reporting purposes.

Much of the evidence on currency invoicing patterns have been based on data collected prior to the Ukraine war. They were also often based on data reported by SWIFT. But the drawback of SWIFT data for the purpose of constructing a trade invoicing currency dataset is the difficulty to distinguish between payment orders that concern trade and those that concern other transactions. More importantly, global trade invoicing flows of sanctioned countries do not pass through SWIFT. Such countries tend to be major oil and gas exporters, implying that their trade volumes will be significant. Unless countries voluntarily report such transactions and the invoicing currency used, which by definition cannot be US dollar due to sanctions, the shifts in invoicing currencies are likely to be missed in the data collection exercise.

Clearly, there will be a bias towards capturing a large share of the US dollar as an invoicing currency particularly in the current geopolitical environment. To provide some examples, Mongolia imports oil and gas from Russia and sells coking coal to China, but the invoicing currency for their trade in today’s environment is likely to be Chinese Yuan (CNY). These transactions will not go through the SWIFT network, and hence, are not captured if SWIFT dataset is used to draw conclusions on changes in invoicing currency patterns. India’s purchases of Russian oil and gas can be in Indian Rupee (INR) or other currencies, but the data on these transactions may also not be available.

Focusing more narrowly on China, the figures published by PBOC under the RMB Internationalization Reports provide some insights into the shifting trend towards CNY settlement of cross-border trade in goods and services

. These reports indicate that the share of cross-border CNY settlement of trade in goods has been 11.7% of the total cross-border goods trade in 2018. In 2024, this share rose to 27.2%. For cross-border trade in services, the share of CNY settlement rose from 20.4% in 2018 to 31.9% in 2024. Over a longer time horizon, the share of China’s cross-border commodity trade settled in CNY has risen from around 11% in 2013 to around 32% in 2026

. Clearly, these statistics point to a sustained increase in CNY settled cross-border trade that is consistent with the Renminbi internationalization agenda of the Chinese government. When these transactions and settlements are processed through direct CIPS members, they will fall outside the SWIFT messaging system.

Data from China cited above provides clear evidence that there has been a gradual shift towards increased use of CNY to settle cross-border trade in goods and services. It is tempting to argue that these changes are not significant to pose a threat to the US dollar’s dominance in global trade settlement. But if lessons of history are to be taken seriously, watershed events can lead to a dramatic shift out of a dominant currency. The rise of US dollar as the dominant currency after World War II at the expense of the Pound Sterling and a further decline in the use of Pound Sterling for invoicing trade after the Brexit are prime examples. The wars in Ukraine and in the Middle East could be such watershed moments for the US dollar going forward. But for that to happen, significant changes to the market structure that makes the US dollar a dominant currency has to take place. We will examine next the reasons for US dollar being the preferred invoicing currency in global trade.

4.2. Reasons for US Dollar Dominance

The openness and depth of US debt and capital markets underpinned by a clear legal framework and effective regulatory oversight and control are important factors that make US dollar the preferred invoicing currency in global trade. But recent developments have raised doubts over some of these beliefs. Often times, executive orders have sidestepped the legal framework raising concerns about the true ownership rights when holding US assets. And the fiscal position and debt trajectory of the United States have raised questions as to whether a devaluation of the US dollar or a haircut on US Treasury debt will be needed to put government debt on sustainable path. Despite these risks, international trade partners continue to invoice goods and services in US dollars. There are a number of reasons why the currency of choice for invoicing international trade is the US dollar, which are explored below.

Diversified global supply chain networks have become essential to modern trade allowing firms to reduce dependence on a single supplier or country. To integrate suppliers from multiple countries into product pricing, large firms require that the currency risk from the supply chain network is adequately managed. That is usually the task of the corporate treasury department. To the extent that supplier contracts are priced in one currency, which could be in a foreign currency, the foreign exchange (FX) risk in multiple currencies does not have to be additionally managed in product pricing. This leads to the preference of one dominant currency to be used in trade invoicing when firms rely on multiple suppliers from different countries.

Another often underestimated factor supporting the case for US dollar as the invoicing currency is the access to trade financing in dollars. Trade finance is a collection of financial tools and instruments supporting international trade by reducing the inherent risks involved in cross-border trade. The inherent risks include non-payment and delivery delays. The instruments used to mitigate the risks are letters of credit, bank guarantees and trade credit insurance, which are provided by financial institutions acting as intermediaries between the exporter and importer. The largest global banks tend to account for a quarter to a third of the global supply of bank-intermediated trade finance, with a high proportion of the financing denominated in US dollars

. That is because of the deeper liquidity in US funding markets, which allow global banks to provide more competitive trade financing terms when it is denominated in US dollars.

A third reason for dollar dominance in trade invoicing is that markets for hedging the domestic currency risk against the US dollar are far more liquid and deep compared to those in other currencies. Indeed, the absence of liquid FX markets for many world currencies against the euro has been one of these reasons why the euro has not been able to gain market share in international trade invoicing. The FX hedging markets are typically provided by global correspondent banks, which are also often the providers of trade finance.

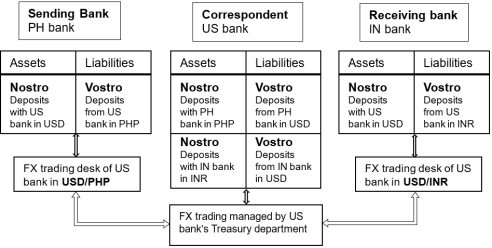

To illustrate their role,

Figure 1 shows the balance sheet structure of banks using the correspondent banking model

. The schematic diagram illustrates the transactions that take place when an importer of goods from, say the Philippines, has to settle an invoice amount negotiated in the US dollar to an exporter in India. While the Philippine peso (PHP) paid by the importer will finally be settled in INR in the exporters’ bank account, the transaction will require an intermediate conversion: from the PHP to US dollars and then from US dollars to INR. The correspondent bank will be making markets in these currency pairs, which will be liquid as they are anchored to one vehicle currency that is widely traded.

Figure 1. Correspondent banking model.

If the correspondent bank is taken out of the FX transaction, the sending bank (PH bank) and the receiving bank (IN bank) will have to hold vostro accounts in the respective domestic currency of the other bank. Managing the invoice payment that is now billed directly in INR (local currency invoicing by the exporter) will require the PH bank to maintain an FX desk to make markets in the PHP-INR currency pair. If the PH bank were to have clients that buy or sell goods to 50 other countries, then the PH bank has to have trading desks that make markets in each of the 50 currency pairs against the PHP. The same operational challenge will also be faced by the IN bank in the absence of a correspondent banking relationship. The absence of liquid hedging markets in different currency pairs as well as the need to manage the FX risk against multiple currencies will also complicate the corporate treasury function of the importing or exporting firm if they have clients in multiple countries.

When the cross-border trade involves commodities like oil and gas where the transaction amounts can be very large, other challenges arise when the invoicing is done in local currency. This shows up when the trade flows between the countries involved is one-sided. Taking the example of settlement of oil imports from Russia to India in INR, the Russian energy companies will accumulate large balances that are held in the special rupee vostro account. But as India’s exports to Russia are not commensurate with its imports from Russia, the balances in these accounts will require conversion to other domestic currencies to pay for imports of Russian firms from those countries. Until conversion, Russian energy firms will face significant exchange rate risk from holding INR, which cannot be hedged easily.

There are other factors that come into play when choosing the invoicing currency for commodity trades. Most importers of commodities like oil and gas commonly hedge price risk in forward markets and through other derivative instruments to protect against volatile market movements. Clearly, from an individual firm’s perspective, economic motivation rather than geopolitical motivation is what determines the choice of the invoicing currency to be used in cross-border trade. Because the hedging markets provided by large financial institutions for these commodities are primarily denominated in US dollar, it becomes the preferred invoicing currency for the transaction. These legacies make it difficult to shift away from US dollar for large commodity transactions.

Finally, central banks in most emerging and developing market economies take into consideration the market practice of their domestic firms to use a dominant currency in global trade, typically the US dollar, in their monetary policy and exchange rate management decisions. This provides further reassurance to importers and exporters to favour the dominant currency invoicing backed by their central bank’s commitment to prudently manage the domestic currency risk versus the most favoured currency in international trade.

4.3. Actions Needed to Reduce Dollar Dominance

The previous section highlighted the various factors that contribute to the US dollar being the preferred invoicing currency in global trade. Efforts to facilitate local currency settlement through multilateral payment network projects such as Nexus and mBridge under the BIS Innovation Hub, however, cannot address the underlying reasons why US dollar invoicing is preferred by all parties in international trade. These newer payment networks are more likely to support retail transactions or small value trade settlements in local currencies. But international firms and commodity import and export firms are unlikely to use these networks for large value transactions.

If a viable alternative invoicing currency to the US dollar has to gain traction, many of the financial market infrastructures needed, such as correspondent banking networks, derivatives markets for hedging price risk, and access to trade finance must develop in the alternative currency. The currency of any country that has significant market size and trade flows could be a potential candidate for the alternative invoicing currency. That candidate is likely to be China, which also has large international banks that can facilitate provision of trade finance and offer correspondent banking services in the CNY

. But that will also require a significant number of its trading partners to support the development of CNY as an alternative currency to the US dollar in global trade invoicing. Assuming that several members within forums such as the ASEAN+3 and the BRICS-plus support this idea, network effects can quickly build up to provide a viable alternative to the US dollar in global trade invoicing. If sizable share of global trade of a country is invoiced in CNY, the country’s central bank will be incentivized to manage the exchange rate volatility of the domestic currency versus the CNY in its monetary policy decision-making framework.

5. Summary and Conclusions

Globalization is being reshaped by digital financial innovation and intensifying geopolitical competition, particularly through transformations in the global payment system and the evolving nature of money. Newer forms of money, such as cryptocurrencies, stablecoins and CBDC are being assessed from the technology they bring for facilitating cheaper and faster domestic and cross-border transactions. But their potential adverse effects on credit creation to support real economic activities tend to receive less attention. Specifically, when private sector savings that are traditionally used by banks to supply credit to the economy shift to the newer forms of money, fractional reserve banking that facilitates private credit creation will be adversely affected. More work needs to done in understanding these effects before promoting newer forms of money.

The financial system—especially payment infrastructures and trade invoicing currencies—has become a central arena for exercising geopolitical influence. Western powers have exercised structural power through control of FMIs, such as payment messaging systems and correspondent banking networks. Because exclusion from dollar-clearing and messaging systems carries high costs, many countries—particularly in the Global South—are developing regional financial safety nets and alternative payment networks to reduce dependence on Western-controlled infrastructures. These initiatives include bilateral payment connectivity, regional crisis funding mechanisms, and local-currency trade settlement arrangements.

Despite these initiatives, the US dollar remains dominant in international trade invoicing due to a number of structural advantages such as deep financial markets, liquid foreign exchange hedging instruments, and widespread availability of dollar-denominated trade finance. Network effects and operational efficiencies also reinforce the dollar’s role as a global vehicle currency. While geopolitical tensions may encourage promoting alternative invoicing currencies, meaningful shifts away from the dollar would require development of markets for hedging instruments, correspondent banking networks and access to trade finance in the alternative invoicing currency.

Building political consensus on a preferred alternative invoicing currency is hard. But for that to happen, the necessary market infrastructure that now supports the case for the US dollar as the preferred invoicing currency has to be developed. The recent geopolitical events with two major wars and sanctions overuse by the Western countries could well be a trigger to build the necessary consensus to support an alternative currency to be used for global trade invoicing.

Abbreviations

SWIFT | Society for Worldwide Interbank Financial Telecommunication |

PBOC | People’s Bank of China |

CBDC | Central Bank Digital Currency |

FMI | Financial Market Infrastructure |

US | United States |

RFSN | Regional Financial Safety Net |

BIS | Bank for International Settlements |

ECB | European Central Bank |

DLT | Digital Ledger Technology |

CMIM | Chiang Mai Initiative Multilateralization |

ASEAN | Association of Southeast Asian Nations |

CRA | Contingent Reserve Arrangement |

IMF | International Monetary Fund |

UAE | United Arab Emirates |

SPFS | System for Transfer of Financial Messages |

CIPS | Cross-Border Interbank Payment System |

RUB | Russian Rouble |

INR | Indian Rupee |

CNY | Chinese Yuan |

AED | United Arab Emirates Dirham |

QR | Quick Response |

FX | Foreign Exchange |

PHP | Philippine Peso |

BRICS | Brazil, Russia, India, China, South Africa |

Author Contributions

Srichander Ramaswamy: Conceptualization, Investigation, Methodology, Formal Analysis, Writing – original draft, Writing – review & editing

Conflicts of Interest

The author declares no conflicts of interest.

References

| [1] |

Markus K Brunnermeier M, James H, Landau J-P. Digitalization of money. BIS Working Papers. 2021.

https://www.bis.org/publ/work941.pdf

|

| [2] |

Bank for International Settlements. (2024). Project Nexus overview: Enabling instant cross-border payments at scale.

https://www.bis.org/innovation_hub/projects/nexus_brochure.pdf

|

| [3] |

Bank for International Settlements. (2022). Project mBridge: Connecting economies through CBDC.

https://www.bis.org/publ/othp59.pdf

|

| [4] |

Lee, S. Dead coins: Over 50% of cryptocurrencies have failed [Internet]. (2026). Available from:

https://www.coingecko.com/research/publications/how-many-cryptocurrencies-failed

[Accessed: 2026-02-17].

|

| [5] |

Ramaswamy, S. (2024). Stablecoins: Business models, systemic risks and policy perspectives. SEACEN Centre.

https://www.seacen.org/publications/RePEc/702001-100493-PDF.pdf

|

| [6] |

Bank for International Settlements. (2025). Chapter III: The next-generation monetary and financial system. BIS Annual Economic Report.

https://www.bis.org/publ/arpdf/ar2025e3.pdf

|

| [7] |

Schaaf, J. (2025). From hype to hazard: What stablecoins mean for Europe. The ECB Blog.

https://www.ecb.europa.eu/press/blog/date/2025/html/ecb.blog20250728~e6cb3cf8b5.en.html

|

| [8] |

GENIUS Act. (2025). Public Law 119-27, 139 Stat. 419.

https://www.congress.gov/119/plaws/publ27/PLAW-119publ27.pdf

|

| [9] |

Shirai, S. (2025). Can stablecoins extend US dollar dominance? East Asia Forum.

https://eastasiaforum.org/2025/08/09/can-stablecoins-extend-us-dollar-dominance/

|

| [10] |

Hong Kong Monetary Authority. (2025). Stablecoins Ordinance: Guideline on supervision of licensed stablecoin issuers.

https://www.hkma.gov.hk/media/eng/doc/key-functions/ifc/stablecoin-issuers/Guideline_on_supervision_of_licensed_stablecoin_issuers_eng.pdf

|

| [11] |

Monetary Authority of Singapore. (2023). MAS finalises stablecoin regulatory framework. Retrieved from:

https://www.mas.gov.sg/news/media-releases/2023/mas-finalises-stablecoin-regulatory-framework

[Accessed: 2026-05-10].

|

| [12] |

BIS Innovation Hub. (2023). Project Mariana: Cross-border exchange of wholesale CBDCs using automated market-makers.

https://www.bis.org/publ/othp75.pdf

|

| [13] |

Praet P. (2012). The role of money in a market economy. Speech at the Bargeldsymposium organised by the Deutsche Bundesbank.

https://www.bis.org/review/r121011c.pdf

|

| [14] |

Carney M. (2026). Davos 2026: Special address by Mark Carney, Prime Minister of Canada. World Economic Forum.

|

| [15] |

International Monetary Fund. (2025). The global financial safety net—A stocktaking.

https://www.imf.org/en/publications/policy-papers/issues/2025/10/09/the-global-financial-safety-net-a-stocktaking-571099

|

| [16] |

Yu J, Kim S. (2025). From concept to consensus: ASEAN+3’s journey toward a stronger regional financial safety net. AMRO Blog.

https://amro-asia.org/from-concept-to-consensus-asean3s-journey-toward-a-stronger-regional-financial-safety-net

|

| [17] |

Boz E, Brüggen A, Casas C, Georgiadis G, Gopinath G, Mehl A. (2025). Patterns of invoicing currency in global trade in a fragmenting world economy. IMF Working Paper WP/25/178.

https://www.imf.org/en/publications/wp/issues/2025/09/12/patterns-of-invoicing-currency-in-global-trade-in-a-fragmenting-world-economy-570297

|

| [18] |

Boz E, Casas C, Georgiadis G, Gopinath G, Le Mezoc H, Mehl A, Nguyen T. Patterns of invoicing currency in global trade: New evidence. Journal of International Economics. 136(C). 2022.

https://www.sciencedirect.com/science/article/pii/S0022199622000368

|

| [19] |

People's Bank of China. (2019). 2019 RMB Internationalization Report. Retrieved from:

https://www.pbc.gov.cn/en/3688241/3688636/3828468/3830455/2025080817511293759/2019121309565566684.pdf

|

| [20] |

People's Bank of China. (2025). 2025 RMB Internationalization Report. Retrieved from:

https://www.pbc.gov.cn/en/3688241/3688636/3828468/5624529/2025123116494089198/2025123116480428858.pdf

|

| [21] |

MacroMicro. (2025). China - Commodity Trade - RMB Cross-border Settlement. Retrieved from:

https://en.macromicro.me/collections/23654/dedollarization/137334/china-commodity-trade-rmb-crossborder-settlement

|

| [22] |

Committee on the Global Financial System. (2014). Trade finance: Developments and issues. CGFS Papers.

https://www.bis.org/publ/cgfs50.pdf

|

| [23] |

Ramaswamy, S. (2025). Wholesale CBDC: Examining the business case. SEACEN Centre.

https://www.seacen.org/publications/RePEc/702001-100493-PDF.pdf

|

| [24] |

Ramaswamy, S. The threat of financial sanctions: What safeguards can central banks build? China & World Economy. 2022. 30(3): 23-41.

https://onlinelibrary.wiley.com/doi/abs/10.1111/cwe.12417

|

Cite This Article

-

APA Style

Ramaswamy, S. (2026). Exercising Geopolitical Influence Through the Financial System. International Journal of Economics, Finance and Management Sciences, 14(4), 263-272. https://doi.org/10.11648/j.ijefm.20261404.12

Copy

|

Copy

|

Download

Download

ACS Style

Ramaswamy, S. Exercising Geopolitical Influence Through the Financial System. Int. J. Econ. Finance Manag. Sci. 2026, 14(4), 263-272. doi: 10.11648/j.ijefm.20261404.12

Copy

|

Download

AMA Style

Ramaswamy S. Exercising Geopolitical Influence Through the Financial System. Int J Econ Finance Manag Sci. 2026;14(4):263-272. doi: 10.11648/j.ijefm.20261404.12

Copy

|

Download

-

@article{10.11648/j.ijefm.20261404.12,

author = {Srichander Ramaswamy},

title = {Exercising Geopolitical Influence Through the Financial System},

journal = {International Journal of Economics, Finance and Management Sciences},

volume = {14},

number = {4},

pages = {263-272},

doi = {10.11648/j.ijefm.20261404.12},

url = {https://doi.org/10.11648/j.ijefm.20261404.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijefm.20261404.12},

abstract = {Globalization is undergoing a profound structural transformation driven by rapid digital innovation and intensifying geopolitical rivalry. The international financial system, particularly the global payment architecture, has emerged as a key arena through which states and private actors seek to exercise political and economic influence. As money forms the foundation of payment systems, competing initiatives involving cryptocurrencies, stablecoins, and central bank digital currencies are reshaping the governance of cross-border finance and raising important questions about monetary sovereignty. At the same time, countries are strengthening regional financial safety nets, developing bilateral payment connectivity, and promoting local currency settlement arrangements to reduce dependence on existing financial infrastructures dominated by Western economies. Competition over the international trade invoicing currency has consequently intensified as governments seek greater strategic autonomy and geopolitical leverage. Existing studies rely on SWIFT data to uncover the competition for the invoicing currency in global trade. But such studies will underrepresent the shifts in trade settlement currencies, particularly because they will not capture trade involving sanctioned countries. The article therefore draws on information reported by PBOC on the share of Chinese Yuan used in cross-border goods trade as a proxy to capture the shifts. It then argues that meaningful erosion of dollar dominance will require not only political commitment but also the development of deeper financial markets, correspondent banking networks, trade finance, and foreign exchange hedging infrastructure in alternative currencies. These developments present both opportunities and some challenges for the future evolution of the global financial system.},

year = {2026}

}

Copy

|

Download

-

TY - JOUR

T1 - Exercising Geopolitical Influence Through the Financial System

AU - Srichander Ramaswamy

Y1 - 2026/07/17

PY - 2026

N1 - https://doi.org/10.11648/j.ijefm.20261404.12

DO - 10.11648/j.ijefm.20261404.12

T2 - International Journal of Economics, Finance and Management Sciences

JF - International Journal of Economics, Finance and Management Sciences

JO - International Journal of Economics, Finance and Management Sciences

SP - 263

EP - 272

PB - Science Publishing Group

SN - 2326-9561

UR - https://doi.org/10.11648/j.ijefm.20261404.12

AB - Globalization is undergoing a profound structural transformation driven by rapid digital innovation and intensifying geopolitical rivalry. The international financial system, particularly the global payment architecture, has emerged as a key arena through which states and private actors seek to exercise political and economic influence. As money forms the foundation of payment systems, competing initiatives involving cryptocurrencies, stablecoins, and central bank digital currencies are reshaping the governance of cross-border finance and raising important questions about monetary sovereignty. At the same time, countries are strengthening regional financial safety nets, developing bilateral payment connectivity, and promoting local currency settlement arrangements to reduce dependence on existing financial infrastructures dominated by Western economies. Competition over the international trade invoicing currency has consequently intensified as governments seek greater strategic autonomy and geopolitical leverage. Existing studies rely on SWIFT data to uncover the competition for the invoicing currency in global trade. But such studies will underrepresent the shifts in trade settlement currencies, particularly because they will not capture trade involving sanctioned countries. The article therefore draws on information reported by PBOC on the share of Chinese Yuan used in cross-border goods trade as a proxy to capture the shifts. It then argues that meaningful erosion of dollar dominance will require not only political commitment but also the development of deeper financial markets, correspondent banking networks, trade finance, and foreign exchange hedging infrastructure in alternative currencies. These developments present both opportunities and some challenges for the future evolution of the global financial system.

VL - 14

IS - 4

ER -

Copy

|

Download